Albertsons 2011 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2011 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

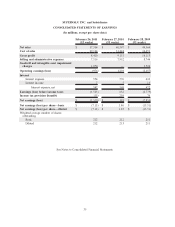

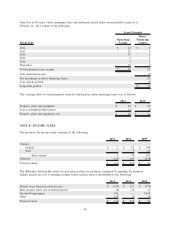

Retail food advertising expenses are a component of Cost of sales in the Consolidated Statements of Earnings

and are expensed as incurred. Retail food advertising expenses, net of cooperative advertising reimbursements,

were $120, $137 and $184 for fiscal 2011, 2010 and 2009, respectively.

The Company recognizes vendor funds for merchandising and buying activities as a reduction of Cost of sales

when the related products are sold. Vendor funds that have been earned as a result of completing the required

performance under the terms of the underlying agreements but for which the product has not yet been sold are

recognized as reductions of inventory. When payments or rebates can be reasonably estimated and it is

probable that the specified target will be met, the payment or rebate is accrued. However, when attaining the

milestone is not probable, the payment or rebate is recognized only when and if the milestone is achieved.

Any upfront payments received for multi-period contracts are generally deferred and amortized on a straight-

line basis over the life of the contracts.

Selling and Administrative Expenses

Selling and administrative expenses consist primarily of store and corporate employee-related costs, such as

salaries and wages, health and welfare, worker’s compensation and pension benefits, as well as rent, occupancy

and operating costs, depreciation and amortization and other administrative costs.

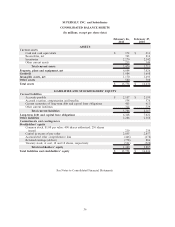

Cash and Cash Equivalents

The Company considers all highly liquid investments with a maturity of three months or less at the time of

purchase to be cash equivalents. The Company’s banking arrangements allow the Company to fund

outstanding checks when presented to the financial institution for payment, resulting in book overdrafts. Book

overdrafts are recorded in Accounts payable in the Consolidated Balance Sheets and are reflected as an

operating activity in the Consolidated Statements of Cash Flows. As of February 26, 2011 and February 27,

2010, the Company had net book overdrafts of $360 and $330, respectively.

Allowances for Losses on Receivables

Management makes estimates of the uncollectibility of its accounts and notes receivable portfolios. In

determining the adequacy of the allowances, management analyzes the value of the collateral, customer

financial statements, historical collection experience, aging of receivables and other economic and industry

factors. The allowance for losses on receivables was $8 and $12 in fiscal 2011 and 2010, respectively. Bad

debt expense was $12, $4 and $7 in fiscal 2011, 2010 and 2009, respectively.

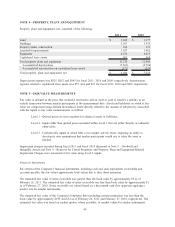

Inventories

Inventories are valued at the lower of cost or market. Substantially all of the Company’s inventory consists of

finished goods.

As of February 26, 2011 and February 27, 2010, approximately 79 percent of the Company’s inventories were

valued using the last-in, first-out (“LIFO”) method. The Company uses a combination of the replacement cost

method and the retail inventory method (“RIM”) to determine the current cost of its inventory before any

LIFO reserve is applied. Under the replacement cost method, the most current unit purchase cost is used to

calculate the current cost of inventories. Under RIM, the current cost of inventories and the gross margins are

calculated by applying a cost-to-retail ratio to the current retail value of inventories. The first-in, first-out

method (“FIFO”) is primarily used to determine cost for some of the remaining highly perishable inventories.

If the FIFO method had been used to determine cost of inventories for which the LIFO method is used, the

Company’s inventories would have been higher by approximately $282 and $264 as of February 26, 2011 and

February 27, 2010, respectively.

During fiscal 2011, 2010 and 2009, inventory quantities in certain LIFO layers were reduced. These reductions

resulted in a liquidation of LIFO inventory quantities carried at lower costs prevailing in prior years as

compared with the cost of fiscal 2011, 2010 and 2009 purchases. As a result, Cost of sales decreased by $11,

$22 and $10 in fiscal 2011, 2010 and 2009, respectively.

40