LinkedIn 2011 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2011 LinkedIn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

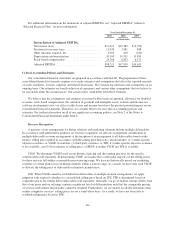

December 31, 2011. Although we believe our estimates are reasonable, no assurance can be given that the final

tax outcome of these matters will be the same as these estimates. These estimates are updated quarterly based on

factors such as change in facts or circumstances, changes in tax law, new audit activity, and effectively settled

issues.

We follow specific and detailed guidelines in each tax jurisdiction regarding the recoverability of any tax

assets recorded on the balance sheet and provide necessary valuation allowances as required. Future realization

of deferred tax assets ultimately depends on the existence of sufficient taxable income of the appropriate

character (for example, ordinary income or capital gain) within the carryback or carryforward periods available

under the tax law. We regularly review our deferred tax assets for recoverability based on historical taxable

income, projected future taxable income, the expected timing of the reversals of existing temporary differences

and tax planning strategies. Our judgments regarding future profitability may change due to many factors,

including future market conditions and our ability to successfully execute our business plans and/or tax planning

strategies. Should there be a change in our ability to recover our deferred tax assets, our tax provision would

increase or decrease in the period in which the assessment is changed.

Recently Issued Accounting Pronouncements

Fair Value Measurement

In May 2011, the Financial Accounting Standards Board (“FASB”) amended existing rules covering fair

value measurement and disclosure to clarify guidance and minimize differences between generally accepted

accounting principles (“GAAP”) in the United States of America and International Financial Reporting Standards

(“IFRS”). The new authoritative guidance requires entities to provide information about valuation techniques and

unobservable inputs used in Level 3 fair value measurements and provide a narrative description of the

sensitivity of Level 3 measurements to changes in unobservable inputs. The guidance will be effective for us on

January 1, 2012 and is not expected to have a material impact on our financial statements.

Comprehensive Income

In June 2011, the FASB issued new authoritative guidance on comprehensive income that eliminates the

option to present the components of other comprehensive income as part of the statement of shareholders’ equity.

Instead, we must report comprehensive income in either a single continuous statement of comprehensive income

which contains two sections, net income and other comprehensive income, or in two separate but consecutive

statements. In December 2011, the requirement regarding the presentation of reclassification adjustments out of

accumulated other comprehensive income was deferred indefinitely. The accounting update, except for the

provision deferred, is effective for us in our interim period ended March 31, 2012. The adoption of this guidance

will require us to change the presentation of comprehensive income and its components which we currently

report within the statements of redeemable convertible preferred stock, stockholders’ equity and comprehensive

income (loss).

Testing Goodwill for Impairment

In September 2011, the FASB issued new authoritative guidance that gives companies the option to make a

qualitative evaluation about the likelihood of goodwill impairment. Companies will be required to perform the

two-step impairment test only if it concludes that the fair value of a reporting unit is more likely than not, less

than its carrying value. The accounting update is effective for annual and interim goodwill impairment tests

performed for fiscal years beginning after December 15, 2011, with early adoption permitted. We adopted this

new authoritative guidance for our goodwill impairment test performed during the third quarter of 2011.

-50-