TomTom 2009 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2009 TomTom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

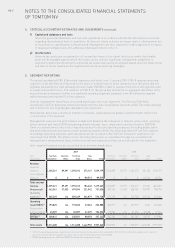

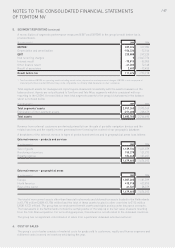

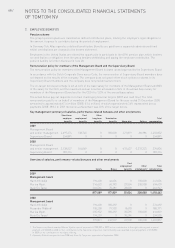

58 / NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

OF TOMTOM NV

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Foreign currencies

The group’s primary activities are denominated in euros. Accordingly, the euro is the company’s functional

currency, which is also the group’s presentation currency. Items included in the financial information of individual

entities in the group are measured using the individual entity’s functional currency, which is the currency of the

primary economic environment in which the entity operates.

Transactions and balances

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing on

the dates of the transactions. At each balance sheet date, monetary items denominated in foreign currencies are

retranslated at the rates prevailing at the balance sheet date. Non-monetary items carried at fair value that are

denominated in foreign currencies are retranslated at the rates prevailing at the date when the fair value was

determined. Non-monetary items that are measured in terms of historical cost in a foreign currency are not

retranslated. Foreign exchange gains and losses resulting from the settlement of such transactions and from the

translation at year-end exchange rates of monetary assets and liabilities denominated in foreign currencies are

recognised in the income statement, except when deferred in equity as qualifying cash flow hedges.

Foreign exchange gains and losses that relate to borrowings and cash and cash equivalents, and all other foreign

exchange gains and losses are presented in the income statement within the account “other financial result”.

Group companies

For consolidation purposes, the assets and liabilities of foreign entities that have a functional currency other than

the group’s presentation currency are translated at the year-end spot rate, whereas the income statement is

translated at the average monthly exchange rate. Translation differences arising thereon are taken to a separate

component of equity (cumulative translation adjustment).

Use of estimates

The preparation of these financial statements requires that the group makes assumptions, estimates and

judgements that affect the reported amounts of assets, liabilities and disclosure of contingent assets and

liabilities as of the date of the Consolidated Financial Statements and the reported amounts of revenues and

expenses during the reporting period. Actual results may differ from those estimates. Estimates are used when

accounting for items and matters such as revenue recognition, allowances for uncollectible accounts receivable,

inventory obsolescence, product warranty costs, depreciation and amortisation, asset valuations, impairment

assessments, taxes, earn-out provisions, other provisions, stock-based compensation and contingencies. The

estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are

recognised in the period in which the estimate is revised if the revision affects only that period, or in the period of

revision and the future periods if the revision affects both current and future periods. The principal accounting

policies adopted are set out below.

Cash flow statements

Cash flow statements are prepared using the indirect method. Cash flows from derivative instruments are

classified consistent with the nature of the instrument.

Basis of consolidation

The Consolidated Financial Statements incorporate the financial statements of the company and entities

controlled by the company (its subsidiaries). Control is achieved where the company has the power to govern the

financial and operating policies of an entity so as to obtain benefits from its activities.

Where necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting

policies in line with the group.

All inter-company transactions, balances, income and expenses are eliminated on consolidation.

Business combinations

The acquisition of subsidiaries is accounted for using the purchase method. The cost of the acquisition is

measured as the aggregate of the fair values at the date of exchange, of assets given, liabilities incurred or

assumed, and equity instruments issued by the group in exchange for control of the acquiree, plus any costs

directly attributable to the business combination. The acquiree’s identifiable assets, liabilities and contingent

liabilities that meet the conditions for recognition under IFRS 3 “Business Combinations” are recognised at their

fair values at the acquisition date.