Macy's 2012 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2012 Macy's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

F-14

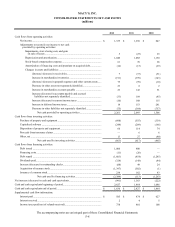

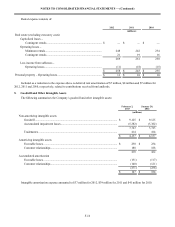

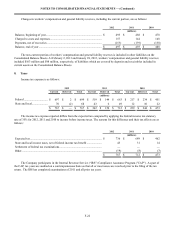

During January 2013, the Company announced the closure of six Macy's and Bloomingdale's stores; during January 2012,

the Company announced the closure of ten Macy's and Bloomingdale's stores; and during January 2011, the Company

announced the closure of three Macy’s stores. In connection with these announcements and the plans to dispose of these

locations, the Company incurred severance costs and other costs related to lease obligations and other store liabilities. For 2012,

these costs also included a gain on the sale of one property that was disposed in 2013 and for 2010 these costs also included a

loss on the sale of one property that was disposed in 2011.

As a result of the Company’s projected undiscounted future cash flows related to certain store locations being less than

the carrying value of those assets, the Company recorded the impairment charges reflected in the table above relating to

properties held and used, including properties that were the subject of announced store closings. The fair values of these

locations were calculated based on the projected cash flows and an estimated risk-adjusted rate of return that would be used by

market participants in valuing these assets or based on prices of similar assets.

During 2011, the Company recognized a gain on the sale of store leases related to the 2006 divestiture of Lord & Taylor,

partially offset by impairment charges and other costs and expenses related to store closings.

At January 28, 2012, the Company had $82 million of cash in a qualified escrow account related to the sale of store leases

discussed above, included in prepaid expenses and other current assets, which was utilized during 2012 for the purchase of two

parcels of the Macy's flagship Union Square location in San Francisco in tax deferred like-kind exchange transactions.

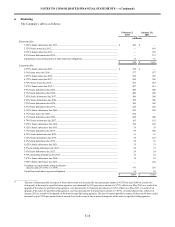

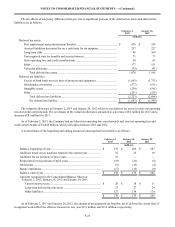

3. Receivables

Receivables were $371 million at February 2, 2013, compared to $368 million at January 28, 2012.

In connection with the sale of most of the Company's credit card accounts and related receivable balances to Citibank, the

Company and Citibank entered into a long-term marketing and servicing alliance pursuant to the terms of a Credit Card

Program Agreement (the “Program Agreement”) with an initial term of 10 years expiring on July 17, 2016 and, unless

terminated by either party as of the expiration of the initial term, an additional renewal term of three years. The Program

Agreement provides for, among other things, (i) the ownership by Citibank of the accounts purchased by Citibank, (ii) the

ownership by Citibank of new accounts opened by the Company’s customers, (iii) the provision of credit by Citibank to the

holders of the credit cards associated with the foregoing accounts, (iv) the servicing of the foregoing accounts, and (v) the

allocation between Citibank and the Company of the economic benefits and burdens associated with the foregoing and other

aspects of the alliance.

Pursuant to the Program Agreement, the Company continues to provide certain servicing functions related to the accounts

and related receivables owned by Citibank and receives compensation from Citibank for these services. The amounts earned

under the Program Agreement related to the servicing functions are deemed adequate compensation and, accordingly, no

servicing asset or liability has been recorded on the Consolidated Balance Sheets.

Amounts received under the Program Agreement were $865 million for 2012, $772 million for 2011 and $528 million for

2010, and are treated as reductions of SG&A expenses on the Consolidated Statements of Income. The Company’s earnings

from credit operations, net of servicing expenses, were $663 million for 2012, $582 million for 2011, and $332 million for

2010.