CVS 2002 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2002 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

|

|

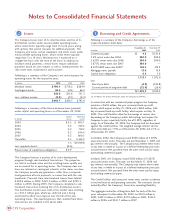

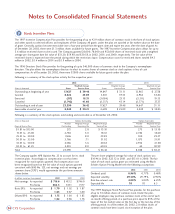

Advertising costs ~Advertising costs are expensed when the

related advertising takes place. Net advertising expense, which

is included in selling, general and administrative expenses was

$152.2 million in 2002, $126.9 million in 2001 and $90.5

million in 2000.

Interest expense, net ~Interest expense was $54.5 million,

$65.2 million and $84.1 million and interest income was $4.1

million, $4.2 million and $4.8 million in 2002, 2001 and

2000, respectively. Capitalized interest totaled $6.1 million in

2002, $10.1 million in 2001 and $14.1 million in 2000.

Interest paid, net of capitalized interest, totaled $60.7 million

in 2002, $75.2 million in 2001, and $98.3 million in 2000.

Nonrecurring items ~During 2001, the Company received

$50.3 million of settlement proceeds from various lawsuits

against certain manufacturers of brand name prescription drugs.

The Company elected to contribute $46.8 million of the

settlement proceeds to the CVS Charitable Trust, Inc. The net

effect of the two nonrecurring items was a $3.5 million pre-tax

($2.1 million after-tax) increase in net earnings (the “Net

Litigation Gain”). The Company also recorded a $352.5 million

pre-tax ($230.5 million after-tax) restructuring and asset

impairment charge in connection with the 2001 strategic

restructuring, which resulted from a comprehensive business

review designed to streamline operations and enhance operating

efficiencies. See Note 11 for further information on the 2001

strategic restructuring and resulting charge.

During 2000, the Company recorded a $19.2 million pre-tax

($11.5 million after-tax) nonrecurring gain in total operating

expenses, which represented a partial payment of the

Company’s share of the settlement proceeds received from a

class action lawsuit against certain manufacturers of brand name

prescription drugs.

Income taxes ~The Company provides for federal and state

income taxes currently payable, as well as for those deferred

because of timing differences between reporting income and

expenses for financial statement purposes versus tax purposes.

Federal and state incentive tax credits are recorded as a

reduction of income taxes. Deferred tax assets and liabilities are

recognized for the future tax consequences attributable to

differences between the carrying amount of assets and liabilities

for financial reporting purposes and the amounts used for

income tax purposes. Deferred tax assets and liabilities are

measured using the enacted tax rates expected to apply to

taxable income in the years in which those temporary

differences are expected to be recoverable or settled. The effect

of a change in tax rates is recognized as income or expense in

the period of the change.

Accumulated other comprehensive loss ~Accumulated other

comprehensive loss consists of a $44.6 million minimum

pension liability, net of a $27.3 million income tax benefit, as of

December 28, 2002. There was no accumulated other

comprehensive income or loss as of December 29, 2001.

Earnings per common share ~Basic earnings per common

share is computed by dividing: (i) net earnings, after deducting

the after-tax ESOP preference dividends, by (ii) the weighted

average number of common shares outstanding during the year

(the “Basic Shares”).

When computing diluted earnings per common share, the

Company assumes that the ESOP preference stock is converted

into common stock and all dilutive stock options are exercised.

After the assumed ESOP preference stock conversion, the ESOP

trust would hold common stock rather than ESOP preference

stock and would receive common stock dividends (currently

$0.23 per share) rather than ESOP preference stock dividends

(currently $3.90 per share). Since the ESOP Trust uses the

dividends it receives to service its debt, the Company would

have to increase its contribution to the ESOP trust to

compensate it for the lower dividends. This additional

contribution would reduce the Company’s net earnings, which in

turn, would reduce the amounts that would be accrued under

the Company’s incentive compensation plans.

Diluted earnings per common share is computed by dividing: (i)

net earnings, after accounting for the difference between the

dividends on the ESOP preference stock and common stock and

after making adjustments for the incentive compensation plans

by (ii) Basic Shares plus the additional shares that would be

issued assuming that all dilutive stock options are exercised and

the ESOP preference stock is converted into common stock.

Options to purchase 20.0 million and 5.2 million shares of

common stock were outstanding as of December 28, 2002 and

December 29, 2001, respectively, but were not included in the

calculation of diluted earnings per share because the options’

exercise prices were greater than the average market price of

the common shares and, therefore, the effect would be

antidilutive.

New Accounting Pronouncements ~The Company adopted,

SFAS No. 142, "Goodwill and Other Intangible Assets" effective

December 30, 2001. Among other things, this statement

requires that goodwill no longer be amortized, but rather tested

annually for impairment. Amortization expense related to

goodwill was $31.4 million pre-tax ($28.2 million after tax, or

$0.07 per diluted share) in 2001 and $33.7 million pre-tax

($31.9 million after-tax, or $0.08 per diluted share) in 2000.

See Note 4, for further information on the impact of adopting

SFAS No. 142.

Notes to Consolidated Financial Statements

28 CVS Corporation