MoneyGram 2009 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2009 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

-

565

-

566

-

567

-

568

-

569

-

570

-

571

-

572

-

573

-

574

-

575

-

576

-

577

-

578

-

579

-

580

-

581

-

582

-

583

-

584

-

585

-

586

-

587

-

588

-

589

-

590

-

591

-

592

-

593

-

594

-

595

-

596

-

597

-

598

-

599

-

600

-

601

-

602

-

603

-

604

-

605

-

606

-

607

-

608

-

609

-

610

-

611

-

612

-

613

-

614

-

615

-

616

-

617

-

618

-

619

-

620

-

621

-

622

-

623

-

624

-

625

-

626

-

627

-

628

-

629

-

630

-

631

-

632

-

633

-

634

-

635

-

636

-

637

-

638

-

639

-

640

-

641

-

642

-

643

-

644

-

645

-

646

-

647

-

648

-

649

-

650

-

651

-

652

-

653

-

654

-

655

-

656

-

657

-

658

-

659

-

660

-

661

-

662

-

663

-

664

-

665

-

666

-

667

-

668

-

669

-

670

-

671

-

672

-

673

-

674

-

675

-

676

-

677

-

678

-

679

-

680

-

681

-

682

-

683

-

684

-

685

-

686

-

687

-

688

-

689

-

690

-

691

-

692

-

693

-

694

-

695

-

696

-

697

-

698

-

699

-

700

-

701

-

702

-

703

-

704

-

705

-

706

|

|

Table of Contents

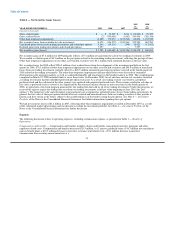

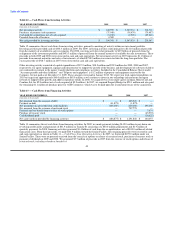

Table 8 — Assets in Excess of Payment Service Obligations

December 31, December 31,

(Amounts in thousands) 2009 2008

Cash and cash equivalents (substantially restricted) $ 3,776,824 $ 4,077,381

Receivables, net (substantially restricted) 1,054,381 1,264,885

Trading investments and related put options (substantially restricted) 26,951 47,990

Available-for-sale investments (substantially restricted) 298,633 438,774

5,156,789 5,829,030

Payment service obligations (4,843,454) (5,437,999)

Assets in excess of payment service obligations $ 313,335 $ 391,031

Liquidity

Our primary sources of liquidity include cash flows generated by the sale of our payment instruments, our cash and cash equivalent

balances, credit capacity under our credit facilities and proceeds from our investment portfolio. Our primary operating liquidity needs

relate to the settlement of payment service obligations to our agents and financial institution customers, as well as general operating

expenses.

To meet our payment service obligations at all times, we must have sufficient highly liquid assets and be able to move funds globally on a

timely basis. On average, we pay over $1.0 billion a day to settle our payment service obligations. We generally receive a similar amount

on a daily basis for the principal amount of our payment instruments sold and the related fees. We use the incoming funds from sales of

new payment instruments to settle our payment service obligations for previously sold payment instruments. This pattern of cash flows

allows us to settle our payment service obligations through on-going cash generation rather than liquidating investments or utilizing our

revolving credit facility. We have historically generated, and expect to continue generating, sufficient cash flows from daily operations to

fund ongoing operational needs.

The timely remittance of funds by our agents and financial institution customers is an important component of our liquidity and allows

for the pattern of cash flows described above. If the timing of the remittance of funds were to deteriorate, it would alter our pattern of

cash flows and could require us to liquidate investments or utilize our revolving credit facility to settle payment service obligations. To

manage this risk, we closely monitor the remittance patterns of our agents and financial institution customers and act quickly if we detect

deterioration or alternation in remittance timing or patterns. If deemed appropriate, we have the ability to deactivate an agent's equipment

at any time, thereby preventing the initiation or issuance of further money transfers and money orders. See "Enterprise Risk Management

— Credit Risk" for further discussion of this risk and our mitigation efforts.

We also seek to maintain liquidity beyond our operating needs to provide a cushion through the normal fluctuations in our payment

service assets and obligations and to invest in the infrastructure and growth of our business. While the assets in excess of payment service

obligations, as shown in Table 8, would be available to us for our general operating needs and investment in the Company, we consider a

portion of our assets in excess of payment service obligations as additional assurance that regulatory and contractual requirements are

maintained. We believe we have sufficient assets and liquidity to operate and grow our business for the next 12 months. Should our

liquidity needs exceed our operating cash flows, we believe that our external financing sources, including availability under our Senior

Facility, will be sufficient to meet any liquidity needs.

Cash and Cash Equivalents — To ensure we maintain adequate liquidity to meet our operating needs at all times, we keep a significant

portion of our investment portfolio in cash and cash equivalents at financial institutions rated Aa3 or better by Moody's and AA- or better

by S&P and in United States government money market funds rated Aaa by Moody's and AAA by S&P. As of December 31, 2009, cash

and equivalents totaled $3.8 billion, representing 92 percent of our total investment portfolio. Cash equivalents consisted of time deposits,

certificates of deposit and money market funds that invest in United States government and government agency securities.

Clearing and Cash Management Banks — We move and receive money through a network of clearing and cash management banks. The

relationships with these clearing banks and cash management banks are a critical

43