Logitech 2005 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2005 Logitech annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

|

|

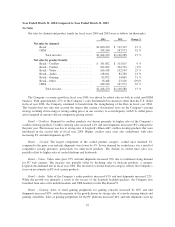

Further, the Company offers volume rebates to its distribution and retail customers and records reserves for

such rebates at the time of shipment. Estimates of required reserves are determined based on a consideration of

historical experience, anticipated volume of future purchases, and inventory levels in the channel. Changes in any

of these variables could impact the amount of the recorded reserves.

Also, the Company enters into cooperative marketing arrangements with most of its distribution and retail

customers allowing customers to receive a credit equal to a set percentage of their purchases of the Company’s

products for various marketing programs. The objective of these programs is to encourage advertising and

promotional events to increase sales of the Company’s products. Accruals for the estimated costs of these

marketing programs are recorded based on the contractual percentage of product purchased in the period the

Company recognizes revenue. The Company regularly evaluates the adequacy of these marketing program

accruals.

Future market conditions and product transitions may require the Company to take actions to increase

customer programs and incentive offerings that could result in incremental reductions to revenue or increased

operating expenses at the time the incentive is offered.

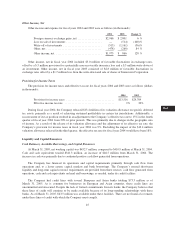

Allowance for Doubtful Accounts

The Company sells its products through a domestic and international network of distributors, retailers and

OEM customers. Logitech generally does not require any collateral from its customers. However, the Company

seeks to control its credit risk through ongoing credit evaluations of its customers’ financial condition and by

purchasing credit insurance on U.S. and European retail accounts receivable balances.

The Company regularly evaluates the collectibility of its accounts receivable and maintains allowances for

doubtful accounts. The allowances are based on management’s assessment of the collectibility of specific

customer accounts, including their credit worthiness and financial condition, as well as the Company’s historical

experience with bad debts, receivables aging, current economic trends and the financial condition of the

Company’s distribution channels.

As of March 31, 2005, three customers represented 14%, 12% and 11% of total accounts receivable. The

customers comprising the ten highest outstanding trade receivable balances accounted for approximately 56% of

total accounts receivables as of March 31, 2005. A deterioration of a significant customer’s financial condition

could cause actual write-offs to be materially different from the estimated allowance. If any of these customer’s

receivable balances should be deemed uncollectible, the Company would have to make adjustments to its

allowance for doubtful accounts, which could have an adverse affect on its financial condition and results of

operations in the period the adjustments are made.

Inventory Valuation

The Company must order components for its products and build inventory in advance of customer orders.

Further, the Company’s industry is characterized by rapid technological change, short-term customer

commitments and rapid changes in demand.

The Company records inventories at the lower of cost or market value and records write-downs of

inventories which are obsolete or in excess of anticipated demand or market value. A review of inventory is

performed each period that considers factors including the marketability and product lifecycle stage, product

development plans, component cost trends, demand forecasts and current sales levels. Inventory exposures are

identified by comparing inventory on hand and on order to forecasted sales over the next six, nine and twelve

month periods. Inventory on hand which is not expected to be sold or utilized based on review of forecasted sales

and utilization is considered excess, and the Company recognizes the write-off in cost of sales at the time of such

determination. If there were an abrupt and substantial decline in demand for Logitech’s products or an

35

CG

20-F

LISA