TomTom 2009 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2009 TomTom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

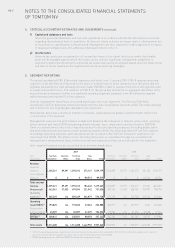

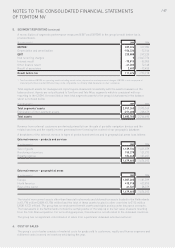

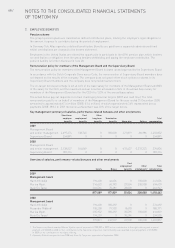

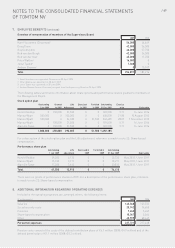

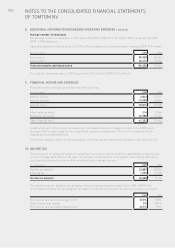

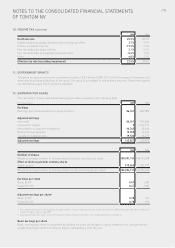

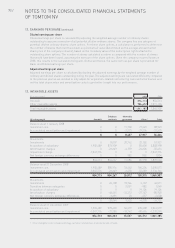

62 / NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

OF TOMTOM NV

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Goodwill

Goodwill represents the excess of the cost of an acquisition over the fair value of the group’s share of the net

identifiable assets of the acquired subsidiary/associate at the date of acquisition.

Goodwill on acquisitions is tested at least annually for impairment and carried at cost less accumulated

impairment losses. Goodwill is allocated to cash-generating units for the purpose of impairment testing. The

allocation is made to those cash-generating units or groups of cash-generating units that are expected to benefit

from the business combination in which the goodwill arose.

Intangible assets other than goodwill

Internally generated intangible assets

Internal software development costs relating to core technology are recognised as an intangible asset if, and only

if, all of the following have been demonstrated:

• the technical feasibility to complete the project

• the intention to complete the intangible asset, and use or sell it

• the ability to use or sell the intangible asset

• how the intangible asset will generate probable future economic benefits

• the availability of adequate resources to complete the project and,

• the cost of developing the asset can be measured reliably.

Internally generated databases are capitalised until a level of completion is reached and activities focus on

maintenance, at this point capitalisation is discontinued.

The amount initially recognised for internally-generated intangible assets is the sum of the expenditure incurred

from the date when the intangible asset first meets the recognition criteria listed above. Subsequent to initial

recognition, internal software development costs are carried at cost less accumulated amortisation and

accumulated impairment losses. The useful life of the group’s core software is estimated at four years.

The group is required to use estimates, assumptions and judgements to determine the expected useful lives and

future economic benefits of these costs. Such estimates are made on a regular basis, or as appropriate

throughout the year, as they can be significantly affected by changes in technology and other factors.

All expenditures on research activities are expensed in the income statement as incurred. Internal software costs

relating to development of non core software with estimated average useful life of less than one year and

engineering cost relating to the detailed manufacturing design of new products are expensed in the period in

which they are incurred.

Acquired intangible assets

Definite-lived intangible assets acquired separately or through a business combination are initially recognised at

cost. The cost of assets acquired separately includes the purchase price and directly attributable costs to bring

the asset to its intended use. Intangible assets acquired in a business combination are identified and recognised

separately from goodwill where they satisfy the definition of an intangible asset and their fair values can be

measured reliably. The cost of such intangible assets is their fair value at the acquisition date.

Subsequent to initial recognition, these intangible assets are carried at cost less accumulated amortisation and

accumulated impairment losses.

The estimated useful life of the intangible assets are as follows:

Databases and tools 10-20 years

Brand name 20 years

Customer relationships 20-27 years

Computer software 2-5 years

Acquired technology 4-5 years

Customer relationships include customers for Tele Atlas maps, there is a high cost to change map providers and

historically there is high customer retention.