SkyWest Airlines 2005 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2005 SkyWest Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

53

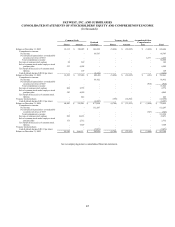

December 31, 2005, 2004, and 2003 respectively. These adjustments have been reflected in the accompanying consolidated

statements of stockholders’ equity and comprehensive income.

Fair Value of Financial Instruments

The carrying amounts reported in the consolidated balance sheets for receivables and accounts payable approximate fair values

because of the immediate or short-term maturity of these financial instruments. Marketable securities are reported at fair value in

the consolidated balance sheets. The fair value of the Company’s long-term debt is estimated based on current rates offered to the

Company for similar debt and approximately $1,751.8 million as of December 31, 2005, as compared to the carrying amount of

$1,753.9 million. The Company’s fair value of long-term debt as of December 31, 2004 was $495.8 million as compared to the

carrying amount of $495.8 million.

SFAS No. 133, “Accounting for Derivative Instruments and Certain Hedging Activities, SFAS No. 138, Accounting for

Certain Derivative Instruments and Certain Hedging Activity, an Amendment of SFAS 133 and related interpretations require that

all derivative instruments be recorded on the balance sheet at their respective fair values.

The Company has an interest rate swap agreement to manage its exposure on the debt instrument related to the Company’s

headquarters. The Company's policies do not permit management to enter into derivative instruments for any purpose other than

cash flow hedging purposes. Accordingly, the Company does not speculate using derivative instruments. The Company assesses

interest rate cash flow risk by identifying and monitoring changes in interest rate exposures that may adversely impact expected

future cash flows and by evaluating hedging opportunities. The fair values of the Company's derivative instruments are

recognized as other current liabilities in the accompanying balance sheet. In accordance with provisions of SFAS No. 133, the

Company recorded a $344,000 and $691,000 liability at December 31, 2005 and 2004 respectively, in the accompanying

consolidated balance sheets representing the fair value of the outstanding interest rate swap agreement. The Company decreased

interest expense by $347,000 and $209,000 during the years ended December 31, 2005 and 2004, respectively, relating to

adjustments to the fair value and of the derivatives.

Segment Reporting

The Company has adopted SFAS No. 131, Disclosures about Segments of an Enterprise and Related Information. This

statement requires disclosures related to components of a company for which separate financial information is available that is

evaluated regularly by the Company’s chief operating decision maker in deciding how to allocate resources and in assessing

performance. Management believes that the Company has only one operating segment in accordance with SFAS No. 131 because

the Company’s business consists of scheduled regional airline service.

New Accounting Standard

As contemplated by SFAS Statement 123, Accounting for Stock-Based Compensation(“SFAS 123”), we currently account for

share-based payments to employees using intrinsic value method set forth in APB Opinion 25, Accounting for Stock Issued to

Employees and, as such, generally recognize no compensation cost for employee stock options. We have determined that we will

adopt SFAS 123 using the modified prospective method. On December 16, 2004, the Financial Accounting Standards Board

("FASB") issued SFAS No. 123(R) (revised 2004), Share-Based Payment (“Statement 123(R)”), which revises SFAS No. 123

and supersedes APB Opinion 25. Generally, the approach in Statement 123(R) is similar to the approach described in SFAS No.

123; however, Statement 123(R) requires all share-based payments to employees, including grants of employee stock options, to

be recognized as an expense in the statement of operations based on their fair values. We will be required to adopt Statement

123(R) effective January 1, 2006.

The adoption of the fair value method set forth in Statement 123(R) is likely to have a significant impact on our future results of

operations, although it is not anticipated to have a significant impact on our overall financial position. The impact of adoption of

SFAS 123(R) cannot be predicted at this time because it will depend on levels of share-based payments granted in the future.

However, had we adopted Statement 123(R) in prior periods, the impact of that standard would have approximated the impact of

SFAS 123 as described in the disclosure of pro forma net income and earnings per share in Note 1 to our consolidated financial

statements set forth in Item 8 of this Report. Statement 123(R) also requires the benefits of tax deductions in excess of recognized

compensation cost to be reported as a financing cash flow, rather than as an operating cash flow as required under current