Home Depot 2009 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2009 Home Depot annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

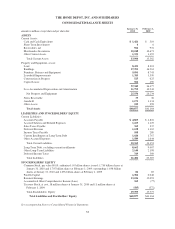

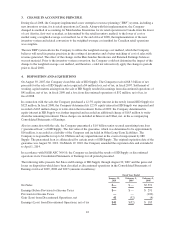

3. CHANGE IN ACCOUNTING PRINCIPLE

During fiscal 2008, the Company implemented a new enterprise resource planning (“ERP”) system, including a

new inventory system, for its retail operations in Canada. Along with this implementation, the Company

changed its method of accounting for Merchandise Inventories for its retail operations in Canada from the lower

of cost (first-in, first-out) or market, as determined by the retail inventory method, to the lower of cost or

market using a weighted-average cost method. As of the end of fiscal 2008, the implementation of the new

inventory system and related conversion to the weighted-average cost method for Canadian retail operations

was complete.

The new ERP system allows the Company to utilize the weighted-average cost method, which the Company

believes will result in greater precision in the costing of inventories and a better matching of cost of sales with

revenue generated. The effect of the change on the Merchandise Inventories and Retained Earnings balances

was not material. Prior to the inventory system conversion, the Company could not determine the impact of the

change to the weighted-average cost method, and therefore, could not retroactively apply the change to periods

prior to fiscal 2008.

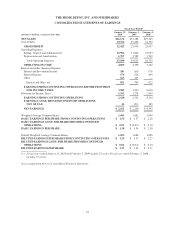

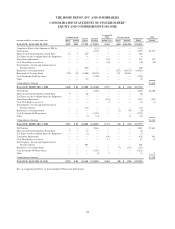

4. DISPOSITION AND ACQUISITIONS

On August 30, 2007, the Company closed the sale of HD Supply. The Company received $8.3 billion of net

proceeds for the sale of HD Supply and recognized a $4 million loss, net of tax, in fiscal 2007. Settlement of

working capital matters arising from the sale of HD Supply resulted in earnings from discontinued operations of

$41 million, net of tax, in fiscal 2009 and a loss from discontinued operations of $52 million, net of tax, in

fiscal 2008.

In connection with the sale, the Company purchased a 12.5% equity interest in the newly formed HD Supply for

$325 million. In fiscal 2008, the Company determined its 12.5% equity interest in HD Supply was impaired and

recorded a $163 million charge to write-down the investment. In fiscal 2009, the Company determined its

equity interest in HD Supply was further impaired and recorded an additional charge of $163 million to write-

down the remaining investment. These charges are included in Interest and Other, net, in the accompanying

Consolidated Statements of Earnings.

Also in connection with the sale, the Company guaranteed a $1.0 billion senior secured amortizing term loan

(“guaranteed loan”) of HD Supply. The fair value of the guarantee, which was determined to be approximately

$16 million, is recorded as a liability of the Company and included in Other Long-Term Liabilities. The

Company is responsible for up to $1.0 billion and any unpaid interest in the event of nonpayment by HD

Supply. The guaranteed loan is collateralized by certain assets of HD Supply. The original expiration date of the

guarantee was August 30, 2012. On March 19, 2010, the Company amended the expiration date and extended it

to April 1, 2014.

In accordance with FASB ASC 360-10, the Company reclassified the results of HD Supply as discontinued

operations in its Consolidated Statements of Earnings for all periods presented.

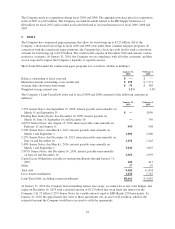

The following table presents Net Sales and Earnings of HD Supply through August 30, 2007 and the gains and

losses on disposition which have been classified as discontinued operations in the Consolidated Statements of

Earnings for fiscal 2009, 2008 and 2007 (amounts in millions):

Fiscal Year Ended

January 31,

2010 February 1,

2009 February 3,

2008

Net Sales $— $ — $7,391

Earnings Before Provision for Income Taxes $— $ — $ 291

Provision for Income Taxes —— (102)

Gain (Loss) from Discontinued Operations, net 41 (52) (4)

Earnings (Loss) from Discontinued Operations, net of tax $41 $(52) $ 185

42