Experian 2013 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2013 Experian annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

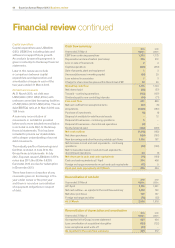

Accounting policies and developments

The principal accounting policies

used are shown in note 5 to the Group

financial statements and these have

been applied consistently.

Two significant strategic transactions

have been completed during the

year – the acquisition of the further

29.6% interest in Serasa and the sale

of the comparison shopping and lead

generation businesses. The treatment

of these transactions is detailed in notes

46 and 47 respectively to the Group

financial statements and is consistent

with both previously adopted policies for

such transactions and with International

Financial Reporting Standards (‘IFRS’).

The year under review has seen little

impact on the Group from developments

in IFRS but the Group is adopting IAS 19

(revised) with effect from 1 April 2013. The

results for the year ended 31 March 2013

will be re-presented accordingly in the

annual report for the year ending 31 March

2014 and it is anticipated that there will be

a small reduction in reported profit before

tax for the year ended 31 March 2013 as

the rate used to determine the expected

return on pension plan assets will fall.

Accounting estimates and assumptions

Details of critical accounting estimates

and assumptions are shown in note 6(a) to

the Group financial statements. The most

significant of these relate to tax, pension

benefits and goodwill and the key

features can be summarised as follows:

•Estimates made in respect of tax assets

and liabilities include the consideration

of transactions in the ordinary course

of business for which the ultimate tax

determination is uncertain.

•The recognition of pension benefits

involves the selection of appropriate

actuarial assumptions, changes to which

may impact on the amounts disclosed in

the Group financial statements.

•The assumptions used in the cash

flow projections underpinning the

impairment testing of goodwill include

assumptions in respect of profitability

and future growth, together with

pre-tax discount rates specific to the

Group’s operating segments.

Financial risk management

The risks and uncertainties that are specific

to our business, together with more general

risks, are set out in the protecting our

business section of this report. Our financial

risk management continues to focus on

the unpredictability of financial markets

and seeks to minimise potentially adverse

effects on our financial performance.

We seek to reduce exposures to foreign

exchange, interest rate and other

financial risks. Detailed narrative and

numeric disclosures in respect of such

risks are included in the notes to the

Group financial statements and the key

features are summarised below.

Foreign exchange risk is managed by:

•Entering into forward foreign exchange

contracts in the relevant currencies in

respect of investments in entities with

functional currencies other than US

dollars, whose net assets are exposed

to foreign exchange translation risk;

•Swapping the proceeds of certain bonds

issued in sterling and euros into US dollars;

•Denominating internal loans in relevant

currencies to match the currencies of

assets and liabilities in entities with

different functional currencies; and

•Using forward foreign exchange

contracts for certain future

commercial transactions.

Interest rate risk is managed by:

•Using both fixed and floating rate

borrowings;

•Using interest rate swaps to adjust

the balance of fixed and floating rate

liabilities; and

•Mixing the duration of borrowings

and interest rate swaps to smooth the

impact of interest rate fluctuations.

Credit risk is managed by:

•Dealing only with banks and financial

institutions with strong credit ratings,

within limits set for each organisation; and

•Closely controlling dealing activity

with counterparty positions monitored

regularly.

Liquidity risk is managed by:

•Entering into long-term committed

bank borrowing facilities to ensure

that sufficient funds are available for

operations and planned expansion; and

•Monitoring of rolling forecasts of

projected cash flows to ensure

that adequate undrawn committed

facilities are available.

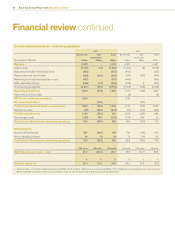

2012 NET FUNDING BY CURRENCY2013 NET FUNDING BY CURRENCY

2012 EBIT BY CURRENCY2013 EBIT BY CURRENCY

2012 NET FUNDING BY INTEREST RATE2013 NET FUNDING BY INTEREST RATE

Financial review continued

US dollar 56%

Brazilian real 27%

Sterling 10%

Other 7%

US dollar 57%

Brazilian real 26%

Sterling 10%

Other 7%

US dollar 76%

Sterling 17%

Euro 4%

Other 3%

US dollar 79%

Sterling 16%

Euro 1%

Other 4%

Fixed 69%

Floating 31%

Fixed 76%

Floating 24%

48 Experian Annual Report 2013 Business review