Whirlpool 2010 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2010 Whirlpool annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

|

|

31

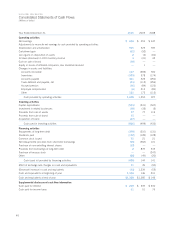

FIN ANCI AL S UMMA RY

The following is a summary of Whirlpool Corporation’s finan-

cial condition and results of operations for 2010, 2009 and

2008. For a more complete understanding of our financial con-

dition and results, this summary should be read together with

Whirlpool Corporation’s Consolidated Financial Statements and

related notes, and “Management’s Discussion and Analysis.”

This information appears in the Financial Supplement to the

Company’s Proxy Statement and in the Financial Supplement to

the 2010 Annual Report on Form 10-K filed with the Securities

and Exchange Commis sion, both of which are also available

through the Internet at www.whirlpoolcorp.com.

ABOU T WH IRL PO OL

Whirlpool Corporation (“Whirlpool”) is the world’s leading manu-

facturer of major home appliances with revenues over $18 billion

and net earnings available to Whirlpool of $619 million in 2010.

We are a leading producer of major home appliances in North

America and Latin America and have a significant presence in

markets throughout Europe and India. We have received world-

wide recognition for accomplishments in a variety of business

and social efforts, including leadership, diversity, innovative

product design, business ethics, social responsibility and com-

munity involvement. We conduct our business through four

reportable segments, which we define based on geography. Our

reportable segments consist of North America, Latin America,

Europe, and Asia. Our customer base is characterized by large,

sophisticated trade customers who have many choices and

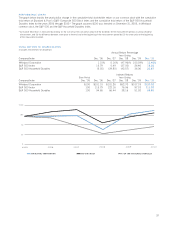

demand competitive products, services and prices. The charts

below summarize the balance of net sales by reportable segment

for 2010, 2009 and 2008, respectively:

We monitor country-specific economic factors such as gross

domestic product, unemployment, consumer confidence,

retail trends, housing starts and completions, sales of existing

homes and mortgage interest rates as key indicators of industry

demand. In addition to profitability, we also focus on country,

brand, product and channel sales when assessing and forecast-

ing financial results.

Our leading portfolio of brands includes: Whirlpool, Maytag,

KitchenAid, Brastemp and Consul, each of which have annual

revenues in excess of $1 billion. Our global branded consumer

products strategy is to introduce innovative new products,

increase customer brand loyalty, expand our presence in foreign

markets, enhance our trade management platform, improve total

cost and quality by expanding and leveraging our global operat-

ing platform and where appropriate, make strategic acquisitions

and investments.

In addition, as we grow revenues from our core products, our

strategy is to extend our core business by offering products or

services that are dependent on and related to our core business

and expand beyond the core into adjacent products through

stand-alone businesses that leverage our core competencies and

core business infrastructure.

2010 OVER VIE W

Whirlpool and the appliance industry as a whole faced signifi-

cant macroeconomic challenges across much of the world in

2010. We experienced strong signs of global economic recovery

during the first six months of 2010 with higher than expected

demand complemented by stable currencies, input costs and

appliance pricing. However, during the second half of 2010 we

experienced a significant slowing in sales growth, especially in

North America, increased material costs and competitive global

pricing pressure. Despite these challenging market conditions,

we experienced volume increases in all geographic regions

compared to 2009, especially in our Latin America region

where unit volumes increased more than 16% compared to

2009, and our Asia region where unit volumes increased more

than 22% compared to 2009.

Competition in the home appliance industry remained intense

in all global markets we serve. In addition to our traditional

competitors Electrolux, General Electric, and Kenmore in North

America, the emerging global competitors: LG, Bosch Siemens,

Samsung and Haier, have contributed to an increasingly com-

petitive pricing environment. We believe that our productivity

and cost controls and new innovative product introductions will

enhance our ability to respond to these competitive conditions.

Despite these challenging business conditions, Whirlpool’s

ongoing focus on cost reductions, productivity and innovative

new product launches continues to enable Whirlpool to adapt

to changes in the macroeconomic environment. We experienced

branded share growth in most markets we serve fueled by our

consumer-relevant innovations and our key new product launches,

which continue to be well-received by consumers. Consolidated

net sales increased 7.4% compared to 2009 and our consolidated

gross margin increased to 14.8% of net sales, an improvement

of 0.8 points compared to 2009.

During the year, Whirlpool remained focused on cost reduction

and productivity initiatives to offset higher material costs and on

continuing to bring consumer relevant innovation to reduce the

impact of the unfavorable price/mix environment.

Sales by Region

Europe,

Middle East,

Africa

21%

200820092010

Europe,

Middle East,

Africa

19%

Europe,

Middle East,

Africa

17%

North

America

55%

North

America

57%

North

America

53%

Latin

America

19%

Latin

America

22%

Latin

America

25%

Asia

3%

Asia

5% Asia

8%

Asia

4%