Royal Caribbean Cruise Lines 2001 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2001 Royal Caribbean Cruise Lines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56

|

|

Notes to the Consolidated Financial Statements (continued)

44 Royal Caribbean Cruises Ltd.

their separate legal identities but would operate as if they were

a single unified economic entity. The contracts governing the

dual-listed company merger would provide that the boards of

directors of the two companies would be identical and that, as far

as possible, the shareholders of Royal Caribbean and P&O

Princess would be placed in substantially the same economic

position as if they held shares in a single enterprise which

owned all of the assets of both companies. The net effect of

the dual-listed company merger would be that the shareholders

of Royal Caribbean would own an economic interest equal to

49.3% of the combined company and the shareholders of

P&O Princess would own an economic interest equal to

50.7% of the combined company.

The obligations of Royal Caribbean and P&O Princess to effect

the dual-listed company merger are subject to the satisfaction

of various conditions, including the receipt of certain regula-

tory approvals and consents and approval by the shareholders

of each of Royal Caribbean and P&O Princess. No assurance

can be given that all required approvals and consents will be

obtained, and if such approvals and consents are obtained, no

assurance can be given as to the terms, conditions and timing

of the approvals and consents. If the dual-listed company

merger is not completed by November 16, 2002, either party

can terminate the agreement if it is not in material breach of its

obligations thereunder. We have incurred, and continue to

incur, costs which have been or will be deferred in connection

with the dual-listed company merger. In the event the transac-

tion is not consummated, we would be required to write these

costs off, resulting in an estimated impact to earnings of approx-

imately $15 million. If the dual-listed company merger is

completed, these deferred costs, together with additional

costs, would be capitalized as part of the transaction.

If the merger agreement is terminated under certain circum-

stances, we would be obligated to pay P&O Princess a break

fee of $62.5 million. These circumstances include, among other

things, our board of directors withdrawing or adversely

modifying its recommendation to shareholders to approve the

dual-listed company merger, our board of directors recom-

mending an alternative acquisition transaction to shareholders,

and our shareholders failing to approve the dual-listed

company merger if another acquisition proposal with respect

to Royal Caribbean exists at that time. Similarly, P&O Princess

would be obligated to pay us a break fee of $62.5 million upon

the occurrence of reciprocal circumstances.

In December 2001, Carnival Corporation (Carnival) announced

a competing pre-conditional offer to acquire all of the

outstanding shares of P&O Princess. In connection with its

pre-conditional offer, Carnival solicited proxies from P&O

Princess’ shareholders in favor of an adjournment of the

P&O Princess’ special meeting prior to a shareholder vote to

approve the dual-listed company merger. On February 14,

2002, Royal Caribbean and P&O Princess convened special

meetings of their respective shareholders to approve the dual-

listed company merger. Prior to voting to approve the merger,

the shareholders of each company voted to adjourn their

respective meetings until an unspecified future date. We do

not know at this time the date on which the meetings will

be reconvened.

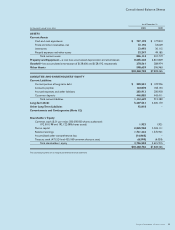

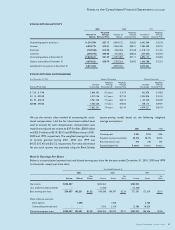

Note 4. Property and Equipment

Property and equipment consists of the following (in thousands):

2001 2000

Land $ 7,056 $ 7,056

Vessels 8,289,028 6,168,383

Vessels under capital lease 771,131 768,474

Vessels under construction 396,286 508,954

Other 366,914 313,689

9,830,415 7,766,556

Less – accumulated depreciation

and amortization (1,224,967) (934,747)

$ 8,605,448 $6,831,809

Vessels under construction include progress payments for the

construction of new vessels as well as planning, design, interest,

commitment fees and other associated costs. We capitalized

interest costs of $37.0 million, $44.2 million and $34.6 million

for the years 2001, 2000 and 1999, respectively. Accumulated

amortization related to vessels under capital lease was

$136.2 million and $112.9 million at December 31, 2001 and

2000, respectively.

Note 5. Other Assets

In July 2000, we purchased a new issue of convertible

preferred stock, denominated in British pound sterling, for

approximately $300 million from First Choice Holidays PLC.

The convertible preferred stock carries a 6.75% coupon.

Dividends of $19.4 million and $9.2 million were earned in

2001 and 2000, respectively and recorded in Other income

(expense). If fully converted, our holding would represent

approximately a 17% interest in First Choice Holidays PLC.