Xcel Energy 2015 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2015 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

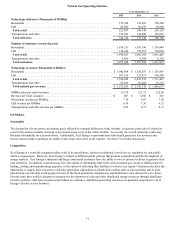

36

Management currently believes these prudently incurred costs are recoverable given the existing regulatory mechanisms in place.

However, adverse regulatory rulings or the imposition of additional regulations could have an adverse impact on our results of

operations and hence could materially and adversely affect our ability to meet our financial obligations, including debt payments and

the payment of dividends on our common stock.

Any reductions in our credit ratings could increase our financing costs and the cost of maintaining certain contractual

relationships.

We cannot be assured that any of our current ratings or our subsidiaries’ ratings will remain in effect for any given period of time, or

that a rating will not be lowered or withdrawn entirely by a rating agency. In addition, our credit ratings may change as a result of the

differing methodologies or change in the methodologies used by the various rating agencies. Any downgrade could lead to higher

borrowing costs. Also, our utility subsidiaries may enter into certain procurement and derivative contracts that require the posting of

collateral or settlement of applicable contracts if credit ratings fall below investment grade.

We are subject to capital market and interest rate risks.

Utility operations require significant capital investment. As a result, we frequently need to access capital markets. Any disruption in

capital markets could have a material impact on our ability to fund our operations. Capital markets are global in nature and are

impacted by numerous issues and events throughout the world economy. Capital market disruption events and resulting broad

financial market distress could prevent us from issuing new securities or cause us to issue securities with less than ideal terms and

conditions, such as higher interest rates.

Higher interest rates on short-term borrowings with variable interest rates could also have an adverse effect on our operating results.

Changes in interest rates may also impact the fair value of the debt securities in the nuclear decommissioning fund and master pension

trust, as well as our ability to earn a return on short-term investments of excess cash.

We are subject to credit risks.

Credit risk includes the risk that our customers will not pay their bills, which may lead to a reduction in liquidity and an increase in

bad debt expense. Credit risk is comprised of numerous factors including the price of products and services provided, the overall

economy and local economies in the geographic areas we serve, including local unemployment rates.

Credit risk also includes the risk that various counterparties that owe us money or product will breach their obligations. Should the

counterparties to these arrangements fail to perform, we may be forced to enter into alternative arrangements. In that event, our

financial results could be adversely affected and we could incur losses.

One alternative available to address counterparty credit risk is to transact on liquid commodity exchanges. The credit risk is then

socialized through the exchange central clearinghouse function. While exchanges do remove counterparty credit risk, all participants

are subject to margin requirements, which create an additional need for liquidity to post margin as exchange positions change value

daily. The Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) requires broad clearing of financial swap

transactions through a central counterparty, which could lead to additional margin requirements that would impact our liquidity.

However, we have taken advantage of an exception to mandatory clearing afforded to commercial end-users who are not classified as

a major swap participant. The Board of Directors has authorized Xcel Energy and its subsidiaries to take advantage of this end-user

exception.

We may at times have direct credit exposure in our short-term wholesale and commodity trading activity to various financial

institutions trading for their own accounts or issuing collateral support on behalf of other counterparties. We may also have some

indirect credit exposure due to participation in organized markets, such as SPP, PJM and MISO, in which any credit losses are

socialized to all market participants.

We do have additional indirect credit exposures to various domestic and foreign financial institutions in the form of letters of credit

provided as security by power suppliers under various long-term physical purchased power contracts. If any of the credit ratings of

the letter of credit issuers were to drop below the designated investment grade rating stipulated in the underlying long-term purchased

power contracts, the supplier would need to replace that security with an acceptable substitute. If the security were not replaced, the

party could be in technical default under the contract, which would enable us to exercise our contractual rights.