Supercuts 2005 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2005 Supercuts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS, CONTINUED

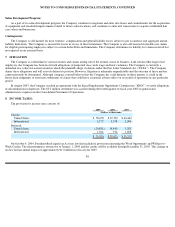

purchase price), it is neither known nor identifiable at the time of the acquisition. The cash flow history of a salon primarily results from repeat

walk-in customers driven by the existing personal relationship between the customer and the stylist(s). Under FAS No. 141, “Business

Combinations,” a customer base does not meet the criteria for recognition apart from goodwill. As such, this portion of the purchase price is

captured within goodwill and should not be attributed to any other contractual arrangement. Because we are acquiring the “going concern”

value of the salon, driven primarily by the manner in which the salon has been operated and the existing walk-in customer base’s relationship

with the stylist(s), the value being acquired is subsumed into goodwill in accordance with FAS No. 141.

Residual goodwill further represents the Company’s opportunity to strategically combine the acquired business with the Company’s

existing structure to serve a greater number of customers through its expansion strategies. In the acquisitions of international salons, beauty

schools and hair restoration centers, the residual goodwill primarily represents the growth prospects that are not captured as part of acquired

tangible or identified intangible assets. Generally the goodwill recognized in the North American salon transactions is expected to be fully

deductible for tax purposes and the goodwill recognized in the international salon transactions is non-deductible for tax purposes. Goodwill

generated in certain acquisitions, such as Hair Club for Men and Women (discussed below), is generally not deductible for tax purposes due to

the acquisition structure of the transaction.

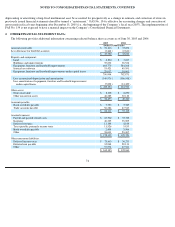

In December 2004, the Company purchased Hair Club for Men and Women (Hair Club) for approximately $210 million, financed with

debt. Hair Club offers a comprehensive menu of hair restoration solutions ranging from Extreme Hair Therapy(TM) to the non-surgical Bio-

Matrix(R) Process and the latest advancements in hair transplantation, based on an analysis of what is best for each customer’s situation. This

industry is comprised of numerous locations domestically and is highly fragmented. As a result, we believe there is an opportunity to

consolidate this industry through acquisition, as well as cross-marketing of the Company’s products and services. Expanding the hair

restoration business organically and through acquisition would allow us to add incremental revenue which is neither dependent upon nor

dilutive to our existing salon and school businesses.

Hair Club operations have been included in the operations of the Company since the acquisition was completed on December 1, 2004, and

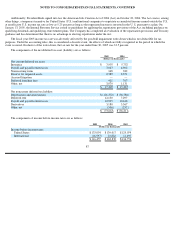

are reported in Note 11 in the “hair restoration centers” segment. Unaudited pro forma summary information is presented below for the years

ended June 30, 2005 and 2004, assuming the acquisition of Hair Club had occurred on July 1, 2003 (i.e., the first day of fiscal year 2004).

Preparation of the pro forma summary information was based upon assumptions deemed appropriate by the Company’s management. The pro

forma summary information presented below is not necessarily indicative of the results that actually would have occurred if the acquisition had

been consummated on the first day of fiscal year 2004, and is not intended to be a projection of future results.

Note: There were no extraordinary items, changes in accounting principles, or material nonrecurring items included in the pro forma amounts

above.

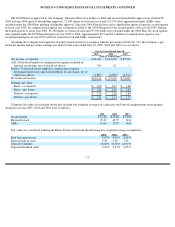

79

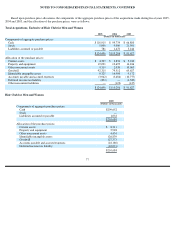

For the Years Ended June 30,

2005

2004

Actual

ProForma

Actual

ProForma

(Dollars in thousands)

(unaudited)

Revenue

$

2,194,294

$

2,243,290

$

1,923,143

$

2,013,683

Net Income

$

64,631

$

64,538

$

104,218

$

103,874

EPS

$

1.39

$

1.39

$

2.26

$

2.25