ComEd 2001 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2001 ComEd annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

|

|

61

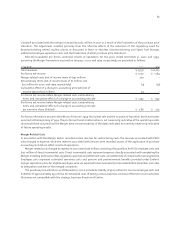

of these contracts are generally considered cash flow hedges under SFAS No. 133. To the extent that the hedges are effective,

changes in the fair value of these contracts are recorded in other comprehensive income, until earnings are affected by the

variability of cash flows being hedged.

Additionally, during 2001, as part of the creation of Exelon’s energy trading operation, Exelon began to enter into

contracts to buy and sell energy for trading purposes subject to limits. These contracts are recognized on the balance sheet

at fair value and changes in the fair value of these derivative financial instruments are recognized in earnings.

Prior to the adoption of SFAS No. 133, Exelon applied hedge accounting only if the derivative reduced the risk of the

underlying hedged item and was designated at the inception of the hedge, with respect to the hedged item. Exelon

recognized any gains or losses on these derivatives when the underlying physical transaction affected earnings.

Contracts entered into by Exelon to limit market risk associated with forward energy commodity contracts are reflected

in the financial statements at the lower or cost or market using the accrual method of accounting. Under these contracts

Exelon recognizes any gains or losses when the underlying physical transaction affects earnings. Revenues and expenses

associated with market price risk management contracts were amortized over the terms of such contracts.

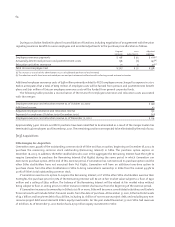

New Accounting Pronouncements

In 2001, the FASB issued SFAS No. 141, “Business Combinations” (SFAS No. 141), SFAS No. 142, and No. 143, “Asset Retirement

Obligations” (SFAS No. 143) and SFAS No. 144, “Accounting for the Impairment or Disposal of Long-Lived Assets (SFAS No. 144).

SFAS No. 141 requires that all business combinations be accounted for under the purchase method of accounting and

establishes criteria for the separate recognition of intangible assets acquired in business combinations. SFAS No. 141 is

effective for business combinations initiated after June 30, 2001.

SFAS No. 142 establishes new accounting and reporting standards for goodwill and intangible assets. Exelon adopted SFAS

No. 142 as of January 1, 2002. Under SFAS No. 142, effective January 1, 2002, goodwill recorded by Exelon is no longer subject to

amortization. After January 1, 2002, goodwill will be subject to an assessment for impairment using a two-step fair value

based test, the first step of which must be performed at least annually, or more frequently if events or circumstances indicate

that goodwill might be impaired. The first step compares the fair value of a reporting unit to its carrying amount, including

goodwill. If the carrying amount of the reporting unit exceeds its fair value, the second step is performed. The second step

compares the carrying amount of the goodwill to the fair value of the goodwill. If the fair value of goodwill is less than the

carrying amount,an impairment loss would be reported as a reduction to goodwill and a charge to operating expense,except

at the transition date, when the loss would be reflected as a cumulative effect of a change in accounting principle. As of

December 31, 2001, Exelon’s Consolidated Balance Sheets reflected approximately $5.3 billion in goodwill net of accumulated

amortization, including $4.9 billion of net goodwill related to the merger of Unicom and PECO recorded on ComEd’s

Consolidated Balance Sheets, with the remainder related to Enterprises. Annual amortization of goodwill related to the

Merger and to Enterprises of $126 million and $24 million, respectively, was discontinued upon adoption of SFAS No. 142.

Exelon has completed the first step of the transitional impairment analysis which indicated that the ComEd goodwill is not

impaired but that an impairment exists with respect to the Enterprises goodwill. The second step of the analysis, which will

compare the fair value of the Enterprises goodwill to the $433 million carrying value at December 31, 2001 has not yet been

completed. The second step analysis is expected to be completed, and the transitional impairment loss recognized, in the

first quarter of 2002 as a Cumulative Effect of a Change in Accounting Principle.

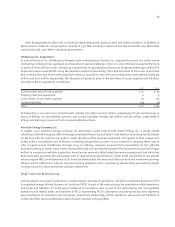

SFAS No. 143 provides accounting requirements for retirement obligations associated with tangible long-lived assets. Exelon

expects to adopt SFAS No. 143 on January 1, 2003. Retirement obligations associated with long-lived assets included within the

scope of SFAS No. 143 are those for which there is a legal obligation to settle under existing or enacted law, statute, written or

oral contract or by legal construction under the doctrine of promissory estoppel. Adoption of SFAS No. 143 will change the

accounting for the decommissioning of Exelon’s nuclear generating plants. Currently, Exelon records the obligation for

decommissioning ratably over the lives of the plants. The January 1, 2003 adoption of SFAS No. 143 will require a cumulative

effect adjustment effective the date of adoption to adjust plant assets and decommissioning liabilities to the values they

would have been had this standard been employed from the in-service dates of the plants.