Dish Network 2012 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2012 Dish Network annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

|

|

Item 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS - Continued

56

56

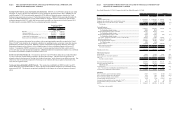

DISH added approximately 78,000 net broadband subscribers during the year ended December 31, 2012 compared

to a loss of approximately 5,000 net broadband subscribers during the same period in 2011. This increase versus the

same period in 2011 primarily resulted from higher gross new broadband subscriber activations driven by increased

advertising associated with the launch of the dishNET branded broadband services. During the year ended

December 31, 2012, DISH added approximately 121,000 gross new broadband subscribers compared to 30,000

gross new broadband subscribers during the same period in 2011. A significant percentage of these activations were

in the fourth quarter 2012, driven by increased advertising associated with the launch of the dishNET branded

broadband services. During the fourth quarter 2012, we added approximately 57,000 gross new broadband

subscribers. Broadband services revenue was $95 million for the year ended December 31, 2012, 0.7% of our total

“Subscriber-related revenue.”

“Net income (loss) attributable to DISH Network” for the year ended December 31, 2012 was $637 million,

compared to $1.516 billion for the same period in 2011. During the year ended December 31, 2012, “Net income

(loss) attributable to DISH Network” decreased primarily due to $730 million of litigation expense related to the

Voom Settlement Agreement, higher subscriber-related expenses primarily from higher programming costs,

increased advertising associated with our Hopper set-top box and the reversal of our accrued expenses related to the

TiVo Inc. settlement during 2011. This decrease was partially offset by the non-cash gain of $99 million related to

the conversion of our DBSD North America 7.5% Convertible Senior Secured Notes due 2009 in connection with the

completion of the DBSD Transaction. See Note 10 in the Notes to the Consolidated Financial Statements in Item 15

of this Annual Report on Form 10-K.

Our ability to compete successfully will depend on, among other things, our ability to continue to obtain desirable

programming and deliver it to our subscribers at competitive prices. Programming costs represent a large percentage of

our “Subscriber-related expenses” and the largest component of our total expense. We expect these costs to continue to

increase, especially for local broadcast channels and sports programming. Going forward, our margins may face

pressure if we are unable to renew our long-term programming contracts on favorable pricing and other economic

terms. In addition, increases in programming costs could cause us to increase the rates that we charge our subscribers,

which could in turn cause our existing Pay-TV subscribers to disconnect our service or cause potential new Pay-TV

subscribers to choose not to subscribe to our service. Additionally, our gross new Pay-TV subscriber activations and

Pay-TV subscriber churn rate may be negatively impacted if we are unable to renew our long-term programming

contracts before they expire or if we lose access to programming as a result of disputes with programming suppliers.

As the pay-TV industry has matured, we and our competitors increasingly must seek to attract a greater proportion

of new subscribers from each other’s existing subscriber bases rather than from first-time purchasers of pay-TV

services. Some of our competitors have been especially aggressive by offering discounted programming and

services for both new and existing subscribers. In addition, programming offered over the Internet has become more

prevalent as the speed and quality of broadband networks have improved. Significant changes in consumer behavior

with regard to the means by which they obtain video entertainment and information in response to digital media

competition could materially adversely affect our business, results of operations and financial condition or otherwise

disrupt our business.

While economic factors have impacted the entire pay-TV industry, our relative performance has also been driven by

issues specific to DISH. In the past, our Pay-TV subscriber growth has been adversely affected by signal theft and

other forms of fraud and by operational inefficiencies at DISH. To combat signal theft and improve the security of

our broadcast system, we completed the replacement of our Security Access Devices to re-secure our system during

2009. We expect that additional future replacements of these devices will be necessary to keep our system secure.

To combat other forms of fraud, we continue to expect that our third party distributors and retailers will adhere to

our business rules.

While we have made improvements in responding to and dealing with customer service issues, we continue to focus

on the prevention of these issues, which is critical to our business, financial position and results of operations. We

implemented a new billing system as well as new sales and customer care systems in the first quarter 2012. To

improve our operational performance, we continue to make significant investments in staffing, training, information

systems, and other initiatives, primarily in our call center and in-home service operations. These investments are

intended to help combat inefficiencies introduced by the increasing complexity of our business, improve customer

Item 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS - Continued

57

57

satisfaction, reduce churn, increase productivity, and allow us to scale better over the long run. We cannot,

however, be certain that our spending will ultimately be successful in improving our operational performance.

We have been deploying receivers that utilize 8PSK modulation technology and receivers that utilize MPEG-4

compression technology for several years. These technologies, when fully deployed, will allow more programming

channels to be carried over our existing satellites. Many of our customers today, however, do not have receivers that

use MPEG-4 compression and a smaller but still significant number of our customers do not have receivers that use

8PSK modulation. We may choose to invest significant capital to accelerate the conversion of customers to MPEG-

4 and/or 8PSK to realize the bandwidth benefits sooner. In addition, given that all of our HD content is broadcast in

MPEG-4, any growth in HD penetration will naturally accelerate our transition to these newer technologies and may

increase our subscriber acquisition and retention costs. All new receivers that we purchase from EchoStar have

MPEG-4 technology. Although we continue to refurbish and redeploy MPEG-2 receivers, as a result of our HD

initiatives and current promotions, we currently activate most new customers with higher priced MPEG-4

technology. This limits our ability to redeploy MPEG-2 receivers and, to the extent that our promotions are

successful, will accelerate the transition to MPEG-4 technology, resulting in an adverse effect on our acquisition

costs per new subscriber activation.

From time to time, we change equipment for certain subscribers to make more efficient use of transponder capacity

in support of HD and other initiatives. We believe that the benefit from the increase in available transponder

capacity outweighs the short-term cost of these equipment changes.

To maintain and enhance our competitiveness over the long term, we introduced the Hopper set-top box, that allows,

among other things, recorded programming to be viewed in HD in multiple rooms. During the second quarter 2012,

the four major broadcast television networks filed lawsuits against us alleging, among other things, that the

PrimeTime Anytime and AutoHop features of the Hopper set-top box infringe their copyrights. In the event a court

ultimately determines that we infringe the asserted copyrights, we may be subject to, among other things, an

injunction that could require us to materially modify or cease to offer these features. See Note 16 in the Notes to the

Consolidated Financial Statements in Item 15 of this Annual Report on Form 10-K for further information. We

recently introduced the Hopper set-top box with Sling, which promotes a suite of integrated products designed to

maximize the convenience and ease of watching TV anytime and anywhere, which we refer to as DISH Anywhere™

that utilizes, among other things, online access and Slingbox “placeshifting” technology. In addition, the Hopper

with Sling has several innovative features which allows customers to watch and record television programming

through certain tablet computers and combines program-discovery tools, social media engagement and remote-

control capabilities through the use of certain tablet computers. There can be no assurance that these integrated

products will positively affect our results of operations or our gross new subscriber activations.

Blockbuster

On April 26, 2011, we completed the Blockbuster Acquisition for a net purchase price of $234 million. This

transaction was accounted for as a business combination and therefore the purchase price was allocated to the assets

acquired based on their estimated fair value. Blockbuster primarily offers movies and video games for sale and

rental through multiple distribution channels such as retail stores, by-mail, the blockbuster.com website and the

BLOCKBUSTER On Demand service. The Blockbuster Acquisition is intended to complement our core business

of delivering high-quality video entertainment to consumers. We are promoting our new Blockbuster offerings

including the Blockbuster@Home™ service which provides movies, games and TV shows through Internet

streaming, mail and in-store exchanges and online. This offering is only available to DISH subscribers.

Blockbuster operations are included in our financial results beginning April 26, 2011. During the year ended

December 31, 2012, Blockbuster operations contributed $1.088 billion in revenue with a $35 million operating loss

compared to $975 million in revenue and $1 million in operating loss for the same period in 2011. The operating

loss during the year ended December 31, 2012 was impacted by a charge of $21 million to “Cost of sales -

equipment, merchandise, services, rental and other” as a result of the Blockbuster UK Administration, discussed

below. In addition, this operating loss resulted from lower monthly revenue and higher inventory costs per unit

relative to the fair value of the inventory costs per unit acquired in the Blockbuster Acquisition, partially offset by

the benefit from the sale of inventory from domestic retail stores that were closed primarily during the first half of

2012. During 2012, we closed approximately 700 domestic retail stores, leaving us with approximately 800