CVS 2005 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2005 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

|

|

Our credit facilities and unsecured senior notes contain customary restrictive financial and operating

covenants. These covenants do not include a requirement for the acceleration of our debt maturities in

the event of a downgrade in our credit rating. We do not believe that the restrictions contained in these

covenants materially affect our financial or operating flexibility.

Our liquidity is based, in part, on maintaining investment-grade debt ratings. As of December 31, 2005,

our long-term debt was rated “A3” by Moody’s and “A-” by Standard & Poor’s, and our commercial paper

program was rated “P-2” by Moody’s and “A-2” by Standard & Poor’s. In assessing our credit strength,

we believe that both Moody’s and Standard & Poor’s considered, among other things, our capital structure

and financial policies as well as our consolidated balance sheet and other financial information. Our debt

ratings have a direct impact on our future borrowing costs, access to capital markets and new store

operating lease costs. Subsequent to our entry into the definitive agreement with Albertson’s in January

2006, Standard & Poor’s placed our long-term debt on a negative outlook, while Moody’s placed all our

ratings under review for possible downgrade. While a downgrade is possible, our long-term debt ratings

are expected to remain investment grade.

Off-Balance Sheet Arrangements

In connection with executing operating leases, we provide a guarantee of the lease payments. We finance a

portion of our new store development through sale-leaseback transactions, which involve selling stores to

unrelated parties and then leasing the stores back under leases that qualify and are accounted for as operating

leases. We do not have any retained or contingent interests in the stores, nor do we provide any guarantees,

other than a guarantee of the lease payments, in connection with the transactions. In accordance with generally

accepted accounting principles, our operating leases are not reflected in our consolidated balance sheet.

Between 1991and 1997, we sold or spun off a number of subsidiaries, including Bob’s Stores, Linens

’n Things, Marshalls, Kay-Bee Toys, Wilsons, This End Up and Footstar. In many cases, when a former

subsidiary leased a store, we provided a guarantee of the store’s lease obligations. When the subsidiaries

were disposed of, the guarantees remained in place, although each initial purchaser agreed to indemnify us

for any lease obligations we were required to satisfy. If any of the purchasers were to become insolvent and

failed to make the required payments under a store lease, we could be required to satisfy these obligations.

Assuming that each respective purchaser became insolvent, and we were required to assume all of these

lease obligations, we estimate that we could settle the obligations for approximately $400 to $450 million

as of December 31, 2005. As of December 31, 2005, we guaranteed approximately 360 such store leases,

with the maximum remaining lease term extending through 2018.

We currently believe that the ultimate disposition of any of the lease guarantees will not have a material

adverse effect on our consolidated financial condition, results of operations or future cash flows.

Critical Accounting Policies

We prepare our consolidated financial statements in conformity with generally accepted accounting

principles, which require management to make certain estimates and apply judgment. We base our

estimates and judgments on historical experience, current trends and other factors that management

believes to be important at the time the consolidated financial statements are prepared. On a regular basis,

we review our accounting policies and how they are applied and disclosed in our consolidated financial

statements. While we believe that the historical experience, current trends and other factors considered

support the preparation of our consolidated financial statements in conformity with generally accepted

accounting principles, actual results could differ from our estimates, and such differences could be material.

Our significant accounting policies are discussed in Note 1to our consolidated financial statements. We

believe the following accounting policies include a higher degree of judgment and/or complexity and, thus,

are considered to be critical accounting policies. The critical accounting policies discussed below are

applicable to both of our business segments. We have discussed the development and selection of our

critical accounting policies with the Audit Committee of our Board of Directors and the Audit Committee has

reviewed our disclosures relating to them.

Impairment of Long-Lived Assets

We account for the impairment of long-lived assets in accordance with Statement of Financial Accounting

Standards (“SFAS”) No. 144, “Accounting for Impairment or Disposal of Long-Lived Assets.” As such, we

evaluate the recoverability of long-lived assets, including intangible assets with finite lives, but excluding

goodwill, which is tested for impairment using a separate test, whenever events or changes in circumstances

indicate that the carrying value of an asset may not be recoverable. We group and evaluate long-lived

assets for impairment at the individual store level, which is the lowest level at which individual cash flows

21

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

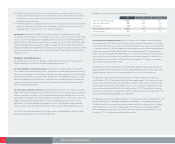

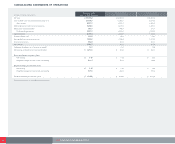

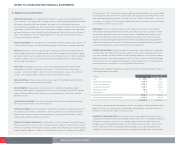

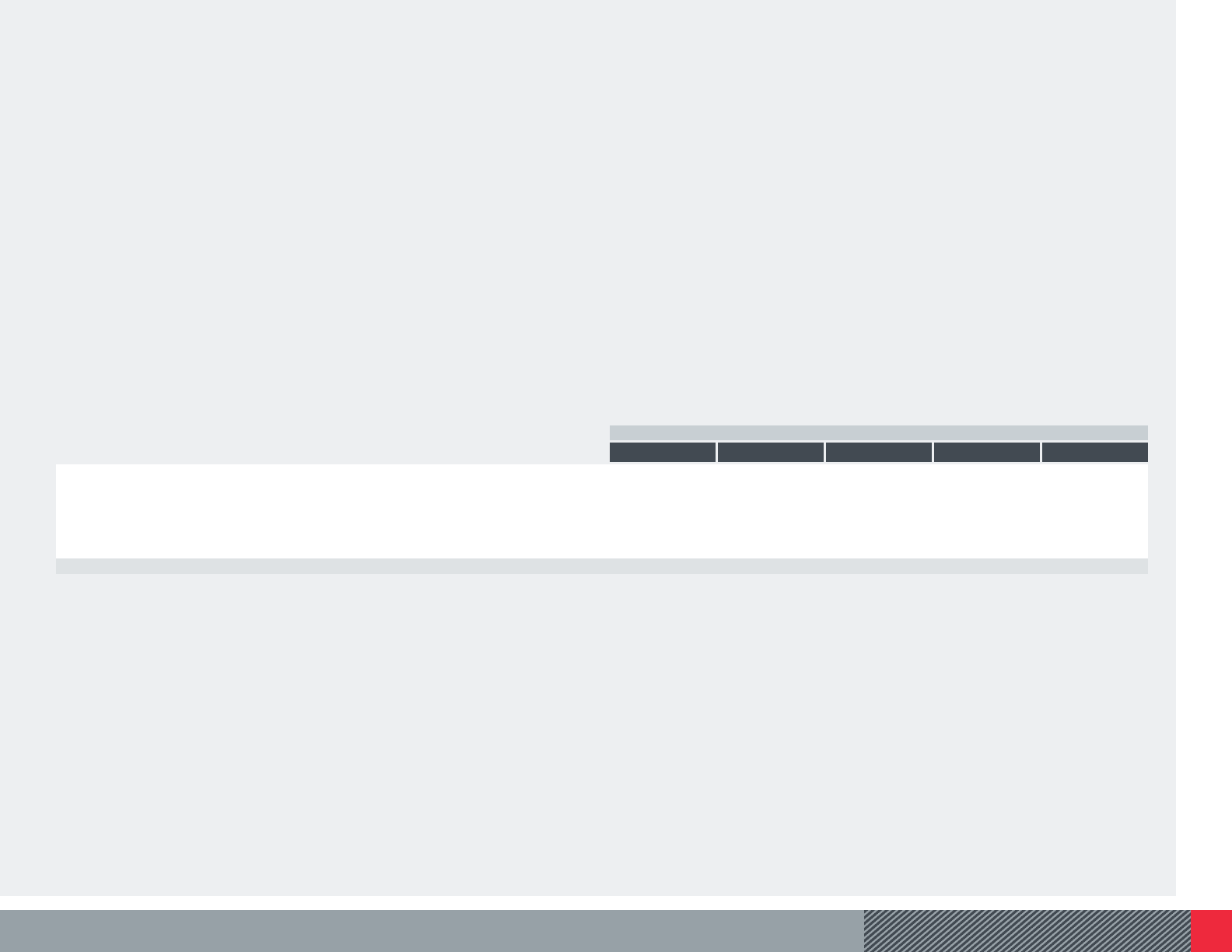

Following is a summary of our significant contractual obligations as of December 31, 2005:

PAYMENTS DUE BY PERIOD

In millions Total Within 1 Year 1-3 Years 3-5 Years After 5 Years

Operating leases $16,327.7 $1,233.0 $2,306.1 $2,295.8 $10,492.8

Long-term debt 1,935.0 341.4 387.3 652.4 553.9

Purchase obligations 70.5 24.5 46.0 — —

Other long-term liabilities reflected in our consolidated balance sheet 284.5 61.6 170.6 40.9 11.4

Capital lease obligations 0.7 0.2 0.2 0.3 —

$18,618.4 $1,660.7 $2,910.2 $2,989.4 $11,058.1