Safeway 2005 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2005 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

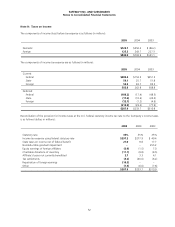

SAFEWAY INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

56

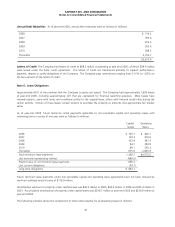

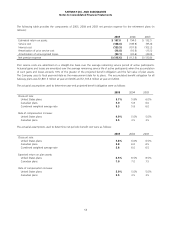

The Company has adopted and implemented an investment policy for the defined benefit pension plans that incorporates a

strategic long-term asset allocation mix designed to meet the Company’s long-term pension requirements. This asset

allocation policy is reviewed annually and, on a regular basis, actual allocations are rebalanced to the prevailing targets. The

following table summarizes actual allocations for Safeway’s plans at year-end 2005 and 2004:

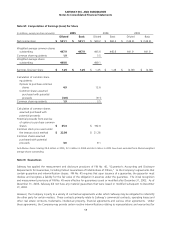

Plan assets

Asset category Target 2005 2004

Equity 65% 66.3% 67.4%

Fixed income 35 33.0 31.5

Cash and other −0.7 1.1

Total 100% 100.0% 100.0%

The investment policy also emphasizes the following key objectives: (1) maintain a diversified portfolio among asset classes

and investment styles; (2) maintain an acceptable level of risk in pursuit of long-term economic benefit; (3) maximize the

opportunity for value-added returns from active management; and (4) maintain adequate controls over administrative costs.

To meet these objectives, the Company’s investment policy reflects the following major themes: (1) diversify holdings to

achieve broad coverage of both stock and bond markets; and (2) use active investment managers with disciplined, clearly

defined strategies, while establishing investment guidelines and monitoring procedures for each investment manager to

ensure the characteristics of the portfolio are consistent with the original investment mandate.

Expected rates of return on plan assets were developed by determining projected stock and bond returns and then applying

these returns to the target asset allocations of the employee benefit trusts, resulting in a weighted average rate of return on

plan assets. Equity returns were based primarily on historical returns of the S&P 500 Index. Fixed-income projected returns

were based primarily on historical returns for the broad U.S. bond market.

Safeway expects to contribute approximately $27.0 million to its defined benefit pension plan trusts in 2006.

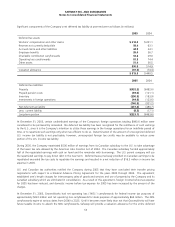

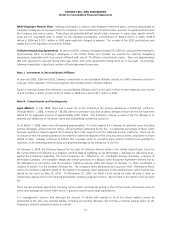

Retirement Restoration Plan The Retirement Restoration Plan provides death benefits and supplemental income payments

for senior executives after retirement. The Company recognized expense of $6.4 million in 2005, $7.1 million in 2004 and

$6.7 million in 2003. The aggregate projected benefit obligation of the Retirement Restoration Plan was approximately

$72.8 million at year-end 2005 and $74.4 million at year-end 2004.

Postretirement Benefits other than Pensions In addition to the Company’s retirement plans and the Retirement

Restoration Plan benefits, the Company sponsors plans that provide postretirement medical and life insurance benefits to

certain employees. Retirees share a portion of the cost of the postretirement medical plans. Safeway pays all the costs of

the life insurance plans. The plans are not funded.

The Company’s accrued postretirement benefit obligation (“APBO”) was $50.3 million at year-end 2005 and $77.8 million at

year-end 2004. The APBO represents the actuarial present value of the benefits expected to be paid after retirement.

Postretirement benefit expense was $4.2 million in 2005, $10.3 million in 2004 and $9.2 million in 2003.

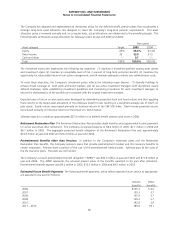

Estimated Future Benefit Payments The following benefit payments, which reflect expected future service as appropriate,

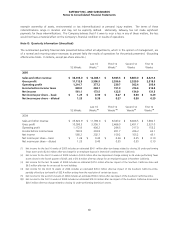

are expected to be paid (in millions):

Pension

benefits

Other

benefits

2006 $125.3 $ 4.5

2007 130.3 3.7

2008 135.4 3.7

2009 139.3 3.7

2010 142.8 3.8

2011 − 2015 780.4 19.1