CVS 2002 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2002 CVS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

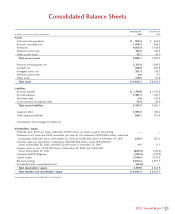

Gross margin, which includes net sales less the cost of

merchandise sold during the reporting period and the related

purchasing costs, warehousing costs, delivery costs and actual and

estimated inventory losses, as a percentage of net sales was 25.1%

in 2002. This compares to 25.6% in 2001 and 26.7% in 2000.

Why has our gross margin rate been declining?

•Pharmacy sales continued to grow at a faster pace than front

store sales. On average, our gross margin on pharmacy sales

is lower than our gross margin on front store sales. Pharmacy

sales as a percentage of total sales for 2002 were 67.6%,

compared to 66.1% in 2001 and 62.7% in 2000.

•Sales to customers covered by third party insurance programs

have continued to increase and, thus, have become a larger

part of our total pharmacy business. On average, our gross

margin on third party pharmacy sales is lower than our gross

margin on cash pharmacy sales. Third party prescription sales

for 2002 were 92.3% of pharmacy sales, compared to

90.9% in 2001 and 89.2% in 2000.

•In recent years, our third party gross margin rates have been

adversely affected by the efforts of managed care

organizations, pharmacy benefit managers, governmental and

other third party payors to reduce prescription drug costs. To

address this trend, we have dropped and/or renegotiated a

number of third party programs that fell below our minimum

profitability standards. These efforts have helped to stabilize

third party reimbursement rates. However, during the latter

part of 2002, as a result of increasing budget shortfalls,

numerous state legislatures proposed or were reported to be

considering reductions in pharmacy reimbursement rates for

Medicaid and other governmental programs as well as other

measures designed to reduce prescription drug costs. In the

event this trend continues and we elect to withdraw from

third party programs and/or decide not to participate in

future programs that fall below our minimum profitability

standards, we may not be able to sustain our current rate of

sales growth and gross margin dollars could be adversely

impacted.

•Also contributing to the gross margin rate decline during

2001 and 2002 were higher markdowns associated with the

increased promotional activity (discussed above) and elevated

physical inventory losses, offset, in part, by the increase in

generic drug sales (also discussed above), which normally

yield a higher gross margin rate than brand name drug sales.

Inventory losses for 2002 were 1.19% of net sales, compared

to 1.52% of net sales in 2001 and 0.60% of net sales in

2000. During 2001, we initiated a number of programs to

address the physical inventory loss trend. These programs

began to reduce inventory losses during the second half of

2002 and we believe they will continue to do so during

2003. However, we cannot guarantee that these programs will

continue to produce the desired results.

Total operating expenses, which include store and administrative

payroll, employee benefits, store and administrative occupancy

costs, selling expenses, advertising expenses, administrative

expenses and depreciation and amortization expense, were 20.1%

of net sales in 2002. This compares to 22.1% of net sales in 2001

and 20.1% in 2000. As you review our performance in this area,

please remember to consider the impact of the following items:

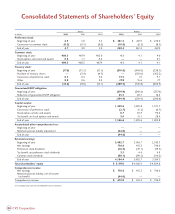

•During 2001, we recorded a $346.8 million pre-tax ($226.9

million after-tax) restructuring and asset impairment charge to

total operating expenses in connection with our 2001

strategic restructuring. We also recorded a $5.7 million pre-

tax ($3.6 million after-tax) charge to cost of goods sold to

reflect the markdown of certain inventory contained in the

closing stores to its net realizable value. In total, the

restructuring and asset impairment charge was $352.5 million

pre-tax ($230.5 million after-tax), the (“Restructuring

Charge”). For further information on the strategic

restructuring and resulting charge, see Note 11 to the

consolidated financial statements.

•During 2001, we received $50.3 million of settlement

proceeds from various lawsuits against certain manufactures

of brand name prescription drugs. We elected to contribute

$46.8 million of the settlement proceeds to the CVS

Charitable Trust, Inc. to fund future charitable giving. The net

effect of these nonrecurring items was a $3.5 million pre-tax

($2.1 million after-tax) increase in net earnings.

•

During 2000, we recorded a $19.2 million pre-tax ($11.5

million after-tax) nonrecurring gain in total operating expenses,

which represented a partial payment from a class action lawsuit

against certain manufacturers of brand name prescription

drugs.

If you exclude the impact of the items discussed above, total

operating expenses as a percentage of net sales were 20.1% in

2002, 20.6% in 2001 and 20.2% in 2000. As you review our

comparable operating expenses, we believe you should consider

the following important information:

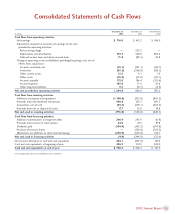

•As a result of adopting Statement of Financial Accounting

Standards ("SFAS") No. 142 at the beginning of 2002, we no

longer amortize goodwill. Goodwill amortization totaled

$31.4 million in 2001 and $33.7 million in 2000. For further

information on the impact of adopting SFAS No. 142, see

Note 4 to the consolidated financial statements.

•

Our strong sales performance has consistently allowed net sales

to grow at a faster pace than total operating expenses.

•

Total operating expenses as a percentage of net sales decreased

during 2002 primarily due to the operational initiatives

completed as part of the strategic restructuring and other

technology enhancements (such as the Excellence in Pharmacy

Innovation and Care system), which have lowered operating

costs, particularly at the store level, due to the increased

efficiencies resulting from our more streamlined operating

structure.

Financial Condition and Results of Operation

15

2002 Annual Report