SkyWest Airlines 2002 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2002 SkyWest Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

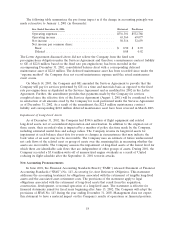

|

|

impacted by changes to the contracts, the annual contract negotiations and the Company’s ability to

earn incentive payments contemplated by the contracts.

Maintenance

The Company operates under an FAA-approved continuous inspection and maintenance program.

The Company’s historical maintenance accounting policy for engine overhaul costs has included a

combination of accruing for overhaul costs on a per-flight-hour basis at rates estimated to be sufficient

to cover the overhauls (the accrual method) and capitalizing the cost of engine overhauls and expensing

the capitalized cost over the estimated useful life of the overhaul (the deferral method). The Company

uses the deferral method of accounting for Brasilia engines and was using the accrual method for CRJ

engines through December 31, 2001. As discussed below, during the quarter ended March 31, 2002, the

Company elected to change its method of accounting for CRJ engine overhauls to expensing overhaul

maintenance events as incurred (the direct-expense method). The costs of maintenance for airframe

and avionics components, landing gear and normal recurring maintenance are expensed as incurred.

For leased aircraft, the Company is subject to lease return provisions that require a minimum portion

of the ‘‘life’’ of an overhaul be remaining on the engine at the lease return date. For Brasilia engine

overhauls related to leased aircraft to be returned, the Company adjusts the estimated useful lives of

the final engine overhauls based on the respective lease return dates.

Effective August 1, 2001, the Company and GE Engine Services, Inc. (GE) executed a sixteen-year

engine services agreement (the Services Agreement) covering the scheduled and unscheduled repair of

CRJ engines. Under the terms of the Services Agreement, the Company agreed to pay GE a fixed rate

per-engine-hour, payable monthly, and GE assumed the responsibility to overhaul the Company’s CRJ

engines as required during the term of the Services Agreement, subject to certain exclusions. The

Company accounted for all CRJ engine overhaul costs through December 31, 2001 under the accrual

method using an estimated hourly accrual rate through August 1, 2001, and then, for the period from

August 1, 2001 through December 31, 2001, using the fixed rate per-engine-hour pursuant to the

Services Agreement.

In response to changing market conditions, the Company and one of its major partners agreed to

modify the method of reimbursement for CRJ engine overhaul costs under their contract flying

arrangement beginning in 2002 from reimbursement based on engine flight hours to reimbursement

based on actual engine overhaul costs at the maintenance event. In April 2002, the Company and GE

signed a letter agreement (the Letter Agreement) amending the Services Agreement in response to the

change with the Company’s major partner. Pursuant to the Letter Agreement, payments under the

Services Agreement were modified from the per-engine-hour basis, payable monthly, to a time and

materials basis, payable at the maintenance event. The revised payment schedule extended through

December 31, 2002, at which time monthly payments were to resume on the fixed rate per-engine-hour,

as adjusted for the difference in the actual payments made under the Letter Agreement during 2002 as

compared to the payments that would have been made under the Services Agreement during 2002. As

discussed below, on March 14, 2002, the Services Agreement was further amended.

Due to the change in the Company’s contractual arrangement with one of its major partners and

based on the Letter Agreement, the Company elected to change from the accrual method to the direct-

expense method for CRJ engine overhaul costs effective January 1, 2002. The Company believes the

direct-expense method is preferable in the circumstances because the maintenance liability is not

recorded until the maintenance services are performed, the direct-expense method eliminates significant

estimates and judgments inherent under the accrual method, and it is the predominant method used in

the airline industry. Accordingly, during the three months ended March 31, 2002, the Company

reversed its engine overhaul accrual that totaled $14.1 million as of January 1, 2002 by recording a

cumulative effect of change in accounting principle of $8.6 million (net of income taxes of $5.5 million).

17