Konica Minolta 2005 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2005 Konica Minolta annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

|

|

43

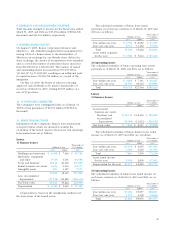

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Konica Minolta Holdings, Inc. and Consolidated Subsidiaries

For the fiscal years ended March 31, 2005 and 2004

1. BASIS OF PRESENTING FINANCIAL STATEMENTS

On April 1, 2003, the former Konica Corporation spun off

its operating activities and shifted to a holding company

structure. Shortly thereafter, Konica Minolta Holdings, Inc.

was established on August 5, 2003, through a share

exchange with Minolta Co., Ltd. For accounting purposes,

the integration with Minolta Co., Ltd. became effective

September 30, 2003. Accordingly, the consolidated financial

statements for the first six months of the year ended March

31, 2004 do not include the results of Minolta Co., Ltd.

The accompanying consolidated financial statements of

Konica Minolta Holdings, Inc. (the “Company”) and its

subsidiaries (together, referred to as the “Companies”) are

prepared on the basis of accounting principles generally

accepted in Japan, which are different in certain respects to

the application and disclosure requirements of International

Financial Reporting Standards, and are compiled from the

consolidated financial statements prepared by the Company

as required by the Securities and Exchange Law of Japan.

Certain items presented in the consolidated financial

statements submitted to the Director of Kanto Finance

Bureau in Japan have been reclassified for the convenience

of readers outside of Japan.

Certain amounts previously reported have been

reclassified to conform with the current year classifications.

As permitted under the Securities and Exchange Law of

Japan, amounts of less than one million yen have been

omitted. As a result, the totals shown in the accompanying

consolidated financial statements (both in yen and in

dollars) do not necessarily agree with the sums of the

individual amounts.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(a) Principles of Consolidation

The consolidated financial statements include the accounts

of the Company and, with certain exceptions which are

not material, those of its 122 subsidiaries in which it has

control. All significant intercompany transactions balances

and unrealized profits among the Companies are eliminated

in consolidation.

Investments in 13 unconsolidated subsidiaries and 2

significant affiliates are accounted for using the equity

method. Investments in 20 other unconsolidated

subsidiaries and 17 affiliates are stated at cost, since they

have no material effect on the consolidated financial

statements.

The excess of cost over the underlying investments in

subsidiaries is recognized as consolidation goodwill and is

amortized on a straight-line basis over a period not

exceeding 20 years.

(b) Translation of Foreign Currencies

Translation of Foreign Currency Transactions

All monetary assets and liabilities denominated in foreign

currencies, whether long-term or short-term, are translated

into Japanese yen at the exchange rates prevailing at the

balance sheet date and revenues and costs are translated

using the average exchange rate for the period.

Translation of Foreign Currency Financial Statements

The translations of foreign currency financial statements of

overseas consolidated subsidiaries and affiliates into

Japanese yen are made by applying the exchange rates

prevailing at the balance sheet dates for balance sheet

items, except common stock, additional paid-in capital and

retained earnings accounts, which are translated at the

historical rates, and the statements of income and retained

earnings are translated at average exchange rates.

(c) Cash and Cash Equivalents

Cash and cash equivalents in the consolidated statements

of cash flows consist of cash on hand, bank deposits able

to be withdrawn on demand and short-term investments

with an original maturity of three months or less, which

represent a minor risk of fluctuation in value.

(d) Allowance for Doubtful Accounts

The allowance for doubtful accounts is provided at the

amount of possible losses from uncollectible receivables

based on the management’s estimate.

(e) Inventories

The Company and its domestic consolidated subsidiaries

inventories are, in the main, recorded at cost as determined

by the periodic-average method. Overseas consolidated

subsidiaries’ inventories are recorded at the lower of cost or

market value, with cost determined by the first-in, first-out.

(f) Property, Plant and Equipment

Depreciation of property, plant and equipment for the

Company and domestic consolidated subsidiaries is

computed using the declining balance method, except for

depreciation of buildings acquired after April 1, 1998, based

on the estimated useful lives of assets.

Depreciation of buildings acquired after April 1, 1998 is

computed using the straight-line method. Depreciation for

foreign subsidiaries is computed using the straight-line

method.

Ordinary maintenance and repairs are charged to

income as incurred. Major replacements and improvements

are capitalized. When properties are retired or otherwise

disposed of, the property and related accumulated depre-

ciation accounts are relieved of the applicable amounts and

any differences are charged or credited to income.

(g) Accounting Standard for Impairment

of Fixed Assets

On August 9, 2002, the Business Accounting Council in

Japan issued “Opinion on Establishment of Asset-

Impairment Accounting Standards,” which requires that

certain fixed assets be reviewed for impairment whenever

events or changes in circumstances indicate that the carrying

amount of an asset may not be recoverable. If the criterion

for impairment recognition is met, an impairment loss as

the difference between the carrying amount and the higher

of net discounted future cash flows or market value of the

asset shall be recognized in the consolidated statements of

income. In the case of the Company, this standard shall be