Porsche 2005 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2005 Porsche annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

114

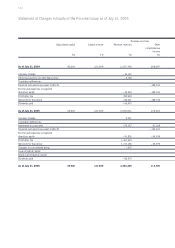

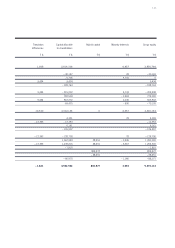

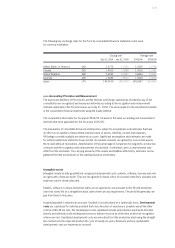

Consolidation Principles

Capital consolidation is performed in accordance with the purchase method pursuant to IFRS 3 (“Business

Combinations”). Purchased assets and liabilities are measured at their fair value on the date of acquisition.

The purchase costs of the shares acquired are then offset against pro rata revalued equity of the subsi-

diary. Any remaining positive difference from offsetting the purchase price against the identified assets

and liabilities is shown as goodwill. To the extent that the identified assets and liabilities exceed the pur-

chase price of the investment, it is recorded in the income statement immediately in the year of acquisition.

Expenses and income as well as receivables, liabilities and provisions between the consolidated entities

are offset. Intercompany profits from the disposal of assets within the Group which have not yet been

resold to third parties are eliminated. Deferred taxes are recognized for consolidations with effect on in-

come taxes. In addition, guarantees and warranties assumed by Porsche AG or one of its consolidated

subsidiaries in favor of other subsidiaries are eliminated.

Investments in associates included using the equity method are carried at cost at the time of first-time

inclusion. The rulings for full consolidation apply by analogy to the measurement using the equity method.

In subsequent periods, the carrying amount is rolled forward to reflect changes in equity of the associate

on the Porsche Group. An impairment test is carried out if there is any indication that that investment is

impaired.

Due to immateriality, the company elects not to eliminate intercompany profits from trade relations

with associates.

Currency Translation

The financial statements of consolidated subsidiaries prepared in foreign currency are translated to the

Euro in accordance with IAS 21. The functional currency is the local currency for all consolidated entities,

since these subsidiaries are independent operations from a financial, economic and organizational per-

spective. Assets, liabilities and contingent liabilities are translated at the mean rate as of the balance sheet

date, while equity is translated at historical rates with the exception of income and expenses recorded

directly in equity. The income statement is translated using average annual exchange rates. Exchange rate

differences resulting from the translation of financial statements are recognized as a separate item directly

under equity until the disposal of the subsidiary.

Foreign currency items in the financial statements of the entities included in consolidation are measured

at the historical rates. Exchange rate gains and losses as of the balance sheet date are recorded in the

income statement.