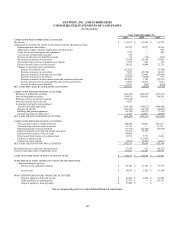

SkyWest Airlines 2005 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2005 SkyWest Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

38

SkyWest Airlines has not historically funded a substantial portion of its aircraft acquisitions with working capital. Rather, it

has generally funded its aircraft acquisitions through a combination of operating leases and debt financing. At the time of each

aircraft acquisition, we evaluate the financing alternatives available, and selected one or more of these methods to fund the

acquisition. In the event that alternative financing can not be arranged at the time of delivery, Bombardia has financed aircraft

acquisitions until more permanent arrangements can be made. Subsequent to this initial acquisition of an aircraft, we may also

refinance the aircraft or convert one form of financing to another (e.g., replacing debt financing with leveraged lease financing).

At present, we intend to satisfy our 2006 firm aircraft purchase commitment, as well as our acquisition of any additional

aircraft, through a combination of operating leases and debt financing, consistent with our historical practices. Based on current

market conditions and discussions with prospective leasing organizations and financial institutions, we currently believe that we

will be able to obtain financing for the committed acquisitions, as well as additional aircraft, without materially reducing the

amount of working capital available for our operating activities.

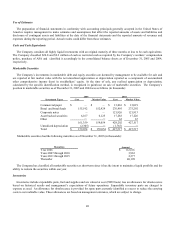

Aircraft Lease and Facility Obligations

We also have significant long-term lease obligations primarily relating to our aircraft fleet. At December 31, 2005, we had

247 aircraft under lease with remaining terms ranging from one to 18 years. Future minimum lease payments due under all long-

term operating leases were approximately $3.2 billion at December 31, 2005. Assuming a 7.0% discount rate, which is the rate

used to approximate the implicit rates within the applicable aircraft leases, the present value of these lease obligations would have

been equal to approximately $2.1 billion at December 31, 2005.

As part of our leveraged lease agreements, we typically agree to indemnify the equity/owner participant against liabilities that

may arise due to changes in benefits from tax ownership of the respective leased aircraft. See Note 4 to our consolidated financial

statements set forth in Item 8 of this Report.

Long-term Debt Obligations

Our total long-term debt at December 31, 2005 was $1,753.9 million, of which $1,746.5 million related to the acquisition of

Brasilia turboprop, CRJ200 and CRJ700 aircraft and $7.4 million related to our corporate office building. The average effective

rate on the debt related to the Brasilia turboprop and CRJ200 aircraft was approximately 5.7% at December 31, 2005.

Approximately, $256.7 million of our current portion of long-term debt is expected to be refinanced into permanent long-term

financing within the next year.

Seasonality

Our results of operations for any interim period are not necessarily indicative of those for the entire year, since the airline

industry is subject to seasonal fluctuations and general economic conditions. Our operations are somewhat favorably affected by

increased travel on our pro-rate routes, historically occurring in the summer months, and are unfavorably affected by decreased

business travel during the months from November through January and by inclement weather which occasionally results in

cancelled flights, principally during the winter months.

New Accounting Standard

As contemplated by SFAS Statement 123, Accounting for Stock-Based Compensation(“SFAS 123”), we currently account for

share-based payments to employees using intrinsic value method set forth in APB Opinion 25, Accounting for Stock Issued to

Employees and, as such, generally recognize no compensation cost for employee stock options. We have determined that we will

adopt SFAS 123 using the modified prospective method. On December 16, 2004, the Financial Accounting Standards Board

("FASB") issued SFAS No. 123(R) (revised 2004), Share-Based Payment (“Statement 123(R)”), which revises SFAS No. 123

and supersedes APB Opinion 25. Generally, the approach in Statement 123(R) is similar to the approach described in SFAS No.

123; however, Statement 123(R) requires all share-based payments to employees, including grants of employee stock options, to

be recognized as an expense in the statement of operations based on their fair values. We will be required to adopt Statement

123(R) effective January 1, 2006.