3M 2009 Annual Report Download - page 3

Download and view the complete annual report

Please find page 3 of the 2009 3M annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

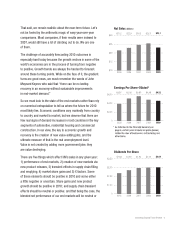

Innovating Toward Faster Growth 1

That said, we remain realistic about the near-term future. Let’s

not be fooled by the arithmetic magic of easy year-over-year

comparisons. Most companies, if their results were indexed to

2007, would still have a lot of climbing out to do. We are one

of them.

The challenge of accurately forecasting 2010 outcomes is

especially hard today because the growth vectors in some of the

world’s economies are in the process of turning from negative

to positive. Growth trends are always the hardest to forecast

around these turning points. While on the face of it, the gradient

turns are good news, we must remember the words of John

Maynard Keynes who said that “there can be no lasting

recovery in an economy without sustainable improvements

in end-market demand.”

So we must look to the state of the end markets rather than rely

on numerical extrapolation to tell us where the future for 2010

most likely lies. Economic conditions vary markedly from country

to country and market to market, but we observe that there are

few real signs of demand increases in most countries in the key

segments of automotive, residential housing and commercial

construction. In our view, the key to economic growth and

recovery is the creation of new value-adding jobs, and the

ultimate measure of that is the real unemployment level.

Value is not created by adding more government jobs: they

are value destroying.

There are five things which affect 3M’s sales in any given year:

1) performance of end markets, 2) creation of new markets via

new product releases, 3) transient effects in supply chain filling

and emptying, 4) market share gains and 5) X factors. Some

of these elements should be positive in 2010 and some either

a little negative or uncertain. Share gains and new product

growth should be positive in 2010; and supply chain transient

effects should be neutral or positive: and that being the case, the

blended net performance of our end markets will be neutral or