TomTom 2009 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2009 TomTom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

/ 59

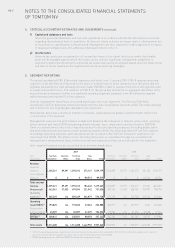

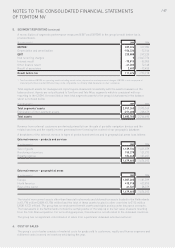

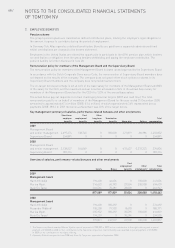

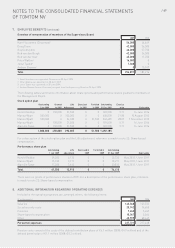

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

OF TOMTOM NV

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Business combinations (continued)

The provision for earn-outs relates to acquisitions where part of the purchase consideration is a future earn out

for the former shareholders of acquired companies. The group provides for future costs related to these earn-outs

based on (or related to) estimates of future results that determine the future cash outflows. The earn-out

provision represents the best estimate of payments which will be made under the earn-out arrangements, taking

into account the provisions of the related contract and the performance criteria included.

Goodwill arising on acquisition is recognised as an asset and initially measured at cost, being the excess of the

cost of the business combination over the group’s interest in the net fair value of the identifiable assets, liabilities

and contingent liabilities recognised. If, after reassessment, the group’s interest in the net fair value of the

acquiree’s identifiable assets, liabilities and contingent liabilities exceeds the cost of the business combination,

the excess is recognised immediately in the profit and loss account.

Associates

Associates are all entities over which the group has significant influence but not control, generally accompanying

a shareholding of between 20% and 50% of the voting rights, or other evidence of significant influence.

Investments in associates are accounted for using the equity method of accounting, and are initially recognised at

cost. The group’s investment in associates includes goodwill identified on acquisition, net of any accumulated

impairment loss.

The group’s share of its associates’ post-acquisition profits or losses is recognised in the income statement, and

its share of post-acquisition movements in reserves is recognised in reserves. The cumulative post-acquisition

movements are adjusted against the carrying amount of the investment. When the group’s share of losses in an

associate equals or exceeds its interest in the associate, including any other unsecured receivables, the group

does not recognise further losses, unless it has incurred obligations or made payments on behalf of the

associate. Unrealised gains on transactions between the group and its associates are eliminated to the extent of

the group’s interest in the associates. Unrealised losses are also eliminated, unless the transaction provides

evidence of an impairment of the asset transferred. Accounting policies of associates have been changed where

necessary to ensure consistency with the policies adopted by the group.

Revenue recognition

Revenue is measured as the fair value of the consideration received or receivable and represents amounts

receivable for goods and services provided in the normal course of business. Revenue is reduced for estimated

customer returns, rebates and other similar allowances.

Sale of goods

Revenue on the sale of goods is only recognised when the risks and rewards of ownership of goods are

transferred to the group’s customers (which include distributors, retailers, end-users and Original Equipment

Manufacturers (“OEMs”)). The risks and rewards of ownership are generally transferred at the time the product is

shipped and delivered to the customer and, depending on the delivery conditions, title and risk have passed to the

customer and acceptance of the product, when contractually required, has been obtained. In cases where

contractual acceptance is not required, revenue is recognised when management has established that all

aforementioned conditions for revenue recognition have been met.

Examples of the above-mentioned delivery conditions are ‘Free on Board point of delivery’ and ‘Costs, Insurance

Paid point of delivery’, where the point of delivery may be the shipping warehouse or any other point of destination

as agreed in the contract with the customer and where title and risk in the goods passes to the customer.

Estimates are made of the financial impact of returns, as well as sales incentives, based on historical data and

expectations of future sales. For further details, refer to note 4, Critical Accounting Estimates and Judgements.

Royalty revenue

Royalty revenue is generated by the licensing of geographic content of the Tele Atlas database to customers.

Licensing takes the form of selling products (CDs and DVDs) to end users for perpetual use or for a fixed period

of time. Revenue is recognised when the product is sold to the end-user. Where the data is licensed for a fixed

period of time, revenue recognition depends on the use of the data as reported by the customer or by the agent

when sold through an agent. Where royalty agreements contain minimum royalty amounts and arrangements for

upgrades, revenue is recognised when it is certain that the economic benefit will flow to the group. Depending on

the revenue characteristics of the related agreement, revenue on these royalty agreements is recognised upfront

or over the period of the agreement.

Sale of services

Services revenue is generated by map update services, content sales and connected navigation services for

commercial fleets. The revenue relating to the service element is recognised over the service period.