HSBC 2002 Annual Report Download - page 293

Download and view the complete annual report

Please find page 293 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

295 -

296

296 -

297

297 -

298

298 -

299

299 -

300

300 -

301

301 -

302

302 -

303

303 -

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

291

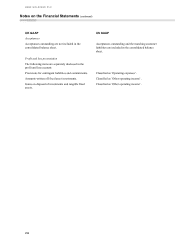

UK GAAP US GAAP

Foreign currency

Under SSAP 20 ‘Foreign Currency Translation’ a

company’ s local currency is the currency of the

primary economic environment in which it operates

and generates net cash flows. Foreign exchange

differences arising when translating non- local

currency assets and liabilities into the local currency

are reported in the profit and loss account.

Under SFAS 52 ‘Foreign Currency Translation’ an

entitiy’ s functional currency is the currency of the

primary economic environment in which it operates.

An entity operating in a single economic environment

may have only one functional currency. Foreign

exchange differences arising when translating non-

functional currency assets and liabilities into the local

currency are reported in the profit and loss account.

Own shares held

UK GAAP allows for the inclusion of own shares held

within equity shares.

AICPA Accounting Research Bulletin 51‘Consolidated

Financial Statements’ requires a reduction in

shareholders’ equity for own shares held.

Dividends payable

Dividends declared after the period end are recorded in

the period to which they relate.

Dividends are recorded in the period in which they are

declared.

Deferred taxation

Deferred taxation is generally provided in the accounts

for all timing differences, subject to assessment of the

recoverability of deferred tax assets.

As provided by SFAS 109 ‘Accounting for Income

Taxes’ , deferred tax liabilities and assets are

recognised in respect of all temporary differences. A

valuation allowance is raised against any deferred tax

asset where it is more likely than not that the asset, or a

part thereof, will not be realised.

Sale and repurchase transactions (‘repos’) and reverse

repos

Repos and reverse repos are accounted for as if the

collateral involved remains with the transferor. On the

balance sheet, repos are included within ‘Deposits by

banks’ and ‘Customer accounts’ and reverse repos are

included within ‘Loans and advances to banks’ or

‘Loans and advances to customers’ .

Under SFAS 140 ‘Accounting for Transfers and

Servicing of Financial Assets and Extinguishment of

Liabilities’ , repos and reverse repos transacted under

agreements that give the transferee the right by contract

or custom to sell or repledge the collateral give rise to

the following adjustments and disclosures. For repos,

where the transferee has the right to sell or repledge the

collateral, the transferor would report the securities

separately in the Financial Statements from other

securities not so encumbered. For reverse repos, where

the transferee has the right to sell or repledge the

collateral, the transferee should not recognise the

pledged asset but should disclose the fair value of the

collateral and if the transferee sells collateral pledged

to it, the proceeds from the sale and the transferee’ s

obligation to return the collateral should be recognised.