HSBC 2002 Annual Report Download - page 307

Download and view the complete annual report

Please find page 307 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

297 -

298

298 -

299

299 -

300

300 -

301

301 -

302

302 -

303

303 -

304

304 -

305

305 -

306

306 -

307

307 -

308

308 -

309

309 -

310

310 -

311

311 -

312

312 -

313

313 -

314

314 -

315

315 -

316

316 -

317

317 -

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

305

income’ . These securities are included in the balance sheet at cost adjusted for the amortisation of premium and

discounts arising on acquisition. Any profit or loss on realisation of these securities is recognised in the profit

and loss account as it arises and included in ‘Gains on disposal of investments’ .

Other debt securities and equity shares are included in the balance sheet at market value. Changes in the market

value of such assets are recognised in the profit and loss account as ‘Dealing profits’ as they arise. Debt

securities and listed equity shares which were acquired in exchange for advances in order to achieve an orderly

realisation continue to be reported as advances under UK GAAP.

Under SFAS 115 ‘Accounting for Certain Investments in Debt and Equity Securities’ , all the above debt

securities and equity shares, with the exception of equity investments without a readily determinable market

value, are classified and disclosed within one of the following three categories: held-to-maturity; available-for-

sale; or trading. Held-to-maturity securities are measured at amortised cost less provision for any other-than-

temporary declines in value. Available-for-sale securities are measured at fair value with unrealised holding

gains and losses excluded from earnings and reported net of applicable taxes and minority interests in a separate

component of shareholders’ funds. Provisions for other-than-temporary declines in value of available-for-sale

securities are recognised in earnings. Trading securities are measured at fair value with unrealised holding gains

and losses included in earnings.

Under US GAAP, HSBC’ s investment securities, other participating interests and debt securities and equity

shares with a readily determinable market value acquired in exchange for advances are classified as available-

for-sale securities, except for certain securities held by RNYC at acquisition, which were classified as held-to-

maturity. All other debt and equity shares are categorised as trading securities.

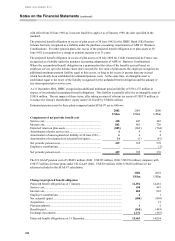

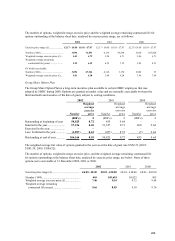

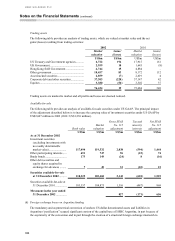

The book and market values of these debt securities and equity shares with a readily determinable market value

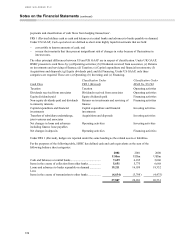

are analysed as follows:

2002 2001

Book value Marke

t

valuation Book value

M

arke

t

valuation

US$m US$m US$m US$m

Trading............................................................. 76,424 76,424 75,684 75,684

Available-for-sale ............................................ 118,325 120,468 103,557 104,873

Held-to-maturity .............................................. 4,648 4,905 4,703 4,866

During the year, US$1,229 million (2001: US$442 million, 2000: US$850 million) of net unrealised gains on

available-for-sale securities were included in Other Comprehensive Income (‘OCI’ ). US$393 million (2001:

US$442 million, 2000: US$270 million) of net gains were reclassified out of OCI and recognised as part of

income for the year.

Upon adoption of SFAS 133 in 2001, HSBC transferred US$190 million of securities previously classified as

held-to-maturity to securities available-for-sale. The reclassification resulted in a net of tax cumulative effect

adjustment loss of US$11 million. Under the provisions of SFAS 133, such a reclassification does not call into

question HSBC’ s interest to hold current or future debt securities to their maturity.

At the same date, HSBC transferred US$1,042 million of securities from available-for-sale to held-to-maturity.

During 2002, HSBC recorded net losses under US GAAP of US$308 million (2001 US$104 million; 2000:

US$25 million) in respect of diminutions in value of available-for-sale securities which were considered to be

other than temporary. These losses were treated as realised items and included in net income.