Food Lion 2006 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2006 Food Lion annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

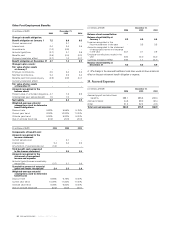

Interest Rate Swaps

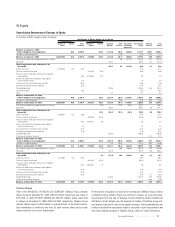

During 2003, a subsidiary of Delhaize Group entered into interest rate swap

agreements to exchange the fixed interest rate of its newly issued EUR 100

million bond for variable rates. The notional amount is EUR 100 million maturing

in 2008. The fixed rate is 8.00%. The variable rate is based on the three-month

Euribor and is reset on a quarterly basis.

During 2002 and 2001, Delhaize America entered into interest rate swap agree-

ments, effectively converting a portion of its debt from fixed to variable rates.

Maturity dates of interest rate swap arrangements match those of the underlying

debt. Variable rates for these agreements are based on six-month or three-

month US Libor and are reset on a semi-annual basis or a quarterly basis. In

December 2003, Delhaize America cancelled USD 100 million (EUR 75.9 million)

of the 2011 interest rate swap arrangement. The notional principal amount of

the interest rate swap arrangements at December 31, 2006 was USD 100 million

(EUR 75.9 million) maturing in 2011.

The interest rate swap agreements exchange fixed rate interest payments for

variable rate payments without the exchange of the underlying principal amounts.

The differential between fixed and variable rates to be paid or received is accrued

as interest rates change in accordance with the agreements and recognized over

the life of the agreements as an adjustment to interest expense. The fair value

of interest rate swaps at December 31, 2006, 2005 and 2004 was EUR -2.6 mil-

lion, EUR - 0.5 million and EUR 6.3 million, respectively. The interest rate swaps

are designated and are effective fair value hedges recorded at fair value on the

balance sheet with changes in fair value recorded in the income statement as

finance costs.

Derivative instruments are carried at fair value defined as the amount at which

these instruments could be settled based on estimates obtained from financial

institutions:

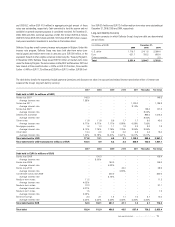

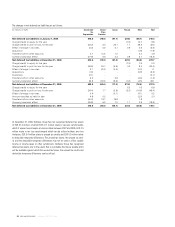

December 31,

(in millions of EUR) 2006 2005 2004

Assets Liabilities Assets Liabilities Assets Liabilities

Interest rate swaps - 2.6 0.9 1.4 6.3 -

Cross currency swaps 0.2 2.3 0.3 7.7 - 15.1

Foreign exchange

forward contracts 1.7 - - - - -

Total 1.9 4.9 1.2 9.1 6.3 15.1

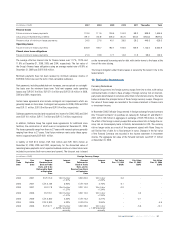

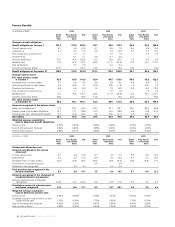

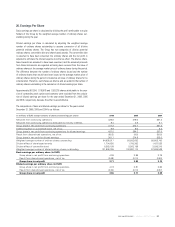

20. Provisions

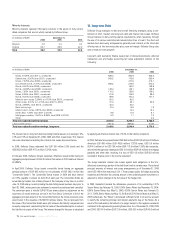

December 31,

(in millions of EUR) 2006 2005 2004

Closed store provision:

Non-current 73.6 101.4 96.7

Current 10.4 13.9 21.3

Self-insurance provision:

Non-current 116.1 125.6 105.1

Current 1.4 5.4 4.2

Pension benefit and other

post-employment benefit provision:

Non-current 80.8 102.0 75.3

Other provisions:

Non-current 19.8 21.7 11.3

Current 2.5 2.2 2.0

Total provisions

Non-current 290.3 350.7 288.4

Current 14.3 21.5 27.5

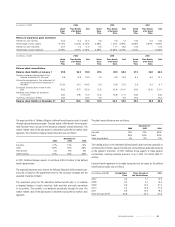

21. Closed Store Provision

Delhaize Group records closed store provisions for the present value of post-clos-

ing lease liabilities and other contractually obligated lease related costs such as

real estate taxes, common area maintenance and insurance cost, net of estimated

amounts to be recovered from subletting closed store space. Remaining lease

liabilities on closed stores generally range from one to 17 years. The average

remaining lease term for closed stores was 5.9 years at December 31, 2006.

The liability associated with each store is discounted using a pre-tax rate that

reflects the borrowing rate of debt with terms matching the terms of future rent

payments. The adequacy of the provision for closed stores is dependent on the

Group’s ability to sublet closed store property for the estimated recovery amount

which may be affected by changes in the economic conditions in the areas where

closed stores are located.

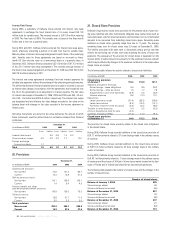

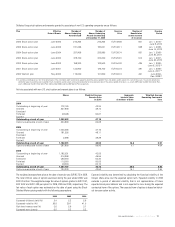

The following table reflects the activity related to closed store liabilities:

(in millions of EUR) 2006 2005 2004

Closed store provision

at January 1 115.3 118.0 121.7

Additions charged to earnings:

Store closings - lease obligations 5.5 8.5 38.3

Store closings - other exit costs 1.5 1.7 7.8

Adjustments to prior year estimates (2.8) 0.2 (2.9)

Interest expense 8.6 10.4 13.1

Reductions:

Lease payments made (21.4) (23.3) (28.9)

Lease terminations (8.2) (13.4) (12.1)

Payments made for other exit costs (3.6) (4.0) (9.6)

Transfer to other accounts 0.4 0.2 (0.3)

Amount classified as held for sale (0.3) - -

Currency translation effect (11.0) 17.0 (9.1)

Closed store provision

at December 31 84.0 115.3 118.0

The provision for closed stores primarily relates to the closed store obligations

in the United States.

During 2006, Delhaize Group recorded additions to the closed store provision of

EUR 7.1 million primarily related to 27 store closings made in the ordinary course

of business.

During 2005, Delhaize Group recorded additions to the closed store provision

of EUR 10.2 million primarily related to 32 store closings made in the ordinary

course of business.

During 2004, Delhaize Group recorded additions to the closed store provision of

EUR 46.1 million primarily related to 17 store closings made in the ordinary course

of business and the closure of 34 Kash n’ Karry stores mainly located on the East

coast of Florida and in Orlando and classified as discontinued operations.

The following table presents the number of closed stores and the changes in the

number of closed stores:

Number of closed stores

Balance at January 1, 2004 225

Store closings added 52

Stores sold/lease terminated (50)

Balance at December 31, 2004 227

Store closings added 32

Stores sold/lease terminated (52)

Balance at December 31, 2005 207

Store closings added 27

Stores sold/lease terminated (53)

Balance at December 31, 2006 181

/ ANNUAL REPORT 2006

82