Kia 2010 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2010 Kia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

|

|

2. Basis of Presenting Financial Statements and Summary of Significant Accounting Policies

(a) Basis of Presenting Financial Statements

Kia Motors Corporation and subsidiaries (collectively the “Company”) maintains its accounting records in Korean won and prepares

statutory consolidated financial statements in the Korean language in conformity with accounting principles generally accepted in the

Republic of Korea. Certain accounting principles applied by the Company that conform with financial accounting standards and accounting

principles in the Republic of Korea may not conform with generally accepted accounting principles in other countries. Accordingly, these

accompanying consolidated financial statements are intended solely for use by only those who are informed in Korean accounting principles

and practices. The accompanying consolidated financial statements have been condensed, restructured and translated into English from

the Korean language consolidated financial statements.

Certain information included in the Korean language consolidated financial statements, but not required for a fair presentation of the

Company’s financial position, results of operations, cash flows, or change in equity is not presented in the accompanying consolidated

financial statements.

The Company prepares the consolidated financial statements in accordance with generally accepted accounting principles in the Republic of

Korea. Except for the items explained in note 29 related to accounting changes, the Company applied the same accounting policies that

were adopted in the previous year’s consolidated financial statements.

(b) Revenue Recognition

Revenue from the sale of motor vehicles and parts is measured at the fair value of the consideration received or receivable, net of

discounts. Revenue is recognized when the significant risks and rewards of ownership have been transferred to the buyer, recovery of the

consideration is probable, the associated costs and possible return of goods can be estimated reliably, and there is no continuing

management involvement with the goods; generally upon delivery to end customer. Revenue from other than the sale of vehicles and parts

is recognized when the Company’s revenue-earning activities have been substantially completed, the amount of revenue can be measured

reliably, and it is probable that the economic benefits associated with the transaction will flow to the Company.

Long-term installment sales are recognized at the time of shipment of motor vehicles and parts when the significant risks and rewards of

ownership have been transferred to buyer. Interest income arising from long-term installment sales contracts is recognized using the level

yielding method.

(c) Allowance for Doubtful Accounts

Allowance for doubtful accounts is estimated based on an analysis of individual accounts and past experience of collection and presented

as a deduction from trade receivables.

When the principals, interest rates, and terms of trade accounts and notes receivable are modified, either through a court order, such as

a reorganization, or by mutual formal agreement, resulting in a reduction in the present value of the future cash flows due to the Company,

the difference between the carrying value of the relevant accounts and notes receivable and the present value of the future cash flows is

recognized as bad debt expense.

(d) Inventories

Inventories are stated at the lower of cost or net realizable value. Net realizable value is the estimated selling price in the ordinary course

of business, less the estimated selling costs. The cost of inventories is determined on the specific identification method for materials-in-

transit and on the moving-average method for all other inventories. Amounts of inventory written down to net realizable value due to losses

occurring in the normal course of business are recognized as cost of goods sold and are deducted as an allowance from the carrying value

of inventories.

(e) Investments in Securities (excluding in associates and joint ventures)

Classification

Upon acquisition, the Company classifies certain debt and equity securities (excluding in associates and joint ventures) into the following

categories: held-to-maturity, available-for-sale or trading securities.

Investments in debt securities where the Company has the positive intent and ability to hold to maturity are classified as held-to-maturity.

Securities that are acquired principally for the purpose of selling in the short term are classified as trading securities. Investments not

classified as either held-to-maturity or trading securities are classified as available-for-sale securities.

Initial recognition

Investments in securities (excluding in associates and joint ventures) are initially recognized at cost.

Subsequent measurement and income recognition

Trading securities are subsequently carried at fair value. Gains and losses arising from changes in the fair value of trading securities are

included in the statement of income in the period in which they arise. Available-for-sale securities are subsequently carried at fair value.

Gains and losses arising from changes in the fair value of available-for-sale securities are recognized as accumulated other comprehensive

income, net of tax, directly in equity. Investments in available-for-sale securities that do not have readily determinable fair values are

recognized at cost less impairment, if any. Held-to-maturity investments are carried at amortized cost with interest income and expense

recognized in the statement of income using the effective interest method.

Fair value information

The fair value of marketable securities is determined using quoted market prices as of the period end. Non-marketable debt securities are

fair valued by discounting cash flows using the prevailing market rates for debt with a similar credit risk and remaining maturity. Credit risk

is determined using the Company’s credit rating as announced by accredited credit rating agencies in Korea. The fair value of investments

in money market funds is determined by investment management companies.

Presentation

Trading securities, available-for-sale securities which mature within one year from the end of the reporting period or where the likelihood of

disposal within one year from the end of the reporting period is probable, held-to-maturity securities which mature within one year from

end of the reporting period, short-term deposits and short-term loans are combined and presented as current assets. All other available-for-

sale securities and held-to-maturity securities are combined and presented as long-term investments.

Impairment

The Company reviews investments in securities whenever events or changes in circumstances indicate that the carrying amount of the

investments may not be recoverable. Impairment losses are recognized when the reasonably estimated recoverable amounts are less than

the carrying amount and it is not obviously evidenced that impairment is unnecessary.

An impairment loss is reversed if the reversal can be related objectively to an event occurring after the impairment loss was recognized and

a reversal of an impairment loss shall not exceed the carrying amount that would have been determined (net of amortization or depreciation)

had no impairment loss been recognized in the asset in prior years. For financial assets measured at amortized cost and available-for-sale

assets that are debt securities, the reversal is recognized in profit or loss. For available-for-sale financial assets that are equity securities,

the reversal is recognized directly in equity.

(f) Investments in Associates

Associates are entities of the Company and its subsidiaries that have the ability to significantly influence the financial and operating policies.

It is presumed to have significant influence if the Company holds directly or indirectly 20 percent or more of the voting power unless it can

be clearly demonstrated that this is not the case.

Investments in associates are accounted for by using the equity method of accounting and are initially recognized at cost.

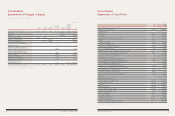

Notes to Consolidated

Financial Statements

December 31, 2010 and 2009

62 COMPONENTS OF SUSTAINABLE GROWTH 63

KIA MOTORS ANNUAL REPORT 2010