Red Lobster 2005 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2005 Red Lobster annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

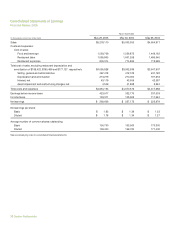

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Financial Review 2005

Darden Restaurants 29

patterns and claim reserve, management and settlement

practices. Unanticipated changes in these factors may

produce materially different amounts of reported expense

under these programs.

Income Taxes

We estimate certain components of our provision for

income taxes. These estimates include, among other

items, depreciation and amortization expense allowable for

tax purposes, allowable tax credits for items such as taxes

paid on reported employee tip income, effective rates for

state and local income taxes and the tax deductibility of

certain other items.

Our estimates are based on the best available informa-

tion at the time that we prepare the provision. We generally

file our annual income tax returns several months after our

fiscal year-end. Income tax returns are subject to audit by

federal, state and local governments, generally years after

the returns are filed. These returns could be subject to mate-

rial adjustments or differing interpretations of the tax laws.

Liquidity and Capital Resources

Cash flows generated from operating activities provide

us with a significant source of liquidity, which we use to

finance the purchases of land, buildings and equipment and

to repurchase shares of our common stock. Since substan-

tially all our sales are for cash and cash equivalents and

accounts payable are generally due in five to 30 days, we

are able to carry current liabilities in excess of current

assets. In addition to cash flows from operations, we use

a combination of long-term and short-term borrowings to

fund our capital needs.

We manage our business and our financial ratios to

maintain an investment grade bond rating, which allows

flexible access to financing at reasonable costs. Currently,

our publicly issued long-term debt carries “Baa1” (Moody’s

Investors Service), “BBB+” (Standard & Poor’s) and

“BBB+” (Fitch) ratings. Our commercial paper has ratings

of “P-2” (Moody’s Investors Service), “A-2” (Standard &

Poor’s) and “F-2” (Fitch). These ratings are as of the date

of this annual report and have been obtained with the

understanding that Moody’s Investors Service, Standard

& Poor’s and Fitch will continue to monitor our credit and

make future adjustments to these ratings to the extent

warranted. The ratings may be changed, superseded, or

withdrawn at any time.

Our commercial paper program is our primary source

of short-term financing. At May 29, 2005, there were no

borrowings outstanding under the program. To support our

commercial paper program, we have a credit facility under a

Credit Agreement dated October 17, 2003, as amended, with

a consortium of banks, including Wachovia Bank, N.A., as

administrative agent, under which we can borrow up to $400

million. The credit facility allows us to borrow at interest rates

based on a spread over (i) LIBOR or (ii) a base rate that is the

higher of the prime rate, or one-half of one percent above the

federal funds rate, at our option. The interest rate spread over

LIBOR is determined by our debt rating. The credit facility

expires on October 17, 2008 and contains various restric-

tive covenants, including a leverage test that requires us to

maintain a ratio of consolidated total debt to consolidated

total capitalization of less than 0.55 to 1.00 and a limitation

of $25 million on priority debt, subject to certain exceptions.

The credit facility does not, however, contain a prohibition on

borrowing in the event of a ratings downgrade or a “material

adverse change,” as defined in the Credit Agreement. None

of these covenants are expected to impact our liquidity or

capital resources. At May 29, 2005, we were in compliance

with all covenants under the Credit Agreement.

At May 29, 2005, our long-term debt consisted princi-

pally of: (1) $150 million of unsecured 5.75 percent medium-

term notes due in March 2007, (2) $75 million of unsecured

7.45 percent medium-term notes due in April 2011, (3)

$100 million of unsecured 7.125 percent debentures due in

February 2016 and (4) an unsecured, variable rate $27 million

commercial bank loan due in December 2018 that is used to

support two loans from us to the Employee Stock Ownership

Plan portion of the Darden Savings Plan. We also have

$150 million of unsecured 8.375 percent senior notes due in

September 2005 and $150 million of unsecured 6.375 per-

cent notes due in February 2006 included in current liabilities,

which we plan to repay through the issuance of unsecured

debt securities in fiscal 2006. Through a shelf registration on

file with the Securities and Exchange Commission (SEC), we

may issue up to an additional $125 million of unsecured debt

securities from time to time. The debt securities may bear

interest at either fixed or floating rates and may have maturity

dates of nine months or more after issuance.