Red Lobster 2005 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2005 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

NOTE 1

Summary of Significant Accounting Policies

Operations and Principles of Consolidation

The consolidated financial statements include the opera-

tions of Darden Restaurants, Inc. and its wholly owned sub-

sidiaries. We own and operate various restaurant concepts

located in the United States and Canada, with no franchis-

ing. We also license 37 restaurants in Japan. All significant

intercompany balances and transactions have been elimi-

nated in consolidation.

Fiscal Year

Our fiscal year ends on the last Sunday in May. Fiscal

2005 and 2003 both consisted of 52 weeks of operation.

Fiscal 2004 consisted of 53 weeks of operation.

Cash Equivalents

Cash equivalents include highly liquid investments such

as U.S. treasury bills, taxable municipal bonds and money

market funds that have a maturity of three months or less.

Amounts receivable from credit card companies are also

considered cash equivalents because they are both short-

term and highly liquid in nature and are typically converted

to cash within three days of the sales transaction.

Inventories

Inventories consist of food and beverages, and are

valued at the lower of weighted-average cost or market.

Land, Buildings and Equipment

Land, buildings and equipment are recorded at cost less

accumulated depreciation. Repair and maintenance costs

incurred to maintain the appearance and functionality of the

land, buildings and equipment that do not extend its useful

life or that are less than $1 are expensed as incurred. Building

components are depreciated over estimated useful lives

ranging from seven to 40 years using the straight-line method.

Leasehold improvements, which are reflected on our consoli-

dated balance sheets as a component of buildings, are

amortized over the lesser of the expected lease term, includ-

ing cancelable option periods, or the estimated useful lives of

the related assets using the straight-line method. Equipment

is depreciated over estimated useful lives ranging from two

to ten years also using the straight-line method. Accelerated

depreciation methods are generally used for income tax

purposes. Depreciation and amortization expense associ-

ated with buildings and equipment amounted to $206,552,

$203,349 and $184,963, in fiscal 2005, 2004 and 2003,

respectively. In fiscal 2005, 2004 and 2003, we had losses

on disposal of land, buildings and equipment of $1,164, $104

and $2,456, respectively, which were included in selling,

general and administrative expenses.

Capitalized Software Costs

Capitalized software, which is a component of other

assets, is recorded at cost less accumulated amortization.

Capitalized software is amortized using the straight-line

method over estimated useful lives ranging from three to ten

years. The cost of capitalized software at May 29, 2005 and

May 30, 2004, amounted to $51,292 and $46,629, respec-

tively. Accumulated amortization as of May 29, 2005 and

May 30, 2004 amounted to $19,877 and $14,301, respec-

tively. Amortization expense associated with capitalized

software amounted to $6,667, $6,655 and $6,255, in fiscal

2005, 2004 and 2003, respectively.

Trust-Owned Life Insurance

In August 2001, we caused a trust that we previously had

established to purchase life insurance policies covering cer-

tain of our officers and other key employees (trust-owned life

insurance or TOLI). The trust is the owner and sole beneficiary

of the TOLI policies. The policies were purchased to offset a

portion of our obligations under our non-qualified deferred

compensation plan. The cash surrender value of the policies is

included in other assets while changes in cash surrender value

are included in selling, general and administrative expenses.

Liquor Licenses

The costs of obtaining non-transferable liquor licenses

that are directly issued by local government agencies for

nominal fees are expensed as incurred. The costs of pur-

chasing transferable liquor licenses through open markets

in jurisdictions with a limited number of authorized liquor

licenses are capitalized. Annual liquor license renewal fees

are expensed.

Impairment of Long-Lived Assets

Land, buildings and equipment and certain other assets,

including capitalized software costs and liquor licenses, are

reviewed for impairment whenever events or changes in

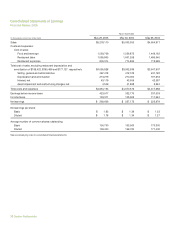

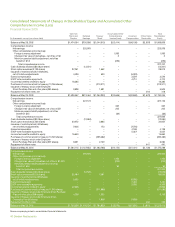

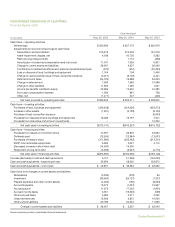

Notes to Consolidated Financial Statements

Financial Review 2005

(Dollar amounts in thousands, except per share data)

42 Darden Restaurants