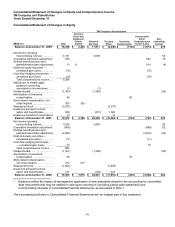

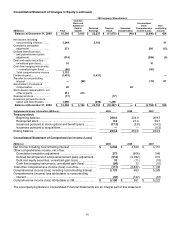

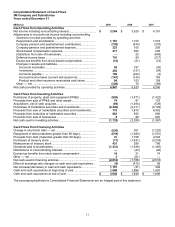

3M 2009 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2009 3M annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

56

New Accounting Pronouncements

In June 2009, the Financial Accounting Standards Board (FASB) issued a standard that established the FASB

Accounting Standards Codification™ (ASC) and amended the hierarchy of generally accepted accounting principles

(GAAP) such that the ASC became the single source of authoritative nongovernmental U.S. GAAP. The ASC did not

change current U.S. GAAP, but was intended to simplify user access to all authoritative U.S. GAAP by providing all

the authoritative literature related to a particular topic in one place. All previously existing accounting standard

documents were superseded and all other accounting literature not included in the ASC is considered non-

authoritative. New accounting standards issued subsequent to June 30, 2009 are communicated by the FASB

through Accounting Standards Updates (ASUs). For 3M, the ASC was effective July 1, 2009. This standard did not

have an impact on 3M’s consolidated results of operations or financial condition. However, throughout the notes to

the consolidated financial statements references that were previously made to various former authoritative U.S.

GAAP pronouncements have been changed to coincide with the appropriate section of the ASC.

In June 2006, the FASB issued an accounting standard codified in ASC 740, Income Taxes, related to accounting for

uncertainty in income taxes. This standard was adopted by 3M effective January 1, 2007. Refer to Note 8 for

additional information concerning this standard.

In September 2006, the FASB issued an accounting standard codified in ASC 820, Fair Value Measurements and

Disclosures. This standard established a single definition of fair value and a framework for measuring fair value, set

out a fair value hierarchy to be used to classify the source of information used in fair value measurements, and

required disclosures of assets and liabilities measured at fair value based on their level in the hierarchy. This

standard applies under other accounting standards that require or permit fair value measurements. 3M adopted the

standard as amended by subsequent FASB standards beginning January 1, 2008 on a prospective basis. One of the

amendments deferred the effective date for one year relative to nonfinancial assets and liabilities that are measured

at fair value, but are recognized or disclosed at fair value on a nonrecurring basis. This deferral applied to such items

as nonfinancial assets and liabilities initially measured at fair value in a business combination (but not measured at

fair value in subsequent periods) or nonfinancial long-lived asset groups measured at fair value for an impairment

assessment. These remaining aspects of the fair value measurement standard were adopted by the Company

prospectively beginning January 1, 2009 and did not have a material impact on 3M’s consolidated results of

operations or financial condition. Refer to Note 13 for additional disclosures of assets and liabilities that are

measured at fair value on a nonrecurring basis as a result of this adoption.

In February 2007, the FASB issued an accounting standard codified in ASC 825, Financial Instruments, that permits

an entity to choose, at specified election dates, to measure eligible financial instruments and certain other items at

fair value that were not currently required to be measured at fair value. An entity reports unrealized gains and losses

on items for which the fair value option has been elected in earnings at each subsequent reporting date. Upfront

costs and fees related to items for which the fair value option is elected are recognized in earnings as incurred and

not deferred. This standard also established presentation and disclosure requirements designed to facilitate

comparisons between entities that choose different measurement attributes for similar types of assets and liabilities.

This standard was effective for financial statements issued for fiscal years beginning after November 15, 2007

(January 1, 2008 for 3M) and interim periods within those fiscal years. At the effective date, an entity could elect the

fair value option for eligible items that existed at that date. The entity was required to report the effect of the first

remeasurement to fair value as a cumulative-effect adjustment to the opening balance of retained earnings. The

Company did not elect the fair value option for eligible items that existed as of January 1, 2008.

In June 2007, the FASB ratified a standard regarding the accounting for nonrefundable advance payments for goods

or services to be used in future research and development activities that requires nonrefundable advance payments

made by the Company for future R&D activities to be capitalized and recognized as an expense as the goods or

services are received by the Company. This standard was effective for 3M with respect to new arrangements entered

into beginning January 1, 2008 and did not have a material impact on 3M’s consolidated results of operations or

financial condition.

In December 2007, the FASB issued and, in April 2009, amended a new business combinations standard codified

within ASC 805, which changed the accounting for business acquisitions. Accounting for business combinations

under this standard requires the acquiring entity in a business combination to recognize all (and only) the assets

acquired and liabilities assumed in the transaction and establishes the acquisition-date fair value as the

measurement objective for all assets acquired and liabilities assumed in a business combination. Certain provisions

of this standard impact the determination of acquisition-date fair value of consideration paid in a business

combination (including contingent consideration); exclude transaction costs from acquisition accounting; and change

accounting practices for acquisition-related restructuring costs, in-process research and development,