Proctor and Gamble 2007 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2007 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

|

|

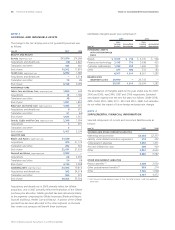

Millions of dollars except per share amounts or as otherwise specied.

Notes to Consolidated Financial Statements The Procter & Gamble Company 61

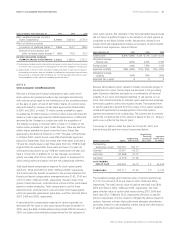

Shares in millions; Years ended June 30 2006 2005

Basic weighted average common

shares outstanding 3,054.9 2,515.6

Effect of dilutive securities

Conversion of preferred shares (1) 154.1 158.3

Exercise of stock options and

other unvested equity awards (2) 76.9 63.2

3,285.9 2,737.1

(1) Despite being included currently in diluted net earnings per common share, the actual conversion

to common stock occurs pursuant to the repayment of the ESOPs’ obligations through 2035.

(2) Approximately 41 million in 2007, 44 million in 2006 and 48 million in 2005 of the Company’s

outstanding stock options were not included in the diluted net earnings per share calculation

because to do so would have been antidilutive (i.e., the total proceeds upon exercise would

have exceeded the market value of the underlying common shares).

NOTE 8

We have a primary stock-based compensation plan under which

stock options are granted annually to key managers and directors

with exercise prices equal to the market price of the underlying shares

on the date of grant. A total of 229 million shares of common stock

were authorized for issuance under plans approved by shareholders

in 2001 and 2003, of which 73 million remain available for grant.

An additional 20 million shares of common stock were authorized for

issuance under a plan approved by Gillette shareowners in 2004 and

assumed by the Company in conjunction with the acquisition of

The Gillette Company in October 2005. A total of 14 million of the

shares remain available for grant under this plan. There are also ve

million shares available for grant under the Future Shares Plan

approved by the Board of Directors in 1997. This plan will terminate

in October 2007. Grants issued under P&G shareholder approved

plans since September 2002 are vested after three years and have a

10-year life. Grants issued under these plans from July 1998 through

August 2002 are vested after three years and have a 15-year life,

while grants issued prior to July 1998 are vested after one year and

have a 10-year life. In addition to our key manager and director

grants, we make other minor stock option grants to employees for

which vesting terms and option lives are not substantially different.

Total stock-based compensation expense for stock option grants

was $612, $526 and $459 for 2007, 2006 and 2005, respectively.

The total income tax benet recognized in the income statement for

these stock-based compensation arrangements was $163, $140 and

$125 for 2007, 2006 and 2005, respectively. We also make minor

grants of restricted stock, restricted stock units and other stock-based

grants to certain employees. Total compensation cost for these

restricted stock, restricted stock units and other stock-based grants,

which are generally expensed at grant date, was $56, $59 and $65 in

2007, 2006 and 2005, respectively.

In calculating the compensation expense for options granted, we

estimated the fair value of each grant issued through December 31,

2004, using the Black-Scholes option-pricing model. Effective January 1,

2005, we utilize a binomial lattice-based model for the valuation of

stock option grants. The utilization of the binomial lattice-based model

did not have a signicant impact on the valuation of stock options as

compared to the Black-Scholes model. Assumptions utilized in the

model, which are evaluated and revised, as necessary, to reect market

conditions and experience, were as follows:

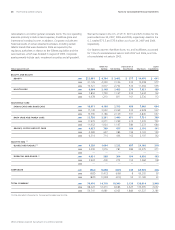

Years ended June 30 2006 2005

Interest rate 4.5% – 4.7% 3.2% – 4.5%

Weighted average

interest rate 4.6% 4.4%

Dividend yield 1.9% 1.9%

Expected volatility 15% – 20% 15% – 20%

Weighted average

volatility 19% 20%

Expected life in years 9 9

Because lattice-based option valuation models incorporate ranges of

assumptions for inputs, those ranges are disclosed in the preceding

table. Expected volatilities are based on a combination of historical

volatility of our stock and implied volatilities of call options on our

stock. We use historical data to estimate option exercise and employee

termination patterns within the valuation model. The expected term

of options granted is derived from the output of the option valuation

model and represents the average period of time that options

granted are expected to be outstanding. The interest rate for periods

within the contractual life of the options is based on the U.S. Treasury

yield curve in effect at the time of grant.

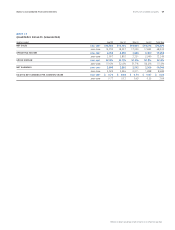

A summary of options under the plans as of June 30, 2007, and

activity during the year then ended is presented below:

Weighted Avg.

Remaining Aggregate

Weighted Avg. Contractual Intrinsic Value

Options in thousands Options Exercise Price Life in Years (in millions)

Outstanding,

beginning of year 362,352 $43.71

Granted 33,091 63.33

Exercised (37,658) 37.77

Canceled (2,779) 51.66

355,006 46.10 7.5 $5,424

257,171 41.22 7.0 5,132

The weighted average grant-date fair value of options granted was

$17.29, $16.30 and $14.34 per share in 2007, 2006 and 2005,

respectively. The total intrinsic value of options exercised was $894,

$815 and $526 in 2007, 2006 and 2005, respectively. The total

grant-date fair value of options that vested during 2007, 2006 and

2005 was $552, $388 and $532, respectively. We have no specic

policy to repurchase common shares to mitigate the dilutive impact of

options; however, we have historically made adequate discretionary

purchases, based on cash availability, market trends and other factors,

to satisfy stock option exercise activity.