Macy's 2012 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2012 Macy's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

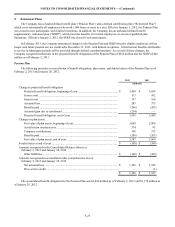

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

F-31

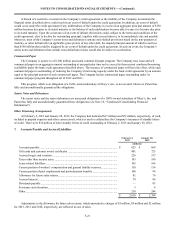

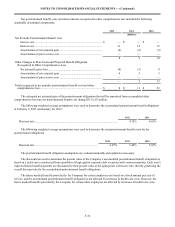

Net pension costs and other amounts recognized in other comprehensive loss for the supplementary retirement plan

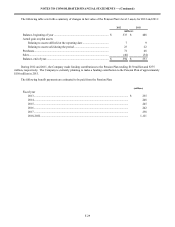

included the following actuarially determined components:

2012 2011 2010

(millions)

Net Periodic Pension Cost

Service cost.............................................................................................. $ 6 $ 6 $ 6

Interest cost.............................................................................................. 35 36 37

Amortization of net actuarial loss............................................................ 17 8 3

Amortization of prior service credit......................................................... (1)(1)(1)

57 49 45

Other Changes in Plan Assets and Projected Benefit Obligation

Recognized in Other Comprehensive Loss

Net actuarial loss...................................................................................... 34 90 22

Amortization of net actuarial loss............................................................ (17)(8)(3)

Amortization of prior service credit......................................................... 1 1 1

18 83 20

Total recognized in net periodic pension cost and

other comprehensive loss ............................................................................ $ 75 $ 132 $ 65

The estimated net actuarial loss for the supplementary retirement plan that will be amortized from accumulated other

comprehensive loss into net periodic benefit cost during 2013 is $19 million.

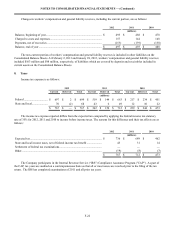

The following weighted average assumptions were used to determine the projected benefit obligations for the

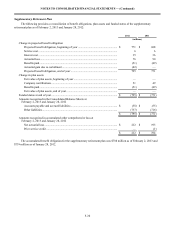

supplementary retirement plan at February 2, 2013 and January 28, 2012:

2012 2011

Discount rate............................................................................................................................... 4.15% 4.65%

Rate of compensation increases.................................................................................................. 4.90% 4.90%

The following weighted average assumptions were used to determine net pension costs for the supplementary retirement

plan:

2012 2011 2010

Discount rate ................................................................................................... 4.65% 5.40% 5.65%

Rate of compensation increases...................................................................... 4.90% 4.90% 4.90%

The supplementary retirement plan’s assumptions are evaluated annually and updated as necessary.

The discount rate used to determine the present value of the projected benefit obligation for the supplementary retirement

plan is based on a yield curve constructed from a portfolio of high quality corporate debt securities with various maturities.

Each year’s expected future benefit payments are discounted to their present value at the appropriate yield curve rate, thereby

generating the overall discount rate for the projected benefit obligation.

The Company develops its rate of compensation increase assumption on an age-graded basis based on recent experience

and reflects an estimate of future compensation levels taking into account general increase levels, seniority, promotions and

other factors. The salary increase assumption is used to project employees’ pay in future years and its impact on the projected

benefit obligation for the supplementary retirement plan.