TomTom 2009 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2009 TomTom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

32 / BUSINESS RISKS (CONTINUED)

Loan covenants

We entered into a facility agreement in September

2007, under which we drew €1,585 million as a term

loan on 10 June 2008 to partially fund the acquisition

of Tele Atlas. The facility agreement includes a €174

million revolving credit facility which remained

entirely undrawn as of 31 December 2009.

The terms of the facility agreement were amended

in June 2009 and the net cash proceeds from a

rights issue in July 2009 were used to reduce our

level of indebtedness towards the banks by

approximately €400 million.

The amended financial covenants require us to

meet certain performance indicators relating to

interest cover and leverage. In case of breach of

our loan covenants, the banks are contractually

entitled to request early repayment of the

outstanding amount.

We closely monitor the contractual performance

indicators and based on the group’s plan for 2010,

management expects to be able to comply with the

loan covenants.

Foreign currencies

We operate internationally and conduct our business

in multiple currencies. Revenues are earned in

euro, pound sterling, the US dollar and other

currencies, while our cost of sales and other costs

are in euro, the US dollar and other currencies.

Foreign currency exposures on our commercial

transactions relate mainly to our estimated

purchases and sales transactions that are

denominated in a currency other than our

reporting currency – the euro (€).

We manage our foreign currency transaction

risk through the buying and selling of options

for forecasted exposures and by entering into

forward contracts for actual commitments. We

aim to cover our exposure for both purchases and

sales for the relevant term based on our business

characteristics. All such transactions are carried

out within the guidelines set by the Treasury

Risk Policy (section 5, Foreign Exchange Risk

Management), which has been approved by the

Supervisory Board.

We do not make use of natural hedges for

anticipated exposures, as these can prove

ineffective in the event of sharp increases or

decreases in currency rates and are therefore not

considered optimal from a risk management point

of view. Foreign currency exposures are grouped

by currency to allow for more efficient hedging.

We hedge at least 80% of our anticipated and

committed foreign currency exposure, in respect

of forecast sales and purchases.

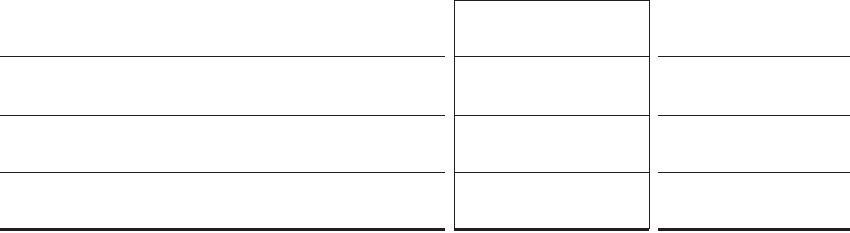

A 2.5% strengthening/weakening of the euro as

of 31 December against the currencies listed

below would have increased (decreased) profit

or loss by the amount shown below. This analysis

assumes that all other variables remain constant.

The analysis was performed on the same basis

for 2008.

2009 2008

(in €) strengthen weaken strengthen weaken

AUD

Net profit after taxation 178,260 -169,564 -254,611 242,190

GBP

Net profit after taxation 692,324 -658,559 -1,153,832 1,430,268

USD

Net profit after taxation 1,416,227 -1,349,176 1,728,546 -1,834,088

Interest rates

Our interest rate risk arises primarily from long term borrowings. These borrowings have a floating interest

coupon based on Euribor plus a spread which depends on leverage levels. The Euribor element of the

interest coupon is hedged with swap instruments.

Market-related interest income is received on the cash balances. It is our intention to earn a reasonable

interest income using vanilla investment instruments like bank deposits and money market fund

investments. All transactions are governed by the Treasury Risk Policy.