TCF Bank 2009 Annual Report Download - page 3

Download and view the complete annual report

Please find page 3 of the 2009 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

2009 Annual Report : 1

offering, secured lending, prudent capital and liquidity

management, and well-managed expense control. We

continue to stand by our conservative philosophy of

banking which has proven to be far superior to the failed

models of our larger competitors. We have a business

model that works. With the commitment of our dedicated

employees, I expect to see continued growth and success.

A Look at 2009:

• TCF was the first bank out of the Top 50 Banks in the

country to repay the TARP preferred stock. In April, TCF

returned $361.2 million of TARP funds it had received

from the U.S. Treasury Department’s Capital Purchase

Program (CPP). TCF accepted the TARP funding in

order to avoid being labeled a weak bank but after the

government changed the rules of the program and public

perception soured, we felt it was no longer advantageous

or even necessary for TCF to continue its participation in

the program. A law change in February allowed for TARP

participants with strong capital levels to pay back TARP.

Unlike so many other TARP-exiting participants, TCF was

not required to raise additional capital to repay the TARP

funds. TCF paid a total of $8.9 million to the government

in TARP-related dividends and taxpayers benefited by an

additional $9.5 million from the auction of TCF warrants

the government received in connection with the program.

The result of TCF’s participation was an estimated 11

percent after-tax cost to TCF stockholders.

• TCF earned $87.1 million and diluted earnings per

common share was $.54. Although we were disap-

pointed in these results, TCF recently reported its

59th consecutive profitable quarter while many of our

competitors fell short during the economic crisis.

2009 was another very difficult year for the financial

services industry, yet TCF continued to be profitable and

reported its 59th consecutive quarter of profitability at

year-end — a record level of sustainability not seen by

many of our peers. In fact, the 2008 and 2009 recession

resulted in 140 failed banks, a national unemployment

rate exceeding 10 percent, and a large decline in housing

and other asset values which resulted in an unparalleled

expansion of government intervention into the financial

system to ward off a fiscal calamity.

TCF has remained profitable during this crisis because

we did not engage in the activities that created the

financial meltdown. TCF has not made subprime, teaser

rate, Option ARM, out of market, low documentation or

other risky mortgage loans. TCF has not participated in

junk bonds, collateralized debt obligations, asset-backed

commercial paper, structured investment vehicles, or other

off-balance-sheet programs. TCF has no auto or credit

card portfolios. TCF has never owned FANNIE MAE®

or

Freddie Mac®

preferred stock, trust preferred securities

or bank-owned life insurance. TCF did not originate, secu-

ritize and sell assets. We have no derivatives. While we

did not participate in these activities, we were not immune

to their effects. TCF’s earnings were down and the stock

price remained pressured throughout 2009, closing the

year at $13.62 per share, down 4 cents from 2008.

TCF management developed a conservative banking

philosophy in the late 1980’s and we have since strictly

adhered to this business model; as a result, TCF’s

fundamentals have remained strong. We have been

able to produce high performance results for many years

because we consistently value a large and growing

customer base through a convenient product and service

Dear Stockholders:

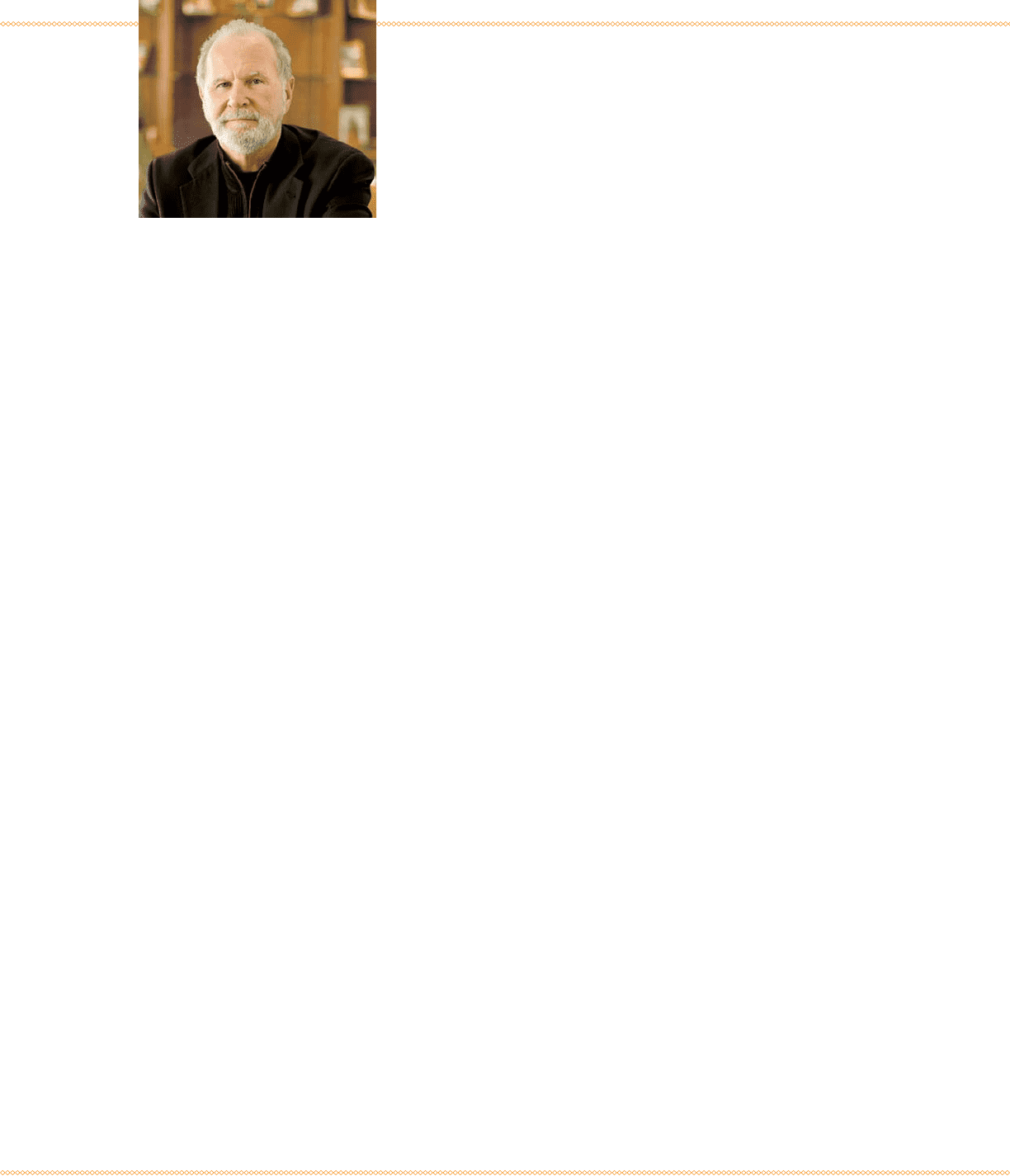

William A. Cooper, Chairman of the Board

and Chief Executive Officer