HSBC 2002 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2002 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

|

|

HSBC HOLDINGS PLC

Financial Review (continued)

134

• maintenance of strong balance sheet liquidity

ratios;

• monitoring of depositor concentration both in

terms of the overall funding mix and to avoid

undue reliance on large individual depositors;

and

• maintenance of liquidity contingency plans.

These plans include the identification of early

indicators of liquidity problems and actions

which are to be taken to improve the liquidity

position at this stage, together with the actions

which the entity can take to maintain liquidity in

a crisis situation while minimising the long-term

impact on its business.

Current accounts and savings deposits payable

on demand or at short notice form a significant part

of HSBC’s overall funding. HSBC places

considerable importance on the stability of these

deposits, which is achieved through HSBC’s diverse

geographical retail banking activities and by

maintaining depositor confidence in HSBC’ s capital

strength. Professional markets are accessed for the

purposes of providing additional funding,

maintaining a presence in local money markets and

optimising asset and liability maturities.

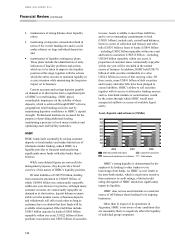

HSBC

HSBC funds itself essentially by raising customer

deposits in local markets and makes limited use of

wholesale market funding, indeed HSBC is a

liquidity provider to financial markets placing

significantly more funds with other banks than it

borrows.

While consolidated figures are not useful for

management purposes, they do provide a broad

overview of the nature of HSBC's liquidity position.

Of total liabilities of US$759 billion, funding

from customers amounted to US$495 billion, of

which US$485 billion was contractually repayable

within one year. However in practice, although many

customer accounts are contractually repayable on

demand or at short notice, deposit balances remain

stable as in the normal course of business deposits

and withdrawals will offset each other as long as

customers have no doubts that their funds will be

available when required. Other liabilities include

US$53 billion deposits by banks (US$50 billion

repayable within one year), US$22 billion of short

positions in securities and US$35 billion of securities

in issue. Assets available to meet these liabilities,

and to cover outstanding commitments to lend

(US$51 billion), include cash, central bank balances,

items in course of collection and treasury and other

bills (US$31 billion); loans to banks (US$95 billion

– including US$92 billion repayable within one year)

and loans to customers (US$352 billion – including

US$164 billion repayable within one year). A

proportion of customer loans contractually repayable

within one year will be extended in the normal

course of business. In addition, HSBC held US$176

billion of debt securities marketable at a value

US$2.0 billion in excess of that carrying value. Of

these assets, some US$41 billion of debt securities

and treasury and other bills have been pledged to

secure liabilities. HSBC’s ability to sell securities

together with its access to alternative funding sources

such as inter-bank markets or securitisation, would

be the routes through which HSBC would meet

unexpected outflows in excess of available liquid

assets.

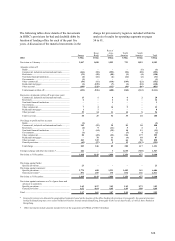

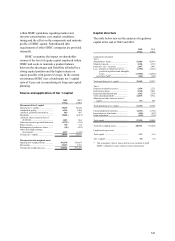

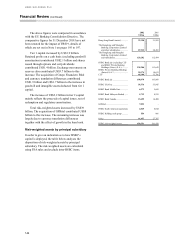

Asset, deposits and advances (US$bn)

Debt securities and loans Customer accounts

Loans and advances to customer Total assets

HSBC’s strong liquidity is demonstrated by the

surplus of its lending to other banks over its

borrowings from banks. As HSBC is a net lender to

the inter-bank market, which is much more sensitive

than customers to credit ratings, a limited credit

rating downgrade of HSBC should not significantly

impair its liquidity.

HSBC does not use securitisations as a material

source of off-balance-sheet funding for its ongoing

businesses.

Other than in respect of its operations in

Argentina, HSBC is not aware of any conditions that

are reasonably likely to negatively affect the liquidity

of individual group companies.

271.2

352.3

495.4

759.3

265.2 308.6

450.0

696.2

258.8 289.8

427.1

674.3

0

100

200

300

400

500

600

700

800

2002 2001 2000