Porsche 2005 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2005 Porsche annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

116

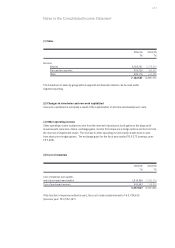

Self-constructed items of property, plant and equipment are recognized at cost of conversion.

In addition to directly allocable costs, they include a proportionate share of production-related overheads.

Financing costs are not included as a component of cost.

Leased assets

Leased assets result from leases where substantially all risks and opportunities incidental to ownership

remain with the Porsche Group as the lessor. These are vehicles from operating leases. They are measured

at cost less systematic straight-line depreciation over their expected useful life or the shorter contract

period taking account of estimated residual values.

Impairment test

An impairment test is performed at least once a year for goodwill, but for other intangible assets with finite

useful lives as well as property, plant and equipment, leased assets and financial assets only when there

is an indication that the asset may be impaired. An impairment loss is recognized if the recoverable

amount of the asset falls short of the carrying amount. If the recoverable amount of the asset falls short

of the carrying value, an impairment loss is recognized. The recoverable amount is generally determined

separately per individual asset. If this is not possible, it is determined on the basis of a group of assets or

the legal entity. The recoverable amount is the higher of an asset’s net selling price and its value in use.

The net selling price is the amount obtainable from the sale of an asset at customary market conditions

less the costs of disposal. Value in use is determined using the discounted cash flow method or capitalized

earnings method on the basis of the estimated future cash flows expected to arise from the continuing

use and its disposal. The cash flows are derived from the long-term business planning and current deve-

lopments are taken into account. They are discounted to the balance sheet date using market-oriented

discount rates for similar risks (before tax) of an average of 8.85 to 10 percent.

If the reason for impairment losses recorded in previous years ceases to exist, the impairment loss is

reversed to a maximum amount of amortized cost. This does not apply to goodwill.

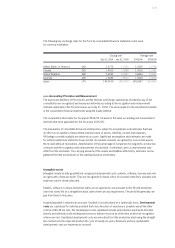

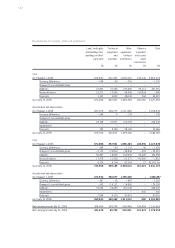

Years

Office and factory equipment 25 to 40

Technical equipment and machines 7 to 20

Other equipment, furniture and fixtures 3 to 13

Property, plant and equipment

Property, plant and equipment are measured at cost less systematic depreciation over their useful life as

well as impairment losses. Costs for repairs and maintenance are recognized as current expenses.

Systematic depreciation, mainly using the straight-line and unit of production methods of depreciation,

reflects the pattern in which the asset’s future economic benefits are expected to be consumed by the

entity. Special tools and equipment are depreciated according to units of production. For plants used in

shift operation depreciation is increased by additional payments for shifts.

Systematic depreciation is mostly based on the following useful lives: