PG&E 2012 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2012 PG&E annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

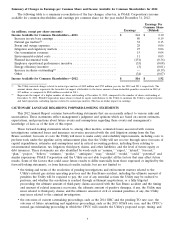

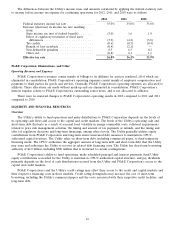

The differences between the Utility’s income taxes and amounts calculated by applying the federal statutory rate

to income before income tax expense for continuing operations for 2012, 2011, and 2010 were as follows:

2012 2011 2010

Federal statutory income tax rate ............... 35.0% 35.0% 35.0%

Increase (decrease) in income tax rate resulting

from:

State income tax (net of federal benefit) ........ (3.0) 1.6 1.0

Effect of regulatory treatment of fixed asset

differences ............................ (3.9) (4.2) (3.0)

Tax credits .............................. (0.6) (0.5) (0.4)

Benefit of loss carryback ................... (0.4) (2.1) —

Non deductible penalties ................... 0.5 6.3 0.2

Other, net .............................. (0.8) 0.1 1.1

Effective tax rate ........................... 26.8% 36.2% 33.9%

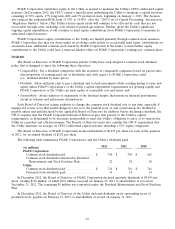

PG&E Corporation, Eliminations, and Other

Operating Revenues and Expenses

PG&E Corporation’s revenues consist mainly of billings to its affiliates for services rendered, all of which are

eliminated in consolidation. PG&E Corporation’s operating expenses consist mainly of employee compensation and

payments to third parties for goods and services. Generally, PG&E Corporation’s operating expenses are allocated to

affiliates. These allocations are made without mark-up and are eliminated in consolidation. PG&E Corporation’s

interest expense relates to PG&E Corporation’s outstanding senior notes, and is not allocated to affiliates.

There were no material changes to PG&E Corporation’s operating results in 2012 compared to 2011 and 2011

compared to 2010.

LIQUIDITY AND FINANCIAL RESOURCES

Overview

The Utility’s ability to fund operations and make distributions to PG&E Corporation depends on the levels of

its operating cash flows and access to the capital and credit markets. The levels of the Utility’s operating cash and

short-term debt fluctuate as a result of seasonal load, volatility in energy commodity costs, collateral requirements

related to price risk management activities, the timing and amount of tax payments or refunds, and the timing and

effect of regulatory decisions and long-term financings, among other factors. The Utility generally utilizes equity

contributions from PG&E Corporation and long-term senior unsecured debt issuances to maintain its CPUC-

authorized capital structure. The Utility relies on short-term debt, including commercial paper, to fund temporary

financing needs. The CPUC authorizes the aggregate amount of long-term debt and short-term debt that the Utility

may issue and authorizes the Utility to recover its related debt financing costs. The Utility has short-term borrowing

authority of $4.0 billion, including $500 million that is restricted to certain contingencies.

PG&E Corporation’s ability to fund operations, make scheduled principal and interest payments, fund Utility

equity contributions as needed for the Utility to maintain its CPUC-authorized capital structure, and pay dividends

primarily depends on the level of cash distributions received from the Utility and PG&E Corporation’s access to the

capital and credit markets.

PG&E Corporation’s and the Utility’s credit ratings may affect their access to the credit and capital markets and

their respective financing costs in those markets. Credit rating downgrades may increase the cost of short-term

borrowing, including the Utility’s commercial paper and the costs associated with their respective credit facilities, and

long-term debt.

16