Frontier Communications 2006 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2006 Frontier Communications annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

|

|

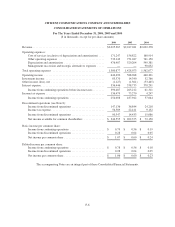

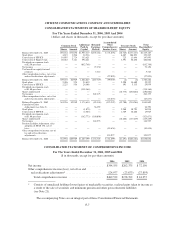

CITIZENS COMMUNICATIONS COMPANY AND SUBSIDIARIES

Notes to Consolidated Financial Statements

(2) RECENT ACCOUNTING LITERATURE AND CHANGES IN ACCOUNTING PRINCIPLES:

Accounting for Defined Benefit Pension and Other Postretirement Plans

In October 2006, the FASB issued SFAS No. 158, “Employers’ Accounting for Defined Benefit Pension

and Other Postretirement Plans” (OPEB), which completes the first phase of a FASB project that will

comprehensively reconsider accounting for pensions and other postretirement benefit plans and amends the

following FASB Statements:

• SFAS No. 87, “Employers’ Accounting for Pensions;”

• SFAS No. 88, “Employers’ Accounting for Settlements and Curtailments of Defined Benefit Pension

Plans and for Termination Benefits;”

• SFAS No. 106, “Employers’ Accounting for Postretirement Benefits Other Than Pensions;” and

• SFAS No. 132(R), “Employers’ Disclosures about Pensions and Other Postretirement Benefits.”

SFAS No. 158 requires (1) recognition of the funded status of a benefit plan in the balance sheet,

(2) recognition in other comprehensive income of gains or losses and prior service costs or credits arising during the

period but which are not included as components of periodic benefit cost, (3) measurement of defined benefit plan

assets and obligations as of the balance sheet date, and (4) disclosure of additional information about the effects on

periodic benefit cost for the following fiscal year arising from delayed recognition in the current period.

For public companies, the requirements to recognize the funded status of a plan and to comply with the

disclosure provisions of SFAS No. 158 are effective as of the end of the fiscal year that ends after December 15,

2006. The requirement to measure plan assets and benefit obligations as of the balance sheet date is effective for

fiscal years ending after December 15, 2008. See Note 24.

Consideration of Prior Years’ Errors in Quantifying Current Year Misstatements

In September 2006, the SEC issued Staff Accounting Bulletin (SAB) No. 108, “Consideration of Prior

Years’ Errors in Quantifying Current Year Misstatements.” SAB No. 108 provides guidance concerning the

process to be applied in considering the impact of prior years’ errors in quantifying misstatements in the current

year. SAB No. 108 is effective for periods ending after November 15, 2006. The Company adopted SAB No. 108

in the fourth quarter of 2006. See Note 5.

Accounting for Uncertainty in Income Taxes

In July 2006, the FASB issued FASB Interpretation No. (FIN) 48, “Accounting for Uncertainty in Income

Taxes.” Among other things, FIN No. 48 requires applying a “more likely than not” threshold to the recognition

and derecognition of uncertain tax positions. FIN No. 48 is effective for fiscal years beginning after

December 15, 2006. We do not expect the adoption of FIN No. 48 to have a material impact on our financial

position, results of operations or cash flows.

How Taxes Collected from Customers and Remitted to Governmental Authorities should be presented in

the Income Statement

In June 2006, the FASB issued EITF Issue No. 06-3, “How Taxes Collected from Customers and Remitted

to Governmental Authorities Should be Presented in the Income Statement” (EITF No. 06-3), which requires

disclosure of the accounting policy for any tax assessed by a governmental authority that is directly imposed on a

revenue-producing transaction, that is Gross versus Net presentation. EITF No. 06-3 is effective for periods

beginning after December 15, 2006. We will adopt the disclosure requirements of EITF No. 06-3 commencing

January 1, 2007.

F-13