CVS 2002 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2002 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

14

Introduction

For an understanding of the significant factors that influenced our

performance during the past three fiscal years, the following

discussion should be read in conjunction with the audited

consolidated financial statements and the notes thereto and the

Cautionary Statement Concerning Forward-Looking Statements

presented in this Annual Report.

Our Business

CVS Corporation (the “Company”) is a leader in the retail

drugstore industry in the United States. The Company sells

prescription drugs and a wide assortment of general merchandise,

including over-the-counter drugs, greeting cards, film and

photofinishing services, beauty products and cosmetics, seasonal

merchandise and convenience foods, through its CVS/pharmacy®

stores and online through CVS.com®. The Company also provides

Pharmacy Benefit Management and Specialty Pharmacy services

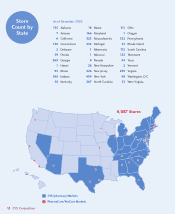

through PharmaCare Management Services. As of December 28,

2002, we operated 4,087 retail and specialty pharmacy stores in

32 states and the District of Columbia. For further information on

our business segments, see Note 10 to the consolidated financial

statements.

Results of Operations

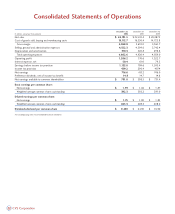

Net sales ~The following table summarizes our sales performance

for the respective years:

As you review our sales performance, we believe you should

consider the following important information:

•Our pharmacy sales growth continues to benefit from our

ability to attract and retain managed care customers and

favorable industry trends. These trends include an aging

American population that is consuming a greater number of

prescription drugs, the increased use of pharmaceuticals as

the first line of defense for healthcare and the introduction of

a number of successful new prescription drugs. However, the

introduction of new prescription drugs had less of an impact

on sales in 2001 and 2002, compared to previous years, due

to the lack of significant new drug introductions since 2001.

It is possible that this trend may continue in 2003 as there is

no way to predict with certainty the timing of new drug

introductions.

•Pharmacy sales dollars were negatively impacted during 2002

by increased introductions of lower priced generic drugs,

which are being substituted for higher priced brand name

drugs. Excluding the generic drug introductions, we estimate

that total same store sales growth for the fiscal year of 2002

would have been approximately 130 basis points higher, while

pharmacy same store sales growth would have been

approximately 180 basis points higher. However, gross margins

on generic drug sales are generally higher than on sales of

equivalent higher priced brand-name drugs.

•Front store sales benefited during 2002 from an increase in

promotional programs that were designed to respond to

competitive and economic conditions, and from the

implementation of our Assisted Inventory Management

system, which increased our in-stock positions. We will

continue to monitor the competitive and economic

environment and we will modify our future promotional

programs, if necessary. We cannot, however, guarantee that

our current and/or future promotional programs will produce

the desired lift in front store sales due to a number of

uncertainties that include, but are not limited to, the general

economic environment and consumer confidence.

•Total sales were negatively impacted during 2002 by the 229

stores that were closed as part of our 2001 strategic

restructuring. We estimate that the impact of the 229 store

closings, net of the sales which we believe transferred to our

remaining stores, lowered sales by approximately $257

million, (a reduction of approximately 120 basis points on

total sales growth) in 2002. However, we believe the sales

that transferred to our remaining stores benefited total same

store sales growth by approximately 60 basis points in 2002.

•Sales were negatively impacted during 2001 by a pharmacist

shortage in certain markets combined with the weakening

economy and an increasingly competitive environment that

ultimately resulted in lower customer counts and lost sales

during 2001. As of the end of 2001, we had returned to full

pharmacist staffing levels.

•Total sales also continued to benefit from our relocation

program, which seeks to move our existing shopping center

stores to larger, more convenient, freestanding locations.

Historically, we have achieved significant improvements in

customer count and net sales when we do this. Although the

number of annual relocations has decreased, our relocation

strategy remains an important component of our overall

growth strategy, as 47% of our existing stores were

freestanding as of December 28, 2002.

Management’s Discussion and Analysis of

2002 2001 2000

Net sales (in billions) $24.2 $22.2 $20.1

Net sales increase:

Total 8.7% 10.7% 11.0%

Pharmacy 11 . 2 % 14 . 5 % 17. 1 %

Front store 3.8% 3.9% 1.5%

Same store sales increase:

Total 8.4% 8.6% 10.9%

Pharmacy 11 . 7 % 13 . 0 % 17. 7 %

Front store 2.3% 1.2% 1.1%

Pharmacy % of total sales 67.6% 66.1% 62.7%

Third party % of pharmacy sales 92.3% 90.9% 89.2%

Prescriptions filled (in millions) 316 309 297

CVS Corporation