Tyson Foods 2002 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2002 Tyson Foods annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

|

|

notes to

consolidated

financial

statements

p 36

Note 4: Other Charges

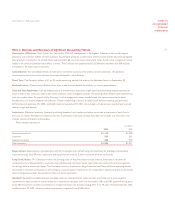

In August 2002, the Company announced its decision to restructure the live swine operation. The restructuring will result in the

closure of company-owned and leased feeder pig finishing farms in Arkansas and eastern Oklahoma. The Company will retain a

limited number of breeding operations in Oklahoma and northwest Arkansas as well as some feeder pig finishing operations in north

central Missouri. As a result of this decision, the Company recorded a live swine restructuring accrual of $26 million in the fourth

quarter of fiscal 2002. This amount is reflected in the pork segment as a reduction to operating income and included on the

consolidated statement of income in other charges.

In August 2002, the Company made the decision to capitalize on the strong recognition of the Tyson brand by expanding the

Tyson brand to beef and pork. Thus, in the fourth quarter of fiscal 2002, the Company recorded a write-down of $27 million related

to the discontinuation of the Thomas E. Wilson brand. This amount is reflected in the prepared foods segment as a reduction to

operating income and included on the consolidated statement of income in other charges.

Note 5: Allowance for Doubtful Accounts

At September 28, 2002, and September 29, 2001, the allowance for doubtful accounts was $26 million and $27 million, respectively.

In fiscal 2000, AmeriServe Food Distribution, Inc. (AmeriServe), a significant distributor of products to fast food and casual dining

restaurant chains, filed for reorganization in Delaware under Chapter 11 of the Federal Bankruptcy Code. The Company is a major

supplier to several AmeriServe customers. In the second quarter of fiscal 2000, the Company recorded a $24 million bad debt

reserve to fully reserve the AmeriServe receivable.

Note 6: Financial Instruments

In October 2000, the Company adopted SFAS No.133, “Accounting for Derivative Instruments and Hedging Activities,” (SFAS 133)

as amended. This statement requires the Company to recognize all derivatives on the balance sheet at fair value. Derivatives that

are not hedges must be adjusted to fair value through earnings. If the derivative is a hedge, depending on the nature of the hedge,

changes in the fair value of derivatives will either be offset against the change in fair value of the hedged assets, liabilities or firm

commitments through earnings, or recognized in other comprehensive income (loss) until the hedged item is recognized in

earnings. The ineffective portion of a derivative’s change in fair value is recognized in earnings.

The adoption of SFAS 133 in October 2000 resulted in a cumulative effect of approximately $6 million after tax ($9 million

pretax) being charged to other comprehensive income (loss).

At September 28, 2002, and September 29, 2001, the Company had derivative related balances totaling $1 million and $5 million

recorded in other current assets and $19 million and $20 million recorded in other current liabilities, respectively.

Cash Flow Hedges: The Company uses derivatives to moderate the financial and commodity market risks of its business operations.

Derivative products, such as futures and option contracts, are considered to be a hedge against changes in the amount of future cash

flows related to commodities procurement. The Company also enters into interest rate swap agreements to adjust the proportion

of total long-term debt and leveraged equipment loans that are subject to variable interest rates. Under these interest rate swaps,

the Company agrees to pay a fixed rate of interest times a notional principal amount and to receive in return an amount equal to

a specified variable rate of interest times the same notional principal amount. These interest rate swaps are considered to be a hedge

against changes in the amount of future cash flows associated with the Company’s variable rate interest payments.

Tyson Foods, Inc. 2002 annual report