Supercuts 2005 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2005 Supercuts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

|

|

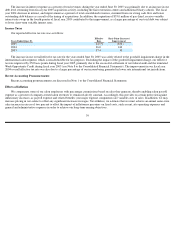

On-Balance Sheet Obligations

Our long-term obligations are composed primarily of senior term notes and a revolving credit facility. The related interest expected to be

paid in relation to these obligations is not included in the table above because of the variable nature of certain interest payments. Additionally,

certain senior term notes are hedged by contracts with financial institutions commonly referred to as interest rate swaps, as discussed in Item

7A, “Quantitative and Qualitative Disclosures about Market Risk.” At June 30, 2005, $0.6 million of our long-term obligations represents the

fair value of the adjustments made to mark these hedge contracts to fair value and an additional $1.9 million represents a deferred gain related

to the termination of certain interest rate hedge contracts.

Other long-term liabilities in the contractual obligations table include a total of $12.9 million related to a salary deferral program, $8.0

million related to established contractual payment obligations under retirement and severance payment agreements for a small number of

retired employees, $4.9 million related to the Executive Profit Sharing Plan (see Note 9) and $0.4 million related to contractual payments

required under non-

compete agreements entered into in conjunction with recent acquisitions. All amounts exclude amounts deemed to represent

interest payments.

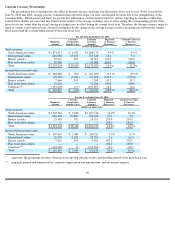

This table excludes the short-term liabilities, other than the current portion of long-term debt, disclosed on our balance sheet as the

amounts recorded for these items will be paid in the next year. We have no unconditional purchase obligations, as defined by FAS 47,

“Disclosure of Long-Term Obligations.” Also excluded from the contractual obligations table are payment estimates associated with employee

health and workers’ compensation claims for which we are self-insured. The majority of our recorded liability for self-insured employee health

and workers’ compensation losses represents estimated reserves for incurred claims that have yet to be filed or settled.

The Company has unfunded deferred compensation contracts covering certain management and executive personnel. The deferred

compensation contracts are offered to key executives based on their accomplishments within the Company. Because we cannot predict the

timing or amount of our future payments related to these contracts, such amounts were not included in the table above. Related obligations

totaled $12.9 and $10.7 million at June 30, 2005 and 2004, respectively, and are included in other non-current liabilities in the Consolidated

Balance Sheet. Refer to Note 9 of the Consolidated Financial Statements for additional information.

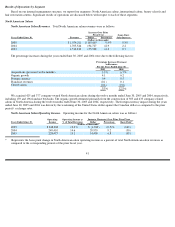

Off-Balance Sheet Arrangements

Operating leases primarily represent long-term obligations for the rental of salon, school and hair restoration center premises, including

leases for company-owned locations, as well as salon franchisee subleases of approximately $146.0 million, which are funded by franchisees.

Regarding the franchisee subleases, we generally retain the right to the related salon assets net of any outstanding obligations in the event of a

default by a franchise owner. Management has not experienced and does not expect any material loss to result from these arrangements.

Other long-term obligations represent our guarantees, primarily entered into prior to December 31, 2002, on a limited number of

equipment lease agreements between our salon franchisees and leasing companies. If the franchisee should fail to make payments in

accordance with the lease, we will be held liable under such agreements and retain the right to possess the related salon operations. We believe

the fair value of the salon operations exceeds the maximum potential amount of future lease payments for which we could be held liable. The

existing guaranteed lease obligations, which have an aggregate undiscounted value of $2.2 million at June 30, 2005, terminate at various dates

between June 2006 and April 2009. The Company has not experienced and does not expect any material loss to result from these arrangements.

49