Supercuts 2005 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2005 Supercuts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

|

|

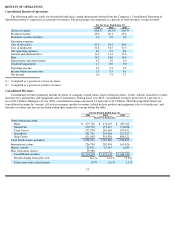

CRITICAL ACCOUNTING POLICIES

The Consolidated Financial Statements are prepared in conformity with accounting principles generally accepted in the United States of

America. In preparing the Consolidated Financial Statements, we are required to make various judgments, estimates and assumptions that could

have a significant impact on the results reported in the Consolidated Financial Statements. We base these estimates on historical experience and

other assumptions believed to be reasonable under the circumstances. Estimates are considered to be critical if they meet both of the following

criteria: (1) the estimate requires assumptions about material matters that are uncertain at the time the accounting estimates are made, and

(2) other materially different estimates could have been reasonably made or material changes in the estimates are reasonably likely to occur

from period to period. Changes in these estimates could have a material effect on our Consolidated Financial Statements.

Our significant accounting policies can be found in Note 1 to the Consolidated Financial Statements contained in Item 8 of this Form 10-

K. We believe the following accounting policies are most critical to aid in fully understanding and evaluating our reported financial condition

and results of operations.

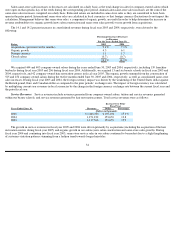

Goodwill

We review goodwill for impairment annually or at any time events or circumstances indicate that the carrying value may not be fully

recoverable. According to our accounting policy, an annual review is performed in the third quarter of each year, or more frequently if

indicators of potential impairment exist. Our impairment review process is based on a discounted future cash flow approach that uses estimates

of revenues for the reporting units, driven by assumed organic growth rates, estimated future gross margin and expense rates, as well as

acquisition integration and maturation, and appropriate discount and tax rates. These estimates are consistent with the plans and estimates that

are used to manage the underlying businesses. Charges for impairment of goodwill for a reporting unit may be incurred if the reporting unit

fails to achieve its assumed revenue growth rates or assumed gross margin, or if interest rates increase significantly. We generally consider our

various concepts to be reporting units when we test for goodwill impairment because that is where we believe goodwill naturally resides.

During the quarter ending March 31, 2005, we reduced our expectations for the European business based on recent growth trends. Based

on the results of our third quarter fiscal year 2005 goodwill impairment testing, which factored in these revised growth trend expectations, we

wrote down the carrying value of the European business to reflect its estimated fair value. As a result, we recorded a pre-tax, non-cash charge

of $38.3 million during the third quarter. Two of the most significant assumptions underlying the determination of fair value of goodwill for

our European business are discount and tax rates. In connection with the measurement we performed during the third quarter, a 100 basis point

increase in the discount rate we used would have resulted in an impairment charge of approximately $42.1 million instead of $38.3 million,

while a 100 basis point decrease in the discount rate would have resulted in an impairment charge of approximately $34.5 million.

Additionally, a five percent increase in the tax rate would have resulted in an impairment charge of approximately $40.3 million instead of

$38.3 million, while a five percent decrease in the tax rate would have resulted in an impairment charge of approximately $37.3 million.

Long

-Lived Assets

We assess the impairment of long-lived assets annually or when events or changes in circumstances indicate that the carrying value of the

assets or the asset grouping may not be recoverable. Our impairment analysis is performed on a salon-by-salon basis. Factors considered in

deciding when to perform an impairment review include significant under-performance of an individual salon in relation to expectations,

significant economic or geographic trends, and significant changes or planned changes in our use of the assets. Recoverability of assets that

will continue to be used in our operations is measured by comparing the carrying amount of the asset to the related total estimated future net

cash flows. If an asset’s carrying

30