Albertsons 2006 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2006 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

|

|

SUPERVALU INC. and Subsidiaries

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Fair Value Disclosures of Financial Instruments

For certain of the company’s financial instruments, including cash and cash equivalents, receivables and

notes payable, the carrying amounts approximate fair value due to their short maturities.

The estimated fair value of notes receivable was in excess of the carrying value by approximately $0.1

million at February 25, 2006. Notes receivable are valued based on a discounted cash flow approach applying a

rate that is comparable to publicly traded debt instruments of similar credit quality.

The estimated fair value of the company’s long-term debt (including current maturities) was in excess of the

carrying value by approximately $35.8 million at February 25, 2006. The estimated fair value was based on

market quotes, where available, or market values for similar instruments.

The estimated fair value of the company’s interest rate swaps is the carrying value at February 25, 2006.

The fair value of interest rate swaps is the amount at which they could be settled and is estimated by obtaining

quotes from brokers.

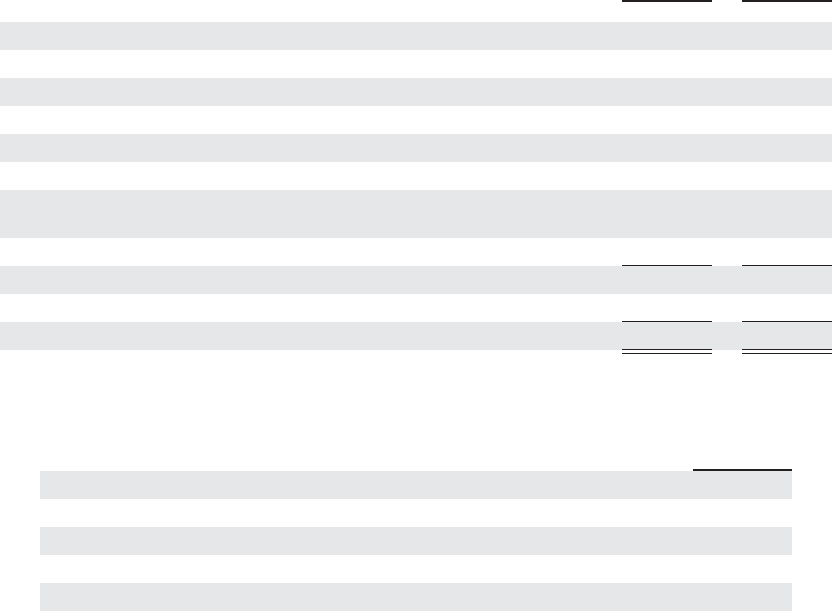

DEBT

Notes, debentures and other debt were composed of the following at year-end:

February 25,

2006

February 26,

2005

(In thousands)

7.875% promissory note due fiscal 2010 $ 350,000 $ 350,000

7.5% promissory note due fiscal 2013 300,000 300,000

Zero-coupon convertible debentures 258,548 247,325

6.64% medium-term notes due fiscal 2007 64,800 103,500

Variable rate industrial revenue bonds 51,680 59,530

8.28%-9.46% promissory notes due fiscal 2007-2011 10,543 15,252

8.02% and 8.57% obligations with quarterly payments of principal and

interest due fiscal 2007 2,401 18,495

Other debt 11,138 22,106

1,049,110 1,116,208

Less current maturities 74,650 64,320

Long-term debt $ 974,460 $1,051,888

Aggregate maturities of long-term debt are:

(In thousands)

2007 $ 74,650

2008 7,109

2009 12,042

2010 367,458

2011 and thereafter 587,851

F-24