Proctor and Gamble 2000 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2000 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

|

|

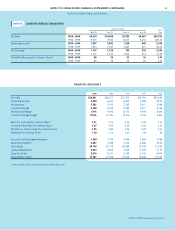

The Procter & Gamble Company and Subsidiaries

30

Millions of dollars except per share amounts

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation: The consolidated financial statements

include The Procter & Gamble Company and its controlled

subsidiaries (the Company). Investments in companies over which

the Company exerts significant influence, but does not control

the financial and operating decisions, are accounted for using the

equity method. These investments are managed as integral parts

of the Company’s business units, and segment reporting reflects

such investments as consolidated subsidiaries.

Use of Estimates: Preparation of financial statements in con-

formity with accounting principles generally accepted in the

United States of America requires management to make estimates

and assumptions that affect the amounts reported in the consoli-

dated financial statements and accompanying disclosures. These

estimates are based on management’s best knowledge of current

events and actions the Company may undertake in the future.

Actual results may ultimately differ from estimates.

New Pronouncements: In June 1998, the FASB issued Statement

No. 133, “Accounting for Derivative Instruments and Hedging

Activities.” This statement will be adopted effective July 1, 2000,

but is not expected to materially impact the Company’s financial

statements.

In December 1999, the Securities and Exchange Commission issued

Staff Accounting Bulletin 101, “Revenue Recognition in Financial

Statements.” The effective date has been deferred pending addi-

tional interpretive guidance. Based on current interpretations, no

material impact on the Company’s financial statements is anticipated.

Currency Translation: Financial statements of subsidiaries outside

the U.S. generally are measured using the local currency as the

functional currency. Adjustments to translate those statements

into U.S. dollars are accumulated in a separate component of

shareholders’ equity. For subsidiaries operating in highly infla-

tionary economies, the U.S. dollar is the functional currency.

Remeasurement adjustments for highly inflationary economies

and other transactional exchange gains and losses are reflected

in earnings.

Cash Equivalents: Highly liquid investments with maturities

of three months or less when purchased are considered cash

equivalents.

Inventory Valuation: Inventories are valued at cost, which is not

in excess of current market price. Cost is primarily determined by

either the average cost or the first-in, first-out method. The

replacement cost of last-in, first-out inventories exceeded carrying

value by approximately $83 and $100 at June 30, 2000 and 1999,

respectively.

Goodwill and Other Intangible Assets: The cost of intangible

assets is amortized, principally on a straight-line basis, over the

estimated periods benefited, generally forty years for goodwill

and periods ranging from three to forty years for other intangible

assets. The realizability of goodwill and other intangibles is eval-

uated periodically when events or circumstances indicate a

possible inability to recover the carrying amount. Such evaluation

is based on various analyses, including cash flow and profitability

projections that incorporate the impact of the Company’s existing

businesses. The analyses necessarily involve significant manage-

ment judgment to evaluate the capacity of an acquired business to

perform within projections. Historically, the Company has gener-

ated sufficient returns from acquired businesses to recover the cost

of the goodwill and other intangible assets.

Property, Plant and Equipment: Property, plant and equipment

are recorded at cost reduced by accumulated depreciation.

Depreciation expense is based on estimated useful lives using the

straight-line method. Estimated useful lives are periodically

reviewed, and where warranted, changes are made that result in

an acceleration of depreciation.

Fair Values of Financial Instruments: Fair values of cash equiv-

alents, short and long-term investments and short-term debt

approximate cost. The estimated fair values of other financial

instruments, including debt, equity and risk management instru-

ments, have been determined using available market information

and valuation methodologies, primarily discounted cash flow

analysis. These estimates require considerable judgment in inter-

preting market data, and changes in assumptions or estimation

methods may significantly affect the fair value estimates.

Reclassifications: Certain reclassifications of prior years’ amounts

have been made to conform with the current year presentation.

NOTE 2 ORGANIZATION 2005

In June 1999, the Board of Directors approved a multi-year restruc-

turing program in conjunction with the Company’s Organization

2005 initiative.

Due to the nature and duration of this program, the timing and

amount of estimated costs and savings require significant judgment

and may change over time. Based on current expectations, the

total cost of the program is estimated to be $2.7 billion ($2.1 billion

after tax) over a six year period (fiscal 1999 through fiscal 2004).

The costs of this program primarily relate to separation and relo-

cation of employees and streamlining manufacturing capabilities,

including consolidation and closure. Certain other costs directly

related to Organization 2005 also are included.