Xcel Energy 2015 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2015 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

94

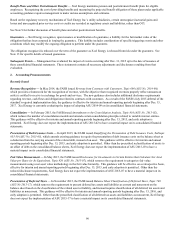

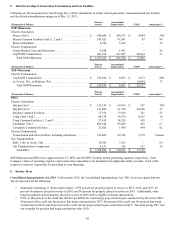

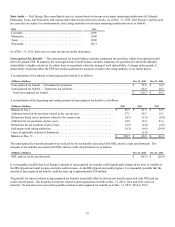

Issuances of Common Stock — During the year ended Dec. 31, 2014, Xcel Energy Inc. issued approximately 5.7 million shares of

common stock through an at-the-market (ATM) program and received cash proceeds of $172.7 million net of $1.9 million in fees and

commissions. Xcel Energy completed its ATM program as of June 30, 2014. The proceeds from the issuances of common stock were

used to repay short-term debt, infuse equity into the utility subsidiaries and for other general corporate purposes.

Deferred Financing Costs — Other assets included deferred financing costs of approximately $92 million and $85 million, net of

amortization, at Dec. 31, 2015 and 2014, respectively. Xcel Energy is amortizing these financing costs over the remaining maturity

periods of the related debt.

Capital Stock — Xcel Energy Inc. has 7,000,000 shares of preferred stock authorized to be issued with a $100 par value. At Dec. 31,

2015 and 2014, there were no shares of preferred stock outstanding.

The charters of PSCo and SPS authorize each subsidiary to issue 10,000,000 shares of preferred stock with par values of $0.01 and

$1.00 per share, respectively. At Dec. 31, 2015 and 2014, there were no preferred shares of subsidiaries outstanding.

Xcel Energy Inc. has 1,000,000,000 shares of common stock authorized to be issued with a $2.50 par value. Outstanding shares at

Dec. 31, 2015 and 2014 were 507,535,523 and 505,733,267, respectively.

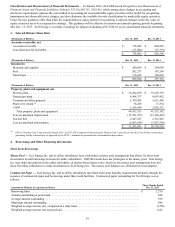

Dividend and Other Capital-Related Restrictions — Xcel Energy depends on its subsidiaries to pay dividends. All of Xcel Energy

Inc.’s utility subsidiaries’ dividends are subject to the FERC’s jurisdiction, which prohibits the payment of dividends out of capital

accounts; payment of dividends is allowed out of retained earnings only. Due to certain restrictive covenants, Xcel Energy Inc. is

required to be current on particular interest payments before dividends can be paid.

The most restrictive dividend limitations for NSP-Minnesota, NSP-Wisconsin and SPS are imposed by their respective state regulatory

commission. PSCo’s dividends are subject to the FERC’s jurisdiction under the Federal Power Act, which prohibits the payment of

dividends out of capital accounts; payment of dividends is allowed out of retained earnings only.

Only NSP-Minnesota has a first mortgage indenture which places certain restrictions on the amount of cash dividends it can pay to

Xcel Energy Inc., the holder of its common stock. Even with this restriction, NSP-Minnesota could have paid more than $1.7 billion

and $1.6 billion in additional cash dividends to Xcel Energy Inc. at Dec. 31, 2015 and 2014, respectively.

NSP-Minnesota’s state regulatory commissions indirectly limit the amount of dividends NSP-Minnesota can pay by requiring an

equity-to-total capitalization ratio between 46.9 percent and 57.3 percent. NSP-Minnesota’s equity-to-total capitalization ratio was

52.1 percent at Dec. 31, 2015 and $967 million in retained earnings was not restricted. Total capitalization for NSP-Minnesota was

$9.9 billion at Dec. 31, 2015, which did not exceed the limit of $10.5 billion.

NSP-Wisconsin cannot pay annual dividends in excess of approximately $33.3 million if its calendar year average equity-to-total

capitalization ratio is or falls below the state commission authorized level of 52.5 percent, as calculated consistent with PSCW

requirements. NSP-Wisconsin’s calendar year average equity-to-total capitalization ratio calculated on this basis was 52.6 percent at

Dec. 31, 2015 and $2.4 million in retained earnings was not restricted.

SPS’ state regulatory commissions indirectly limit the amount of dividends that SPS can pay Xcel Energy Inc. by requiring an equity-

to-total capitalization ratio (excluding short-term debt) between 45.0 percent and 55.0 percent. In addition, SPS may not pay a

dividend that would cause it to lose its investment grade bond rating. SPS’ equity-to-total capitalization ratio (excluding short-term

debt) was 53.8 percent at Dec. 31, 2015 and $438 million in retained earnings was not restricted.

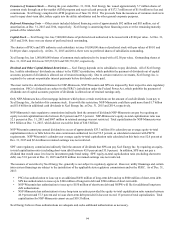

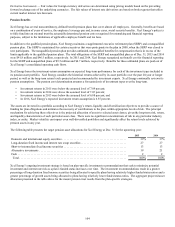

The issuance of securities by Xcel Energy Inc. generally is not subject to regulatory approval. However, utility financings and certain

intra-system financings are subject to the jurisdiction of the applicable state regulatory commissions and/or the FERC. As of Dec. 31,

2015:

• PSCo has authorization to issue up to an additional $450 million of long-term debt and up to $800 million of short-term debt.

• SPS has authorization to issue up to $100 million of long-term debt and $500 million of short-term debt.

• NSP-Wisconsin has authorization to issue up to $150 million of short-term debt and NSPW will file for additional long-term

debt authorization.

• NSP-Minnesota has authorization to issue long-term securities provided the equity-to-total capitalization ratio remains between

46.9 percent and 57.3 percent and to issue short-term debt provided it does not exceed 15 percent of total capitalization. Total

capitalization for NSP-Minnesota cannot exceed $10.5 billion.

Xcel Energy believes these authorizations are adequate and seeks additional authorization as necessary.