Cincinnati Bell 2008 Annual Report Download - page 140

Download and view the complete annual report

Please find page 140 of the 2008 Cincinnati Bell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

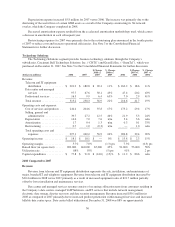

Technical Bulletin No. 90-1, “Accounting for Separately Priced Extended Warranty and Product Maintenance

Contracts,” and is deferred and recognized ratably over the term of the underlying customer contract.

Products — The Company recognizes equipment revenue upon the completion of contractual obligations,

such as shipment, delivery, installation, or customer acceptance. Wireless handset revenue and the related

activation revenue are recognized when the products are delivered to and accepted by the customer, as this is

considered to be a separate earnings process from the sale of wireless services. Wireless equipment costs are also

recognized upon handset sale and are in excess of the related handset and activation revenue.

The Company is a reseller of IT and telephony equipment and considers the criteria of Emerging Issues

Task Force (“EITF”) 99-19, “Reporting Revenue Gross as a Principal versus Net as an Agent,” when recording

revenue, such as title transfer, risk of product loss, and collection risk. Based on this guidance, these equipment

revenues and associated costs have generally been recorded on a gross basis, rather than recording the revenues

net of the associated costs. The Company benefits from vendor rebate plans, particularly rebates on hardware

sold by Technology Solutions. If the rebate is earned and the amount determinable based on the sale of the

product, the Company recognizes the rebate as an offset to costs of products sold upon sale of the related

equipment to the customer.

With respect to arrangements with multiple deliverables, the Company follows the guidance in EITF 00-21,

“Revenue Arrangements with Multiple Deliverables,” to determine whether more than one unit of accounting

exists in an arrangement. To the extent that the deliverables are separable into multiple units of accounting, total

consideration is allocated to the individual units of accounting based on their relative fair value, determined by

the price of each deliverable when it is regularly sold on a stand-alone basis. Revenue is recognized for each unit

of accounting as delivered or as service is performed depending on the nature of the deliverable comprising the

unit of accounting.

The Company often is contracted to install the IT equipment that it sells. The revenue recognition guidance

in Statement of Position (“SOP”) 97-2, “Software Revenue Recognition,” is applied, which requires vendor

specific objective evidence (“VSOE”) in order to recognize the IT equipment separate from the installation. The

Company has customers to which it sells IT equipment without the installation service, customers to which it

provides installation services without the IT equipment, and also customers to which it provides both the IT

equipment and the installation service. As such, the Company has VSOE that permits the separation of the IT

equipment from the installation services. The Company recognizes the IT equipment revenue upon completion of

its contractual obligations, generally upon delivery of the IT equipment to the customer, and recognizes

installation service revenue upon completion of the installation.

Pricing of local voice services is generally subject to oversight by both state and federal regulatory

commissions. Such regulation also covers services, competition, and other public policy issues. Various

regulatory rulings and interpretations could result in increases or decreases to revenue in future periods.

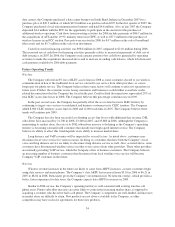

Accounting for Allowances for Uncollectible Accounts Receivable — The Company established the

allowances for uncollectible accounts using percentages of aged accounts receivable balances to reflect the

historical average of credit losses as well as specific provisions for certain identifiable, potentially uncollectible

balances. The Company believes its allowance for uncollectible accounts is adequate based on these methods, as

the Company has not had unfavorable experience with its estimation methods. However, if one or more of the

Company’s larger customers were to default on its accounts receivable obligations or if general economic

conditions in the Company’s operating area further deteriorated, the Company could be exposed to potentially

significant losses in excess of the provisions established. Substantially all of the Company’s outstanding accounts

receivable balances are with entities located within its geographic operating areas. Regional and national

telecommunications companies account for the remainder of the Company’s accounts receivable balances. The

Company has one large customer with receivables that represent 10% of the Company’s outstanding accounts

receivable balances.

Reviewing the Carrying Values of Goodwill and Indefinite-Lived Intangible Assets — Pursuant to

Statement of Financial Accounting Standards (“SFAS”) No. 142, “Goodwill and Other Intangible Assets,”

goodwill and intangible assets not subject to amortization are tested for impairment annually or when events or

changes in circumstances indicate that the asset might be impaired.

40