Dollar Tree 2014 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2014 Dollar Tree annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

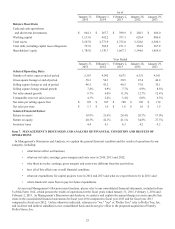

16

Lawsuits have been filed against Family Dollar, its directors, Dollar Tree, and one of Dollar Tree's subsidiaries challenging

the proposed merger, and an adverse ruling in such lawsuits may prevent the proposed merger from becoming effective or

from becoming effective within the expected timeframe.

Family Dollar, its directors, Dollar Tree, and one of Dollar Tree's subsidiaries are named as defendants in three putative

class action lawsuits, which have been consolidated under the caption In re Family Dollar Stores, Inc. Stockholder Litig.,

C.A. No. 9985 CB., brought by purported Family Dollar shareholders challenging the proposed merger, seeking, among other

things, to enjoin consummation of the proposed merger. The parties conducted certain document discovery and depositions

relating to the motion for a preliminary injunction and a hearing was held on December 5, 2014. On December 19, 2014, the

Court of Chancery issued an opinion and order denying plaintiffs’ preliminary injunction motion. The plaintiffs sought from

the Court of Chancery certification of an interlocutory appeal of that order to the Delaware Supreme Court, but on January 2,

2015, the Court of Chancery denied that request. No schedule has yet been set for the adjudication of the plaintiffs’ remaining

claims for relief. If the plaintiffs are successful in their remaining claims, there could be an adverse effect on our and Family

Dollar’s business, financial condition, results of operations and cash flows.

Our substantial indebtedness could adversely affect our financial condition and prevent us from fulfilling our

obligations under the notes.

Our consolidated indebtedness as of January 31, 2015 was $757 million. Following the proposed merger, we will have

substantially increased our indebtedness, which could adversely affect our ability to fulfill our obligations and have a negative

impact on our financing options and liquidity position. Upon completion of the proposed merger we expect to have

indebtedness of approximately $8,507 million and availability under our new revolving credit facility of approximately

$1,250 million, less amounts outstanding for letters of credit.

Our high level of debt could have significant consequences, including the following:

• limiting our ability to obtain additional financing in the future for working capital, capital expenditures,

acquisitions or other general corporate purposes;

• requiring a substantial portion of our cash flows to be dedicated to debt service payments, instead of other

purposes, thereby reducing the amount of cash flows available for working capital, capital expenditures,

acquisitions and other general corporate purposes;

• limiting our ability to refinance our indebtedness on terms acceptable to us or at all;

• imposing restrictive covenants on our operations;

• placing us at a competitive disadvantage to competitors carrying less debt; and

• making us more vulnerable to economic downturns and limiting our ability to withstand competitive

pressures.

In addition, our credit ratings impact the cost and availability of future borrowings and, accordingly, our cost of

capital. Our ratings reflect the opinions of the ratings agencies of our financial strength, operating performance and ability

to meet our debt obligations. There can be no assurance that we will achieve a particular rating or maintain a particular

rating in the future.

We may not be able to generate sufficient cash to service all of our indebtedness and may be forced to take other actions to

satisfy our obligations under our indebtedness, which may not be successful.

Our ability to make scheduled payments on or to refinance our debt obligations depends on our financial condition and

operating performance, which are subject to prevailing economic and competitive conditions and to certain financial,

business, legislative, regulatory and other factors beyond our control. We may be unable to maintain a level of cash flows

from operating activities sufficient to permit us to fund our day-to-day operations or to pay the principal, premium, if any, and

interest on our indebtedness.

If our cash flows and capital resources are insufficient to fund our debt service obligations and other cash requirements,

we could face substantial liquidity problems and could be forced to reduce or delay investments and capital expenditures or to

sell assets or operations, seek additional capital or restructure or refinance our indebtedness. We may not be able to effect any

such alternative measures, if necessary, on commercially reasonable terms or at all and, even if successful, such alternative

actions may not allow us to meet our scheduled debt service obligations. Upon consummation of the proposed merger, the

agreements that will govern the indebtedness to be incurred or assumed in connection with the proposed merger are expected

to restrict (a) our ability to dispose of assets and use the proceeds from any such dispositions and (b) our ability to raise debt